Agricultural “dumping” – the practice of exporting commodities at prices below the cost of production -- can be devastating for farmers in importing countries, especially in low-income countries with little power to use trade rules to defend their markets. It is unfair competition for producers in other exporting countries. And by encouraging overproduction in the U.S., it traps U.S. producers, too, in a never-ending need for higher yields, or bigger farms, or both.

Corn is emblematic of the problems created by dumping because it is such an important export crop for the U.S. and because more and more acres are given to corn production despite persistent low prices and the importance of corn to other countries’ food security, including in Mexico, Central America and east and southern Africa. After decades of low prices, corn prices increased sharply in 2007/2008, ushering in what appeared to be the end of low prices and dumping. A period of instability followed, when prices fell only to rise again in 2011, before falling again, renewing the dumping that is harmful to farmers in the South and the North. With so many losers, why does dumping persist?

Why does dumping matter?

Dumping matters for at least three reasons. First, it undermines the economic viability of competing farmers, whether the farmers are growing crops for their domestic markets, or selling their crops to traders for export in competition with U.S. production. This is especially a problem for largely agricultural developing countries that rely on agriculture for economic stability. It has been the subject of ongoing controversies at the World Trade Organization (WTO) and in the context of the North American Free Trade Agreement (NAFTA), particularly among developing country governments whose farmers complain about the flood of cheap imports.

Second, dumping is a threat to U.S. producers, most of whom sell their product into markets that are controlled by just a handful of agricultural commodity trading corporations (four corporations control an estimated 75-90 percent of grain trade globally[1]). The prices farmers get for their crops, on average, are often less than their average cost of production. The gap lessened, and even disappeared briefly, while commodity prices were higher after the 2007-2008 food price crisis. But prices are now down again, the lowest they have been since 2006. Net farm income in the U.S. is down by 50 percent from 2013.[2] U.S. commodity farmers rely on off-farm income as well as government payments to stay in business. The economic consequences of a system that reinforces dumping are felt by U.S. commodity growers and their families, their hired workers, and by the rural communities they live in – communities that are deprived of capital that should support vibrant economic life.

Third, dumping creates an economic environment that undermines the realization of environmental objectives. Care of the natural resource base, including soil health, water quality and the ecological diversity of farmland, are all squeezed, not just because commodity markets externalize environmental costs, but also because sustainable practices are priced out by increasingly concentrated competition. The result is a vicious circle of policies that harm family farmers, the environment, and local economies in both the U.S. and the countries receiving agribusiness’ exports from the U.S.

It is not uncommon for there to exist short-term price discrepancies between domestic and export markets. No market is perfect and commodity markets are rife with market failures and imperfections. Dumping is different. Dumping destabilizes markets. Dumping is unpredictable. It undermines domestic agricultural production, which is an important source of poverty-reducing growth.

Estimating dumping

IATP has calculated the extent of U.S. dumping of wheat, soybeans, corn, rice and cotton periodically since the 1990s. The common-sense assumption is that—at least on average and most of the time—the export price should be higher than the production price, to allow the cost of transportation and some profit for the handler. IATP uses the definition of dumping established in the GATT for markets in which the market price may not reflect “normal value” (for example because of the presence of significant public subsidies). In such cases, normal value has to be constructed.

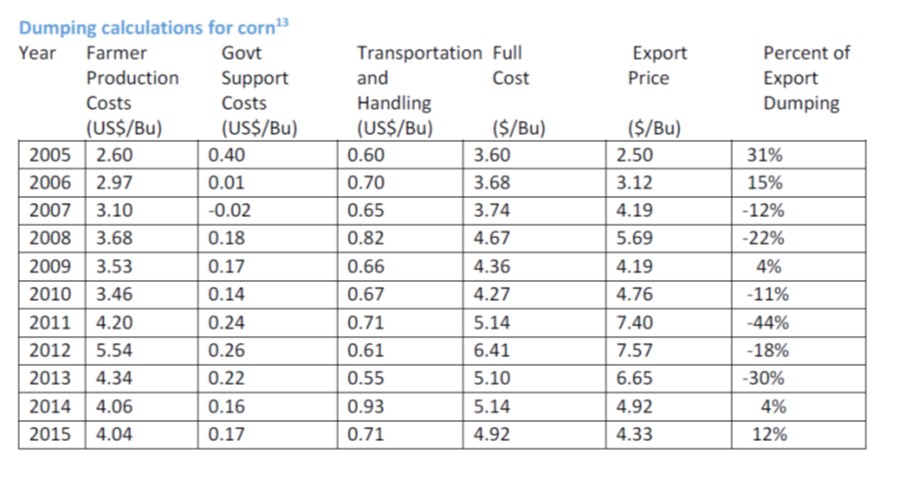

Using data from the U.S. Department of Agriculture (USDA) and the Organization for Economic Cooperation and Development (OECD), IATP calculates dumping by comparing production costs and export prices, looking at each commodity separately. In our new calculations of dumping rates,[3] we relied on the same methodology as in the 2003 and 2005 analyses, adding the costs of production to government support allocated for those crops and estimating transportation costs to arrive at an approximation of the full cost of production, which we then compare to export prices.

