Key Points

TTIP through the Backdoor: Agribusiness counting on CETA’s regulatory cooperation agenda for the bulk of the benefits AFTER implementation

EU meat labeling scheme under threat through CETA. Post-NAFTA, the North American meat industry is highly integrated and forced the U.S. to repeal country of origin labeling (COOL)

European producers priced out of market due to market failure and unfair competition

ICS: Agribusiness Right to Sue Governments

I. TTIP through the Backdoor: Agribusiness counting on CETA’s (de) regulatory cooperation agenda for the bulk of the benefits

A. The Canadian Cattlemen’s Association (CCA), a key industry lobby group, is counting on de-regulation of the EU’s food safety standards to reap most of the benefits from CETA.

- In virtually every public document related to CETA, the CCA has indicated that while the zero-duty quotas for additional access to European markets are welcome, the real benefits for Canada will come through removing “longstanding technical barriers.”

- These include carcass washes such as citric acid and peroxyacetic acid.

John Masswohl, director of government relations for the Canadian Cattlemen’s Association:

Until these treatments are approved, the signal that we have from the cattle side, from Cargill and JBS, is that they will not be interested in accessing the European market…And, as long as Cargill and JBS remain uninterested in the European market, there’s not really much incentive for cattle producers to increase their production of cattle that are eligible for Europe.

- Through “technical negotiations” after CETA implementation, the CCA seeks to address:

In his testimony to the Canadian Parliament on November 17, 2016, on endorsing the CETA implementing legislation, Masswohl reiterated the CCA’s key condition:

We will expect a commitment from the Government of Canada to develop and fully fund a comprehensive strategy utilizing technical, advocacy, and political skills to achieve the elimination of the remaining non-tariff barriers to Canadian beef.

B. A review of CETA shows parallel provisions to TTIP, particularly in its focus on removing non-tariff barriers, and the emphasis on “risk based” and “science based” regulations as opposed to the precautionary principle.

- Canada has many of the same food safety assessment processes and standards as the U.S.: widespread hormone and antibiotic use, use of ractopamine and GMOs and lack of labeling;

- Canada has challenged the EU’s precautionary principle alongside the U.S. in both the hormone beef and GMO challenges at the World Trade Organization and thus sees the EU’s precautionary principle as a key barrier to trade.

- Similar concerns to TTIP prevail in CETA about quality of Canadian meat imports and weakening of EU food safety, labor, environmental and public health standards related to meat production. See IATP’s Selling Off the Farm, for a detailed analysis.

TTIP Through the Backdoor: (de) Regulatory Cooperation

NAFTA set up an informal process for regulatory cooperation, for example, the Technical Working Group on Pesticides (TWG, set up in 1996). Between 2016 and 2021 the TWG aims to:

- Align maximum residue levels (MRLs)—the amount of legally acceptable pesticide in a food

- Expand the joint review process for biopesticides and registration for minor users

- Address differences in data requirements and the risk assessment process to harmonize pesticide regulation in NAFTA

The process lacks transparency and industry presence dominates these critical regulatory negotiations between the U.S. and Canada. CETA sets a up a system that goes beyond NAFTA whereby technical committees discuss these critical regulatory issues in secret with industry at the table and the Joint Committee maybe empowered to put policy changes into effect without consultation with or oversight from member states.

Agribusiness operating in North America (Canada, U.S. and Mexico) will utilize CETA--with or without TTIP--to achieve the removal of important regulatory barriers to agribusiness trade.

C. CETA regulatory cooperation is mislabled as “voluntary”

- Through CETA’s regulatory cooperation chapter (21), dialogue process on biotechnology, chapter (25), the Sanitary and Phytosanitary (SPS) and Technical Barriers to Trade (TBT) chaptersi CETA creates a “Living Agreement.”

- Together, these provisions aim to target EU’s regulations on food and agriculture, including on GMO approvals and zero tolerance.

