At this year’s COP28, countries will try again to adopt rules for carbon offset trading, in particular, for removals, under Article 6.4 of the Paris Agreement. The concept of carbon removals is commonly used to describe a range of activities that draw carbon out of the atmosphere and “lock” it away in forests, soils or geological reservoirs. At the same time, policymakers in the European Union (EU) are negotiating similar rules for an EU Carbon Removal Certification Framework (CRCF). The EU is often championed for its progressive climate policies. However, instead of requiring the highest possible standards in the CRCF, the EU risks breaking with a central principle of its long-standing position in international climate negotiations: ruling out the double counting of carbon credits.

What does that mean? Certificates generated under the CRCF could be used by the EU to fulfill both the commitments in its domestic Climate Law and its national contributions to the Paris Agreement (formally described as Nationally Determined Contributions, or NDCs) — and at the same time, companies purchasing certified removals could count those same certificates in their registers to fulfill their own net-zero commitments. The EU would allow counting in multiple registers. The atmosphere is only allowed one register. Breaking with its own position brings into question the EU’s credibility at international climate negotiations.

Reviving and legitimizing a broken climate solution

Carbon offsetting is based on the faulty, distorted assumption that the climate impact of greenhouse gases released into the atmosphere in one place can be compensated by someone elsewhere claiming either to emit less or store more carbon than they would have without the prospect of selling those claimed climate benefits as an offset. Carbon offsetting is the basis of most existing “net-zero” claims and targets. For example, a fossil fuel company can claim to produce “climate neutral oil” by suggesting that its continuing emissions have been “cancelled out” by a carbon offset project elsewhere that temporarily stores more carbon in soils than would have been the case without the offset project.

While numerous scandals this year have damaged the reputation of voluntary carbon market credits and carbon offset projects, policymakers are gearing up to revive a dysfunctional “climate solution” on a national and international level. Recent investigations have shown that most credits used for offsetting, including in the largest flagship projects, are actually “phantom credits.” In other words, the emissions reductions are highly exaggerated. The idea that the global community could offset its way out of the climate crisis has been harshly criticized, in particular by civil society showing that “there is no space for offsets in the IPCC’s remaining carbon budget” and by experts arguing that “carbon offsets are incompatible with the Paris Agreement.”

It is still unclear if and how the plethora of national and international voluntary and compliance markets will interact. Some actors, such as the private sector Integrity Council for the Voluntary Carbon Market (ICVCM), which seeks to improve and standardize the quality of carbon credits verified for sales by private registries, strive to make that connection. ICVCM, for example, claims that its carbon credit standards will align with those of the Paris Agreement.

Here, we outline two significant proposals for carbon trading: Article 6.4 of the Paris Agreement and the Carbon Removal Certification Framework.