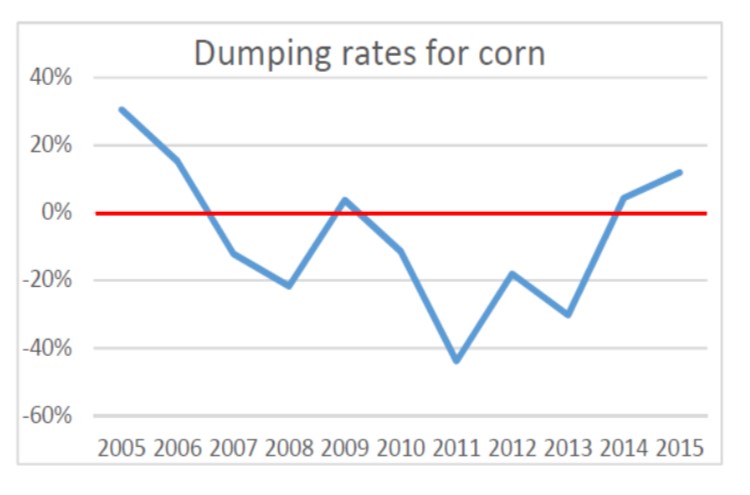

Graph 1 illustrates the results of those estimates for corn. As prices fell in the wake of the food price crisis and the price spike following the 2011-12 drought in the U.S., the rate of dumping of corn increased, reaching 12 percent in 2015. Despite the apparent pause in dumping during the price shocks of 2007-2008, and 2011, dumping persists. Current projections for continued overproduction of agricultural commodities and low prices point to a return to dumping for the foreseeable future.

While much of the international debate on dumping in agriculture, particularly at the WTO, has focused on the role of government subsidies, the issue in the U.S. context is more complex. It’s not only the amount of the subsidies, but the incentives they create to produce certain crops that then require larger markets, and the lack of any policy tools to ensure a fair price from the marketplace. That imperative in turn drives U.S. trade policy, not only at the WTO but in other agreements like NAFTA as well.

How have U.S. farmers fared under this system?

The fact that U.S. corn can continue to be sold at prices below the cost of production, especially given the small relative share of subsidies to total costs, seems counterintuitive. USDA’s Costs of Production includes costs of seeds, fertilizers, labor and other inputs, as well as expenses such as the cost of his or her own labor (opportunity cost of unpaid labor) and the implied costs of land. “Capital recovery of machinery and equipment” will in most cases mean paying back loans on those purchases, or planning to replace equipment that wears out. A farmer might absorb some of those losses in the short term, but a business cannot run at a perpetual loss. To cover the revenue shortfall, farm families are pushed to seek off-farm work. Often, they are looking for health insurance, too, as the cost of health care is another major issue for U.S. farmers and their families.[4]

Lots of parties make money from agriculture, including - some years - farmers. Many years, however, farmers work at a loss. Agribusiness makes money much more consistently. When we look at the cost of production and the movement to ports and then to export, there are profits and losses at various stages along the supply chain but much of it is hidden behind proprietary contracts and vertically integrated supply chains. The system is structured in a way that allows, even encourages, farmers to operate at a loss, which maximizes profits further downstream for agribusiness and leaves the public covering the farmers’ losses.

The current Farm Bill revenue insurance programs respond to price drops, but they are not designed to resolve them. They compensate farmers to some degree for the catastrophic drop in farm prices, even as costs have continued to rise. They do nothing to slow or lessen production. Farm incomes have plummeted for the last three years,[5] and the level of farm debt to income is the highest since the 1980s.[6] Since the payments under these programs are based on a five-year Olympic average (i.e., discounting the highest and lowest prices) for each crop, continued low prices means that the payments will continue to plummet as well. The U.S. government’s answer has been to encourage exports to compensate for low prices, but that response has failed to raise prices, and has not resolved farmers’ underlying lack of market power.

Dumping on Mexico under NAFTA

Corn holds an important place in Mexico’s economy, diet and culture. Under NAFTA, U.S. corn exports to Mexico increased more than 400 percent in the first few years of the agreement, disrupting local markets. Based on Mexican Census data, Tim Wise estimates that more than 2 million Mexicans left agriculture in the wake of NAFTA’s flood of imports, or as many as one quarter of the farming population.[7] Even when dumping rates decreased during the period of high prices, existing public support programs for agriculture in Mexico, as in the U.S., tended to support the largest farmers and agribusiness interests, rather than the smaller producers who had been the backbones of their rural economies.[8]

The integration of supply chains under NAFTA that has resulted both from the trade deal and from each country’s agricultural policies has undermined rural economies on both sides of the border. Exports of cheap corn to Mexico accompanied the expansion of cattle production in that country. Many of those animals are then brought back across the border for processing, with the resulting meat sold in the United States or exported back to Mexico at low prices (increasingly, the animals and beef cross in both directions). Along the way, and despite the expanded market, small and medium scale farmers and ranchers have lost bargaining power and revenue.

Corn has become a bargaining chip in recent trade debates between the U.S. and Mexico. The Mexican government has responded to the Trump administration’s calls to renegotiate – or abandon – NAFTA by seeking to diversify its sources of corn imports. One proposal in the Mexican Senate calls for the government to cease corn imports from the U.S. and instead purchase from Brazil, in effect substituting imports from one set of agribusiness to another.[9]

Who benefits from dumping?

The benefits of export oriented agriculture tend to accrue to the largest actors, particularly the agribusinesses most directly involved in international markets. While farmers’ planting decisions are locked in seasonally or even longer, agribusinesses are set up to react to changes in markets at lightning speed. Those companies profit when prices rise or when they fall, as long as they are successfully predicting the direction of change.

New phenomena such as computer driven high frequency trading have amplified price swings. Grain traders have better risk management strategies, including access to global markets and vastly more information on market conditions. As importantly, grain traders are in the business of adding value to primary commodities, whether they are fattening animals or turning corn into ethanol. Cheap grain then becomes an input and the companies are happy to keep those prices low. The structure of those supply chains, as well as the rules that govern them, favor agribusinesses with global reach. Corporate concentration in nearly every sector of agricultural inputs, production, processing and distribution has increased substantially over the last 20 years, including vertical consolidation within supply chains[10].

Conclusions

Dumping can be devastating for farmers in importing countries, especially in low-income countries with little power to defend their markets. It is also unfair to producers in other exporting countries. The underlying causes include failed agricultural policies in the United States that actively encourage overproduction and fail to limit market concentration, as well as the failure of WTO rules to protect its members from the effects of dumping and other U.S. policy failures.

The need for a better Farm Bill that ensures farmers are paid fairly, builds greater climate resilience and provides consumers with healthier food produced more sustainably, is becoming more apparent and urgent. The increasing focus on over-production and expanding exports takes us in the opposite direction.

The return to dumping of U.S. corn and other commodities by agribusiness at a time when the U.S. government is challenging other countries’ agricultural programs (as the U.S. has challenged China at the WTO or Canada’s dairy program under NAFTA) is hypocritical and clouds the possibility for a successful outcome on necessary reforms. Several U.S. food and farm groups came together in early 2017 to call for a different approach in NAFTA – one that allows countries to countries to “protect their farmers from unfair imports that distort the domestic market, undermine prices and ultimately compromise the economic viability of independent farmers.”[11]

IATP's findings underline the need for a new approach to global trade rules—an approach that respects the obligation on governments to protect food security at home, that respects the complex relationship of food systems to economic development, and, that respects the importance of accountability in domestic politics in rich and poor countries alike. It is a time for strong, clear rules that value more equitable returns to food production and distribution within the supply chain, as well as stable and predictable food prices.

Endnotes:

[1] Murphy, S., Burch, D., & Clapp, J. (2012). Cereal Secrets. Oxford: Oxfam.

[2] Schnepf, Randy, “U.S. Farm Income Outlook for 2017”, February 14, 2017, Congressional Research Service. 7-5700. Washington, D.C. and https://www.ers.usda.gov/data-products/chart-gallery/gallery/chart-detail/?chartId=76952

[3] An earlier version of these calculations was published by The South Centre in January 2017, based on data from fall 2016. These calculations slightly revise those estimates based on updated data.

[4] https://www.ers.usda.gov/data-products/chart-gallery/gallery/chart-detail/?chartId=58426

[5] Schnepf, 2017.

[6] Jeff Wilson and Megan Durisin, “Betting the Farm and Losing: Banks Seek Collateral for Debts,” Bloomberg, November 13, 2016.

[7] Timothy Wise, “Reforming NAFTA’s Agricultural Provisions,” in The Future of North American Trade Policy: Lessons from NAFTA, The Pardee Center, 2009, p. 35.

[8] Jonathan Fox and Libby Haight, eds., Subsidizing Inequality: Mexican Corn Policy since NAFTA, Woodrow Wilson Center for International Scholars, 2010.

[9] Semple, Kirk, Mexico Ready to Play the Corn Card in Trade Talks, New York Times, April 2, 2017.

[10] Hendrickson, Mary and Wilkinson, John and Heffernan, William D. and Gronski, Robert, The Global Food System and Nodes of Power (August 2, 2008).

[11] https://www.iatp.org/blog/201701/principles-of-a-new-us-trade-policy-fo…

[xii] The percent of export dumping is the difference between the full cost of production and the export price, divided by the full cost of production. Sources: Farmer production costs are from USDA Commodity Costs and Returns. Government Support Costs are from OECD Producer Support Estimates Database, which includes the costs of public support attributable to each crop, primarily Farm Bill credit programs Transportation and export prices are based on information in USDA Agricultural Marketing Services Grain Transportation Report Datasets, Table 2: Market Update: U.S. Origins to Export Position Price Spreads.