Lire Le Piège des Engrais en français. Lea La Trampa de los Fertilizantes en español.

KEY FINDINGS

- The cost of chemical fertilisers in both the global North and South has skyrocketed over the past two years and is putting severe economic strain on farmers’ and public budgets.

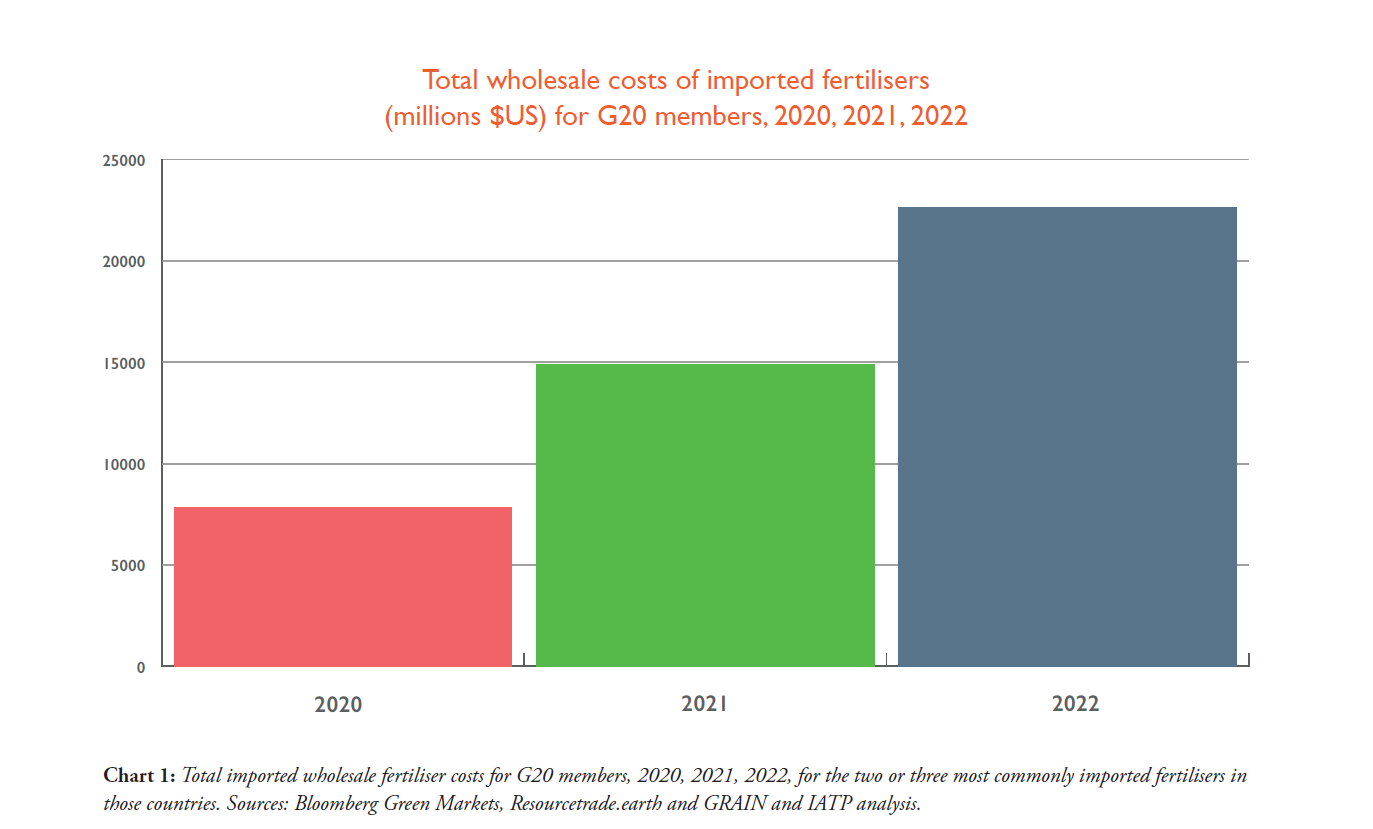

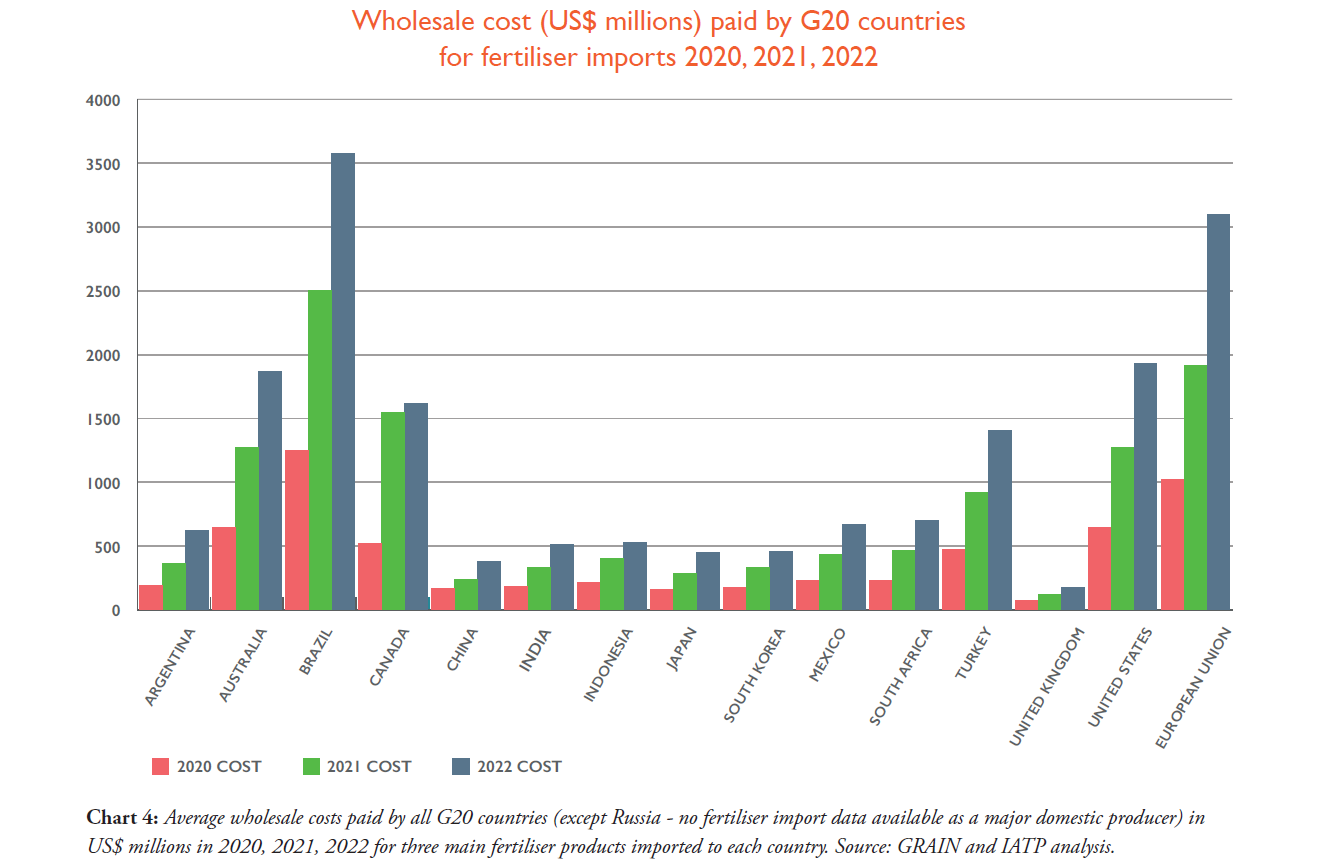

- G20 nations paid almost twice as much for key fertiliser imports in 2021 compared to 2020 and are on course to spend three times as much in 2022 — an additional cost of at least US$ 21.8 billion. For example, the UK paid an extra US$ 144 million for fertiliser imports in 2021 and 2022, and Brazil paid an extra US$ 3.5 billion.