Parallel negotiations of Article 6.4 and the EU CRCF

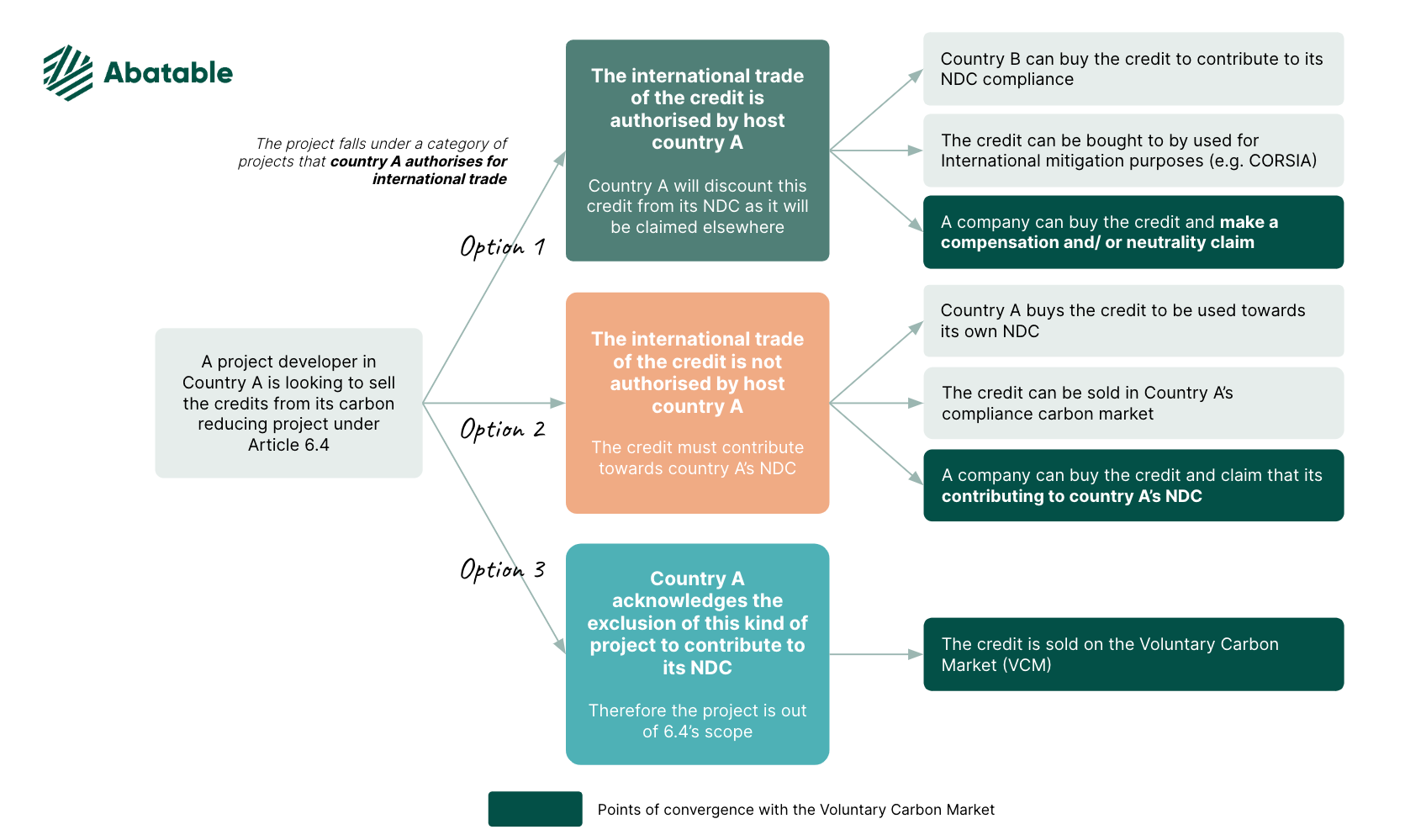

Since the Paris Agreement came into force in 2016, governments have negotiated under the auspices of the United Nations Framework on Climate Change (UNFCCC) different aspects of the treaty’s Article 6. This article is meant to set up mechanisms for voluntary cooperation between national governments, as well as other stakeholders, such as companies. Two of the mechanisms under Article 6 are market based and set up rules for carbon trading. Controversial from the beginning, the negotiations of Article 6 have been extended over many years. One of the mechanisms, Article 6.4, establishes rules for carbon trading between a signatory country and an actor outside of the treaty, such as any private sector company. When it goes into effect, it will likely mimic the model of existing voluntary carbon markets on which companies or individuals can buy carbon credits (based on carbon removal or emissions reductions) to claim they are offsetting their emissions. Article 6 is premised on the assumption that making decarbonization cheaper by financing mitigation projects in other countries (often projects for temporary carbon sequestration in forests) will lead to countries raising the level of their NDCs to global mitigation ambition.

Currently, a Supervisory Body is tasked with making recommendations on the rules and implementation of Article 6.4 to the delegates at COP28.

In the meantime, EU policymakers are negotiating the CRCF, a new policy framework for the EU that would establish rules for the quantification and certification of carbon removals (and some emission reductions). The CRCF would create “certified units” that could be used for various purposes, including for trade as offsets on voluntary carbon markets, and to achieve compliance climate targets for the EU in the future. The European Parliament and the Council have just concluded their position on the CRCF and will start the final negotiations with the European Commission in the upcoming weeks and months.

Double counting, double claiming, double use = double cheating

Carbon markets have been criticized for many issues that undermine the environmental integrity of these mechanisms. Critics emphasize that offsetting is incompatible with the Paris Agreement. All the problems connected to offsetting become even more critical if the same mistake is made twice. A fundamental rule for offsetting is that the supposed climate benefit reflected in a carbon credit can only be counted or claimed by one actor. This means that if, for example, one country sells offset credits to another country under the Paris Agreement, the selling country could no longer claim the climate benefit in its own NDC report to the UNFCCC. For that reason, so-called “corresponding adjustments” have been introduced in the Paris Agreement to ensure that the climate benefit claimed for the offset is subtracted from the registries of the selling country.