- CETA is therefore a “permanent project” where actions agreed in CETA’s Joint Committee cir-cumvent the European and member state parliaments. In addition, there is legal about the role member states will play on regulatory decisions stemming from technical and specialized com-mittees and agreed to by CETA’s joint committee.

II. EU’s meat labeling scheme under threat through CETA. Post-NAFTA, the North American meat industry is highly integrated and forced the U.S. to repeal country of origin labeling.

A. Canadian beef and pork quota expansion provides big incentives for the North American Meat Industry to restructure production chains to fill the quota that Canada is currently not filling (particularly if agribusiness achieves its goals of removing regulatory barriers in CETA’s living agreement).

Canadian National Farmers Union notes:

Canada’s decision to sign the Canada-US Free Trade Agreement (CUSTA) and the North American Free Trade Agreement (NAFTA) increased continental integration, strengthened the power of the packers [meat processors], and pushed down prices in all three NAFTA signatory countries. Yet one further example: the takeover by Cargill of the Canadian packing sector gave those companies increased ability to move cattle and beef across the border to the detriment of cattle prices in both nations.

B. One major result of this meat industry integration has been the decade long fight on and repeal of Country of Origin Labeling (COOL) legislation in the U.S. for meat.

- The legislation, which over 90 percent of U.S. consumers supported, required processors to state where the animal was born, raised and slaughtered.

- Canada and Mexico, on behalf of the North American Meat Industry, put an end to this much desired consumer demand. They brought a challenge to the World Trade Organization, complaining that the U.S. law violates trade rules and they won.

- The EU has similar COOL legislation that would be vulnerable to trade dispute challenges as meat trade with Canada increases. Meanwhile, the EU parliament is considering COOL for processed meat which goes beyond the repealed U.S. legislation.

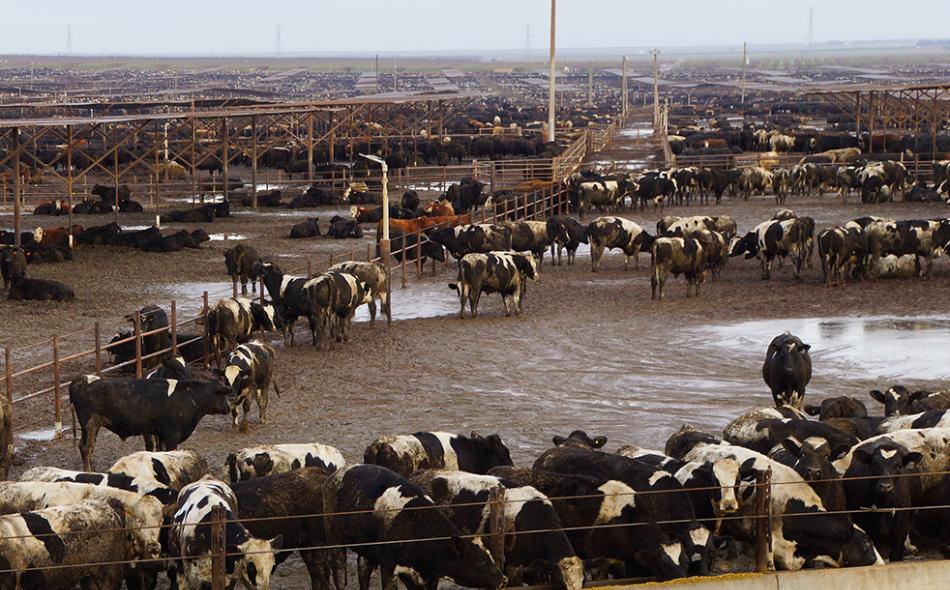

III. Unfair Competition due to scale/model of production and market failure due to agribusiness concentration

A. Canadian Feedlots (farms that fatten cattle for slaughter), pig and poultry operations can often be as large as U.S. farms

- Sizes can be as large as 20,000 cattle, between 5,000 and 20,000 pigs and 100,000 birds