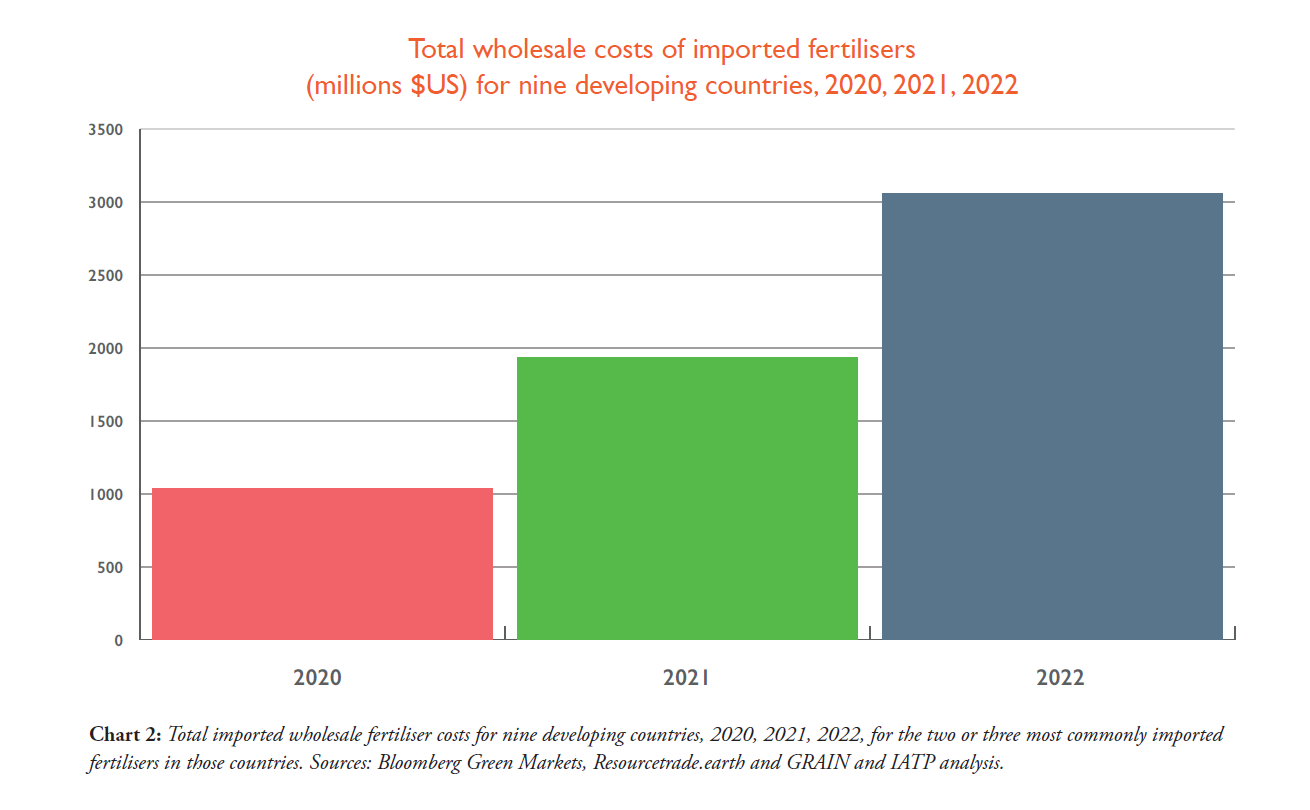

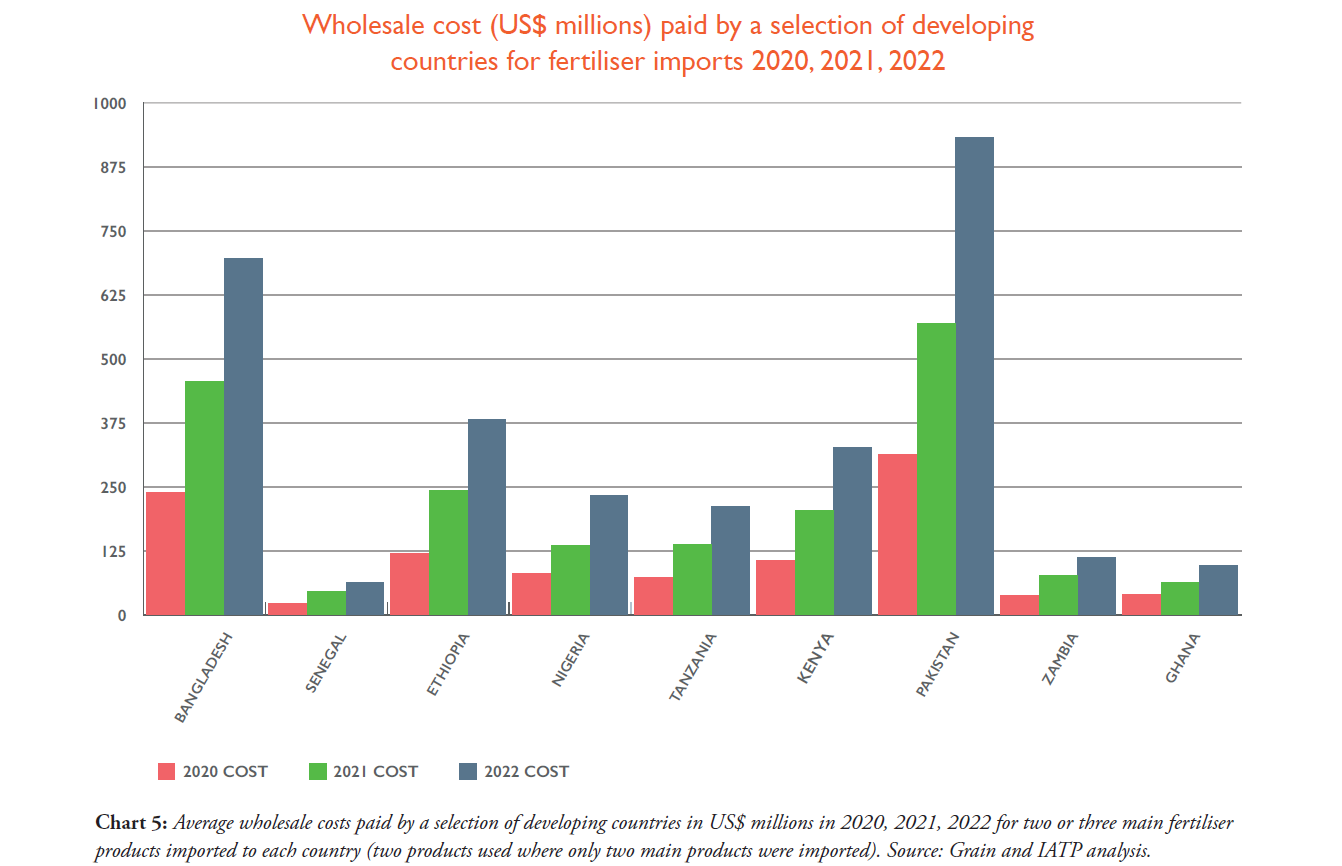

- Nine developing countries are on course to pay three times more in 2022 than they did in 2020. These countries include Pakistan, which paid an extra US$ 874 million, and Ethiopia, which paid an extra US$ 384 million in 2021 and 2022.