While many different terms are used to describe the problem — including double claiming or double use — double counting can be broadly defined as “a single GHG emission reduction or removal, achieved through a mechanism issuing units, [being] counted more than once towards attaining mitigation pledges or financial pledges for the purpose of mitigating climate change.”

There are various forms of double counting. In addition to two countries counting units towards both of their NDCs, double counting can also occur with climate pledges at different levels, such as by companies.

For example, a country promises to achieve a certain target to increase emissions sequestration in the land sink for its NDCs. The country also hosts a private project that scales up reforestation, which could result in carbon sequestration in the forestry sector. That country’s government would want to count the sequestration towards its land sink target. At the same time, the project developer would want to sell the sequestration in the form of offsets to another company that may or may not operate in the country where the project takes place. The resulting benefit might thus be used simultaneously by both the country to fulfill its land sink target and by the buyer of the credits from the reforestation project.

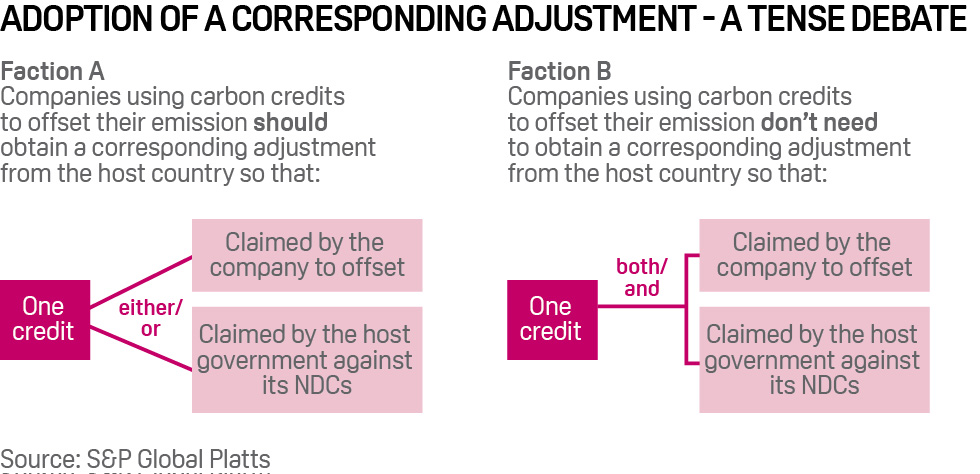

What does the EU say about double counting in Article 6.4?

In the international climate negotiations, the EU has long objected to double counting. In its 2022 submission to the Supervisory Body on Article 6.4, the EU stated that “the mechanism can be used either for compliance (e.g. towards NDCs and CORSIA) – more on CORSIA below – or not for compliance (e.g. for results based finance or domestic carbon markets),” implying that carbon credits could either be used by a country to fulfill its NDC or for other purposes, such as companies claiming the offset in their company registries — but not both.

Later, the EU position emphasized that Article 6.4 must clarify early how the carbon credits can be used by the countries in which the projects take place, by the project developers as well as the buyers. For that reason, Article 6.4 should define “how emission reductions are shared between buyers and the host country, in order to enable the host country to use part of the achieved emission reductions to achieve its own NDC.” The EU affirms that “to ensure that host Party action is not undermined, it is important that mitigation outcomes, including removals, be shared between the host country and the users of the Article 6.4 emission reductions.”

Together, these statements convey that a unit certified under Article 6.4 of the Paris Agreement could not be counted towards a host country’s NDCs and also on the register of the buyer, e.g., a private company, at the same time. Instead, the two parties would need to split the “climate benefit,” also called “mitigation outcome” in UNFCCC speak. For example, a project would lead to the sequestration of 100 tonnes of CO2 equivalents, but only 50 tonnes are credited and can be used by the buyer and the host country needs to apply a corresponding adjustment in its national inventories. The remaining 50 tonnes cannot be purchased but are tallied in the emissions inventory of the host country.