- Example of scale:

average pig farm in Germany: 586 pigs/farm; average pig farm in Canada: 1,919 pigs/farm; average pig farm in U.S.: 6,081 pigs/farm

B. European farmers priced out of the market given the on-going European crisis in the livestock sector and lack of comparable regulations in Canada

- Canadian prices are dropping; oversupply is already a problem for some products

- Increased exports to the EU will work to reduce producer payments in the EU

- Canadian pork has sold for as little as 60 percent less than European pork. In 2014, despite the price crash in the European pork sector, Canadian price was still 25 percent lower. On average, Canadian pork sells between 15 and 35 percent less than European pork.1

- Market opening through CETA enables Canadian producers to offer their products in the EU at much cheaper prices than comparable EU producers.

C. No special safeguard for the EU in agriculture.

- Only Canada successfully negotiated an agricultural special safeguard for over a 100 tariff lines: “…only Canada may apply a special safeguard pursuant to Article 5 of the WTO Agreement on Agriculture [related to human, animal, plant health risks]. (Article 2.7.3 of the CETA Agreement).

- The EU’s recent declarations on the issue only reiterate the EU’s ability to use existing WTO safeguards within the framework of existing EU regulations.

- Moreover, the EU declaration agreed with Belgium appears to limit Belgium to negotiate (within 12 months of signing CETA) when it could ask the Commission to trigger the existing WTO safeguard clauses. The final decision would of course rest with the Commission and ultimately the Council to determine whether and to what extent to apply these safeguard provisions. In another words, nothing new has been agreed.

D. Extreme agribusiness concentration in the livestock sector in North America will force further consolidation of the livestock sector in the EU, disadvantaging both European producers and consumers

- Two companies (JBS and Cargill) control over 90 percent of the beef packing business in Canada

- Only four companies control over 85 percent of the much bigger U.S. market: JBS, Cargill, Tyson, National Beef

- Lower Canadian standards on production (i.e. poor animal welfare) make meat cheaper to produce than in Europe. Proposed changes to Canadian Food and Drug regulations would allow meat processing technologies (illegal in the EU) such as irradiation of ground beef, leading to even more small processors leaving the business and further consolidating a powerful industry (see hyperlink)

- In the last few decades, the European livestock sector has also been consolidating, but 15 companies still dominate the European meat sector. CETA (and other EU FTAs) will accelerate agribusiness concentration, further depressing farm prices, even as farmers struggle with high input costs. Decreased competition will also hurt European consumers.

- Brazil-based JBS has bought out major meat processors in North America and globally to become the number one meat processor in the world. In 2019, JBS will be free to relocate to Europe after its contract with the Brazilian National Development Bank (BNDS) ends. JBS has an aggressive record of mergers and acquisitions and had plans to shift to Ireland until BNDS denied permission.

IV. ICS: Agribusiness Right to Sue Governments

A. CETA’s investor-state provisions allow companies like Cargill and JBS to sue EU governments for regulations that may curtail their future profits. Because there are 47,000 U.S. subsidiaries based in Canada, CETA can be used by these companies (even if TTIP is stalled) in addition to Canadian ones to challenge EU regulations.

The recent European Public Health Alliance report, Unhealthy Side Effects of CETA notes:

While CETA opens up agricultural markets, it does not address the associated risks linked to drug- resistant infections and does not contain specific measures needed to protect the consumer and patients from them. Via the ICS, it would make it more difficult to introduce stricter controls on antibiotic use in meat and dairy animals in the future.

It stresses:

If current trends continue, drug-resistant infections could kill 10 million people per year globally by 2050 at a cumulative cost of 100 trillion USD. Via tariff elimination, trade in meat and meat products is expected to increase under the Agreement. This may result in more intensive farming methods, consolidation of larger farm holdings and an increase in antibiotic use.

1. Thomsen, B. 2016. CETA’s threat to agricultural markets and food quality. In Making Sense of CETA, 2nd Edition. PowerShift, CCPA et al. Berlin/Ottowa, pgs. 51-58