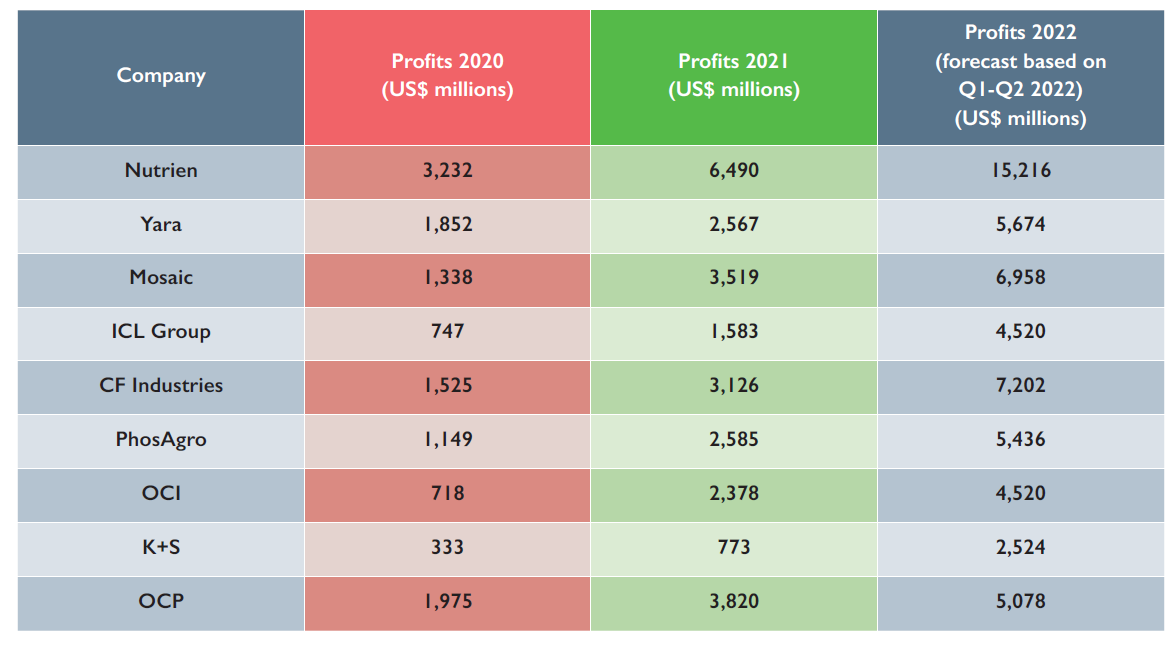

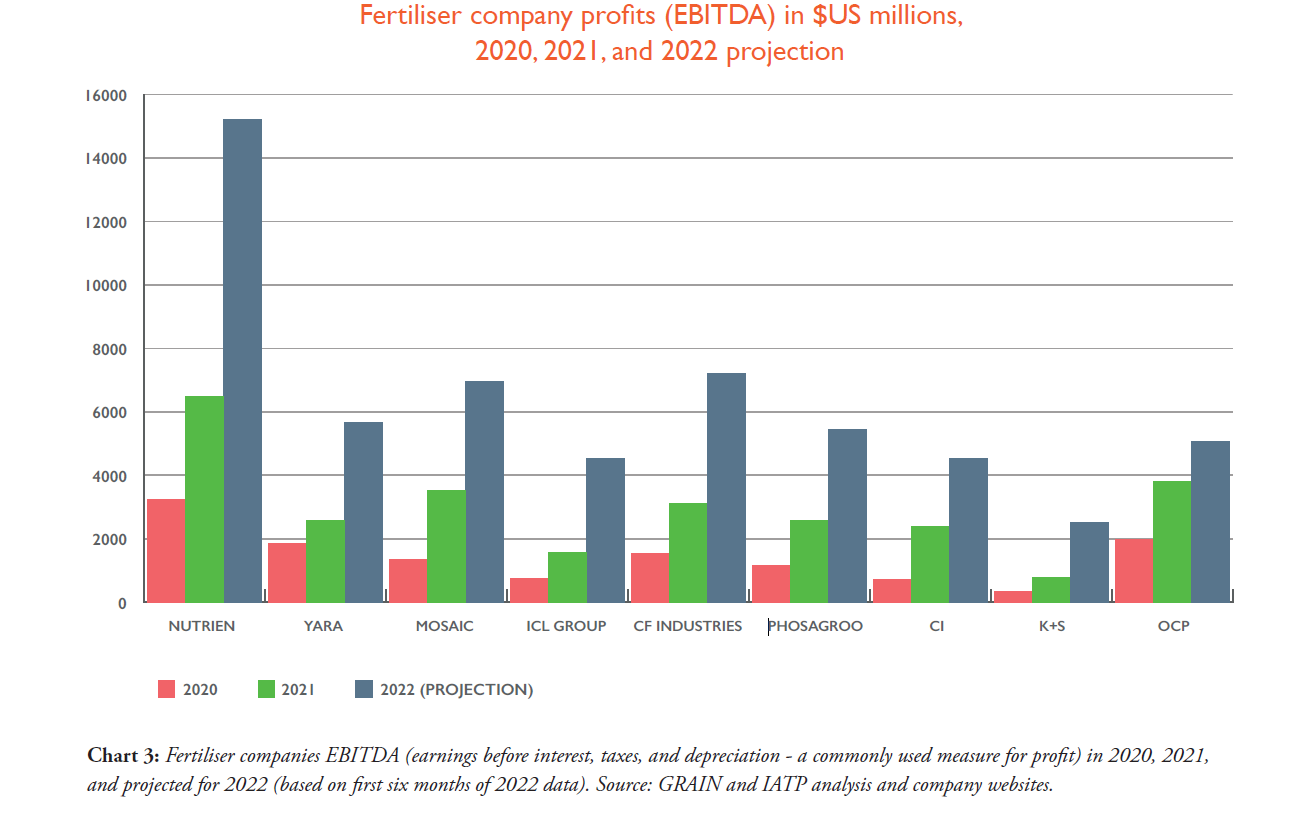

- The world’s largest fertiliser companies are making record profits as farmers struggle to cope with increased prices. Nine of the world’s largest fertiliser companies are expected to make US$ 57 billion in profit in 2022, up more than fourfold from two years ago; their profits in 2021 and 2022 are on course to come to a total of US$ 84 billion.