What does the EU say about double counting in the CRCF?

The EU’s position on Article 6.4 stands in stark contrast to the current developments of the EU’s CRCF. While the final agreement has yet to be reached, positions of EU decision-making institutions indicate what the final rules might look like. The EU declared an economy-wide climate neutrality target for 2050 (balancing emissions and removals), and its approach to climate policy attempts to cover all sectors and greenhouse gas emissions. This includes a specific legally binding target for the land sector to increase carbon sequestration on land to -310 million tonnes CO2eq by 2030.

As the EU struggles to achieve that target, the European Commission’s original proposal, published in November 2022, suggests that the CRCF would enable the EU “to channel more effective and result-based support toward carbon farming activities that can contribute to the achievement of this target.” By allowing the trade of CRCF units as offsets, the Commission could finance its land sinks targets through private offsetting — thus enabling the counting of climate benefits both in its EU registers and in corporate climate claims.

The Council — made up of representatives of EU national governments — echoes the Commission’s proposal in its positionadopted on November 17, stating that the CRCF “will be instrumental in meeting the Union climate change mitigation objectives set in international agreements [such as the Paris Agreement] and in Union law, while avoiding double counting.” While paying lip-service to the aim of ruling out double counting, the Council also reiterates that the CRCF certificates can be used for different purposes, including “national and corporate register and corporate GHG inventories, including with regard to the LULUCF Regulation [EU Regulation on land, land use change and forestry], the proof of climate-related and other corporate claims (including on biodiversity), or the exchange of certified units through voluntary markets.” There is no addition to the legal text that would rule out double counting in national and private registers.

On November 21, the European Parliament adopted its position, agreeing on the recommendations made by its environment committee. The text suggests that: “All removals, sequestration and emission reductions generated under this Regulation shall contribute to achieving the Union’s nationally determined contributions (NDCs) and climate targets and objectives as set out in [the European Climate Law] and shall not contribute to a third country’s NDC.” It further elaborates that “a certified unit shall not be used or claimed by more than one legal or natural person at any point in time.” A legal or natural person would be “undertakings or public authorities other than a Member State, like city councils or communes.”

The positions on the CRCF permit the assumption that EU policymakers would want to count all removals and reductions certified under the CRCF towards EU-wide targets. The EU accounts substantiate the EU’s NDC claims. At the same time, they don’t explicitly exclude the possibility of private sector companies (operating inside or outside the EU) purchasing CRCF certificates and using them to substantiate their own company-wide climate claims.1 Thus, even if the certified credits have a positive impact, the overall climate impact could be overstated by being counted in multiple registers.

Article 6, CORSIA and the CRCF

One particularly important case study on double counting is international aviation. While domestic flights within the European Economic Area (EEA) — the EU, Iceland, Liechtenstein and Norway — are covered by the EU’s compliance market, international flights are supposed to be addressed under the CORSIA scheme (Carbon Offsetting and Reduction Scheme for International Aviation) of the International Civil Aviation Organization (ICAO). This means that national emissions inventories do not cover aviation emissions from flights originating in the EU but ending outside the EU.

It is logical that a country must adjust its national inventory if a credit generated, e.g., through a reforestation project in that country, is sold to airlines. Although Article 6 requires the avoidance of double counting between NDCs and CORSIA, the watchdog Carbon Market Watch concludes that there is, in fact, a particular risk of double counting of carbon credits in a country’s NDC and in CORSIA. In the case of the CRCF, this could amount to a clear case of double counting: The EU could address international aviation emissions under CORSIA by using CRCF certificates to meet its CORSIA commitments. At the same time, the EU could use a CRCF certificate to meet its domestic NDC, e.g., for its land sink targets.

The purpose of voluntary carbon markets

The original premise of voluntary carbon markets was that they would increase emissions reduction ambition beyond what was already promised by governments. The idea, implemented through the additionality principle, was that voluntary carbon markets would spark climate action that would not have happened without the carbon credit project and investment. Proving additionality has turned out to be an impossible task.

Since under the Paris Agreement not all countries have pledged economy-wide emissions reduction targets that encompass all greenhouse gas emissions, voluntary carbon markets and Article 6 were promoted to fill these gaps of climate action. As such, experts have concluded that “double counting with voluntary actions could undermine global efforts to reduce GHG emissions.” The role of the voluntary carbon market becomes increasingly difficult to define as countries, including the EU, are moving towards economy-wide climate targets.

A 2020 report of the German Environmental Agency found that “double claiming” of countries and private actors is a critical issue determining the effectiveness of voluntary carbon markets. The report suggested various options to address the problem, including the use of corresponding adjustments, only generating credits for activities outside of the NDC scope or limiting the emission reduction claim to the host country. The report concluded that “the climate impact can therefore not be guaranteed without imposing the measures to avoid double claiming set out above.”

Assessing double counting rules in the sphere of carbon removal policies, scientists found that none of even the most ambitious initiatives “addresses the challenge of double-counting of removals at the company and national level.” They explain that “double claiming of the same mitigation outcome toward both the private sector actor's carbon neutrality target and the host country's NDC would effectively render the private sector actor's carbon neutrality claim untrue. This is because, in case of mitigation outcomes counted toward the host country's NDC, the private sector actor effectively subsidizes the achievement of mitigation levels that the country was committed to achieving anyway.” They further state: “It is important that private sector support for CDR is recognized as complementary to public CDR policy, rather than a substitute or justification for postponing public action.”

What does the carbon market industry say?

While double counting at the same level, for example between two countries, is widely considered unacceptable, double counting at different levels, e.g., a country and a company, is still controversial.

Proponents of voluntary carbon markets argue that it is not double counting if a country and a company both claim a carbon credit because their pledges operate at different levels. A company’s claims would, for example, not be counted under the Paris Agreement, but they would be indirectly part of countries’ inventories. Initiatives like the Voluntary Carbon Markets Integrity Initiative (VCMI) have also recommended how buyers of carbon credits can manage double counting and corresponding adjustments. VCMI states that a carbon credit used by a company can be counted twice as the credits “represent a contribution towards both a company’s climate goals and towards the collective global effort to reach net zero.”

In contrast, carbon credit providers, such as Gold Standard, have updated their rules on double counting to avoid cases in which a company and a country claim the same climate benefits. Similarly, an analysis for a carbon offsetting platform concludes that there would be differences concerning which claims a company will be able to make when buying a carbon credit under Article 6: The only credits that could be claimed as offsets would be the ones that have not been authorized by a project’s host country to contribute to its NDC.

The carbon offset credit provider atmosfair describes the problem in a similar way. It states that if a company and a country would both claim emissions reductions, that would lead to “double claiming,” and even if, for example, a company would only claim the financial contribution to the emission reduction, that claim may result in less finance for mitigation activities provided by a country, and hence an overall loss for CO2 reductions and ambition. The offset credit provider Compensate emphasizes that “if a company claims to be carbon neutral through offsetting that is also counted into the project’s host country goals, as far as the climate is concerned, the company hasn’t actually done anything extra,” i.e., no “additionality” in Paris Agreement terms.

Should the EU move forward with its approach to double counting in the CRCF, it would contradict an important principle of offset projects justified by its search of finance. The CRCF would set a dangerous precedent that could have significant knock-on effects for international negotiations on Article 6.

It is highly questionable how the EU would convince countries in the Global South to agree to rules to avoid double counting in Paris Agreement market mechanisms, while the EU allows the practice in its own domestic policies. Many offset projects occur in countries in the Global South. These countries could have their NDCs adjusted when international financiers like the UAE company Blue Carbon sell carbon offset credits from managing forests in Liberia (if the rules suggested by the EU on Article 6.4 were to apply), while the same taking place in the EU under the CRCF could be allowed.

Relabeling double counting as “co-claiming,” as proposed in the CRCF, would redefine the role of voluntary carbon trading from an action that brings about alleged additional climate action to action that has already been promised. Double counting is only one of the myriads of problems that carbon market bring with them, which we have addressed elsewhere. Instead of betting on voluntary contributions with questionable effects, policymakers should focus instead on:

Investing in decarbonization and resilient economies;

Phasing out subsidies for polluting industries;

Implementing effective regulation of big polluters to cut real emissions at their source.

IATP will monitor closely negotiations at the EU and international level on carbon trading. COP28 could be a decisive moment for setting Article 6.4 rules. Negotiators must be careful not to sacrifice environmental integrity at the international or regional level to generate finance that will not bring about the promised contribution to climate action.