- Actions must focus on reducing the consumption of chemical fertilisers and supporting alternative technologies — not increasing production. This will cut costs, and the damage which chemical fertilisers cause to the environment and the climate.

INTRODUCTION

The global food system is addicted to chemical fertilisers. For the past 50 years, these fertilisers have been heavily promoted by global institutions, governments and agribusiness as the means for increasing crop yields, while other options for increasing soil fertility and food production have been ignored or undervalued. As a result, worldwide use of chemical fertilisers has increased tenfold since the 1960s.1 Some credit chemical fertilisers for enabling global food production to keep up with population growth, but their use has come at a high cost.

Chemical fertilisers are, today, major sources of water and air pollution. Overuse is widespread and an important cause of soil health degradation; proper use requires support and extension services that are rarely available.2 Chemical fertilisers account for 2.4% of global emissions, or one out of every 40 tonnes of global greenhouse gas emissions.3

This year, the bill for these energy-intensive products has hit new heights. With the world in the midst of an energy and climate crisis, prices for chemical fertilisers are at record levels. Fertiliser corporations are using their market power to capture mega profits, while farmers and governments are scrambling to try and cope with the added costs, especially in the global South. High fertiliser prices are putting food production at severe risk in many places. In early October 2022, the United Nations warned that, if immediate action is not taken to bring fertiliser prices down, there could be a global shortage of food.4

The response so far from many governments is to look for ways to increase chemical fertiliser production. Not surprisingly, this is also the solution that the world’s largest fertiliser companies are promoting. When the G20 nations meet in Bali, Indonesia in November 2022, increased global fertiliser production is expected to be a major part of the agenda. In fact, the French President Emmanuel Macron plans to convene a preparatory meeting with the CEOs of the leading fertiliser companies ahead of the G20 gathering to find ways “to scale up production as fast as possible”.5

But increased production of chemical fertilisers will not resolve this crisis. The era of cheap fertilisers is over, and the costs have become too much to bear — both in terms of the financial burden for farmers and public budgets, the severe environmental and health impacts, and the long-term risks to food security. While some short-term actions can be taken to cut waste and address excess profit taking by fertiliser companies, it is critical that governments focus on reducing consumption in the long-term, including programmes to support farmers to transition towards environmentally-sound and more cost-effective alternatives.

HOW HIGH AND FAST ARE FERTILISER PRICES RISING?

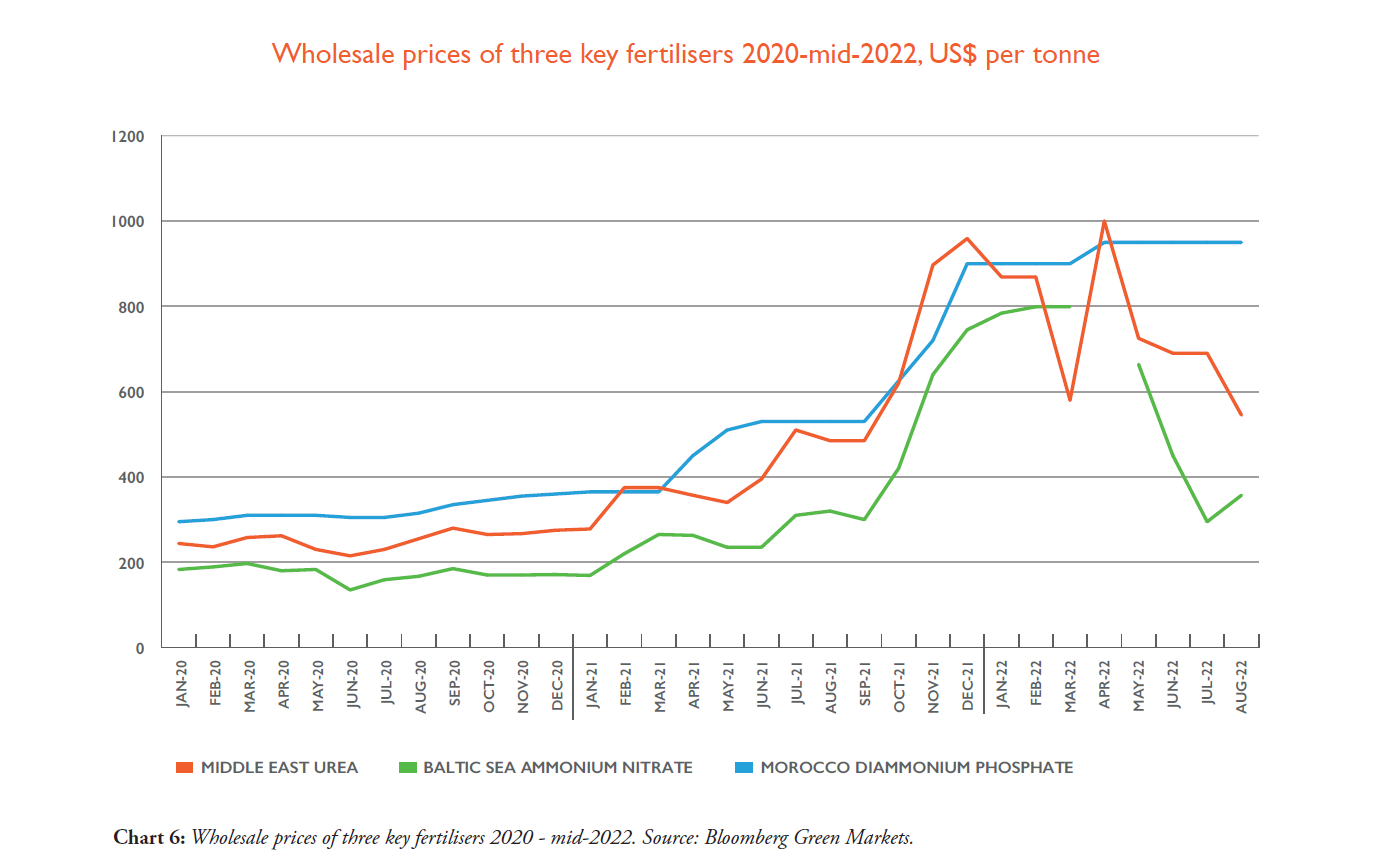

A combination of factors, including the high cost of natural gas, the war in Ukraine and the oligopoly power of fertiliser companies, have caused prices for chemical fertiliser to double and in some cases even triple in the last two years.6 For example, in January 2020 Canada was paying US$ 225 for a tonne of urea from the Baltic, and by January 2022 it was paying US$ 814. Likewise, in January 2020 Mexico was paying US$ 280 for a tonne of diammonium phosphate from the US, and by January 2022 this had risen to US$ 810.7

To better understand the impact of these rising prices, we examined the wholesale costs of the three fertilisers imported in the greatest quantities to the G20 and a sample of developing countries for which data was publicly available (see Annex I for more detail about our methodology). Domestic costs and domestic production are not analysed because the data is not as readily available. This means that our findings only tell part of the story — the full extra global cost to governments and farmers is even higher than the numbers we show.

From our calculations, we estimate that G20 members (Argentina, Australia, Brazil, Canada, China, EU (including France, Germany, Italy), India, Indonesia, Japan, South Korea, Mexico, South Africa, Turkey, the UK and the US) paid at least US$ 21.8 billion extra for the three chemical fertilisers they import in the greatest quantities over 2021 and 2022, compared to 2020 prices. For these G20 members, this meant a 189% increase in costs for the sample of imported fertilisers in 2021, and on course for a 288% increase in 2022.

The developing countries sampled (Ghana, Ethiopia, Pakistan, Senegal, Kenya, Bangladesh, Zambia, Tanzania and Nigeria) together spent 186% more in 2021 and 295% more in 2022 for the same sample of fertilisers (a total extra bill of US$ 2.9 billion).

WHY ARE COSTS RISING?

The initial price increases in 2021 were driven by the rising cost of natural gas, which is a key raw ingredient for nitrogen fertilisers. After falling back slightly in early 2022, there was another sharp increase due to the war in Ukraine which constrained the supply of both gas and fertiliser itself — Russia supplies 45% of the ammonia nitrate market.8 Russia and Ukraine are both significant exporters of phosphorus fertilisers, and Russia’s ally Belarus a major exporter of potassium fertilisers.9 Prices fell back slightly after the initial invasion before climbing again in the summer as it became clear the war would not end quickly and concerns over medium-term gas shortages in Europe returned. The costs of fertilisers in both 2021 and 2022 have been far higher on average than in 2020.

Some chemical fertilisers are not made from gas but from mineral deposits, such as potash and phosphate. However, the mining and production of fertilisers using these minerals is highly energy intensive and, therefore, still affected by the price of gas. These deposits are also highly concentrated geographically — 70% of the world’s phosphate reserves are in Morocco and the Western Sahara,10 while 75% of the world’s potash production comes from China, Canada, Russia, and Belarus.11

Given that fossil fuels prices are expected to become more volatile and their supplies more constrained as measures to fight climate change are implemented, prices of fertilisers are likely to remain high for years to come.

But there is another factor fuelling fertiliser prices: corporate profits. The US$ 200 billion global fertiliser market is controlled by a handful of companies — just four of these companies control 33% of all nitrogen fertiliser production.12 For example, the National Farmers’ Union in the UK has expressed concern about CF Fertilisers’ monopoly over the UK fertiliser market.13 Meanwhile in the US, Mosaic is estimated to control over 90% of the domestic phosphate fertiliser market.14

Given their market power, these companies have so far been able to pass on the increased costs of their raw ingredients and production processes to maintain or even increase their profit margins.15

According to company filings, the combined profits of nine of the world’s biggest fertiliser companies (Nutrien, Yara, Mosaic, ICL Group, CF Industries, PhosAgro, OCI, K+S, OCP) were just under US$ 13 billion in 2020. In contrast, if their reported profit levels in the first six months of 2022 are maintained, then over the whole year they will earn more than US$ 57 billion in profits, 440% of their 2020 profits. This is 30 times the US$ 1.9 billion due to be paid by US farmers for fertiliser imports in 2022. The biggest fertiliser companies’ 2022 profits are on course to be twice the entire GDP of Senegal, which saw its costs for the imported fertilisers analysed by this report more than double from 2020 to 2022.

Some companies, especially in western Europe, have reduced production, or closed temporarily due to high gas prices.16 But a few weeks’ closure or reduced production is likely to dent, rather than completely wipe out, major profits this year and should not distract regulators from the fact that the industry is dominated by global corporations which are making far larger profits than usual despite interruptions to production in some locations.

There is some evidence that fertiliser prices are fuelling food prices by increasing the cost of production or reducing yields as farmers cut the amount of fertiliser they apply or the area of land under production. In Zambia, for instance, high fertiliser prices are being blamed for contributing to food price inflation, which reached 353% in August 2022 compared to August 2021.17

In the UK, it is estimated that farmers will have paid an additional £1.1 billion in total fertiliser costs from 2020-2024 (assuming that gas prices remain high and keep fertiliser prices high).18 In Canada, grain farmers have seen costs of fertilisers double from CAN$ 65 to CAN$ 140 per acre between 2021 and 2022.19

Across the world, from Pakistan to Ethiopia and Ecuador, farmers are protesting to demand that governments take action to reduce fertiliser prices. But the rising prices are straining government reserves and budgets, making it difficult for governments to even maintain their existing fertiliser subsidies.20 Ghana, for example, had to scale back its fertiliser subsidy scheme, reducing the total amount of fertiliser covered by the scheme from 450,000 tonnes to just 150,000 tonnes.21

Governments like Kenya and the Philippines, which have stepped in with new subsidies risk racking up large debts and depleting their public budgets.22 The Indian fertiliser subsidy budget — currently around US$ 26 billion — is now predicted to fall far short of what is needed.23 The US Department of Agriculture has launched a fertiliser expansion programme, recently announcing US$ 500 million in grants to expand domestic production.24

Some G20 countries, such as the US, have suggested that the solution to the fertiliser crisis is to increase supplies of natural gas and develop more production facilities at home and in developing countries.25 A key outcome of the Leaders’ Summit on Global Food Security at the UN General Assembly in September 2022 was a pledge to increase chemical fertiliser production.

European fertiliser companies are lobbying hard for actions by their governments to ensure they have “affordable” access to natural gas at a time when supplies within Europe are severely constrained.26 They say this is necessary to protect domestic production from imports and to keep their factories in operation.27 While the European Commission has announced it will be issuing a communication on fertilisers that will focus both on measures to increase domestic production and reduce the use of fertilisers in agriculture, some governments within the EU appear to be already siding with the fertiliser lobby.28 French President Emmanuel Macron, for instance, has announced he will host a meeting in Paris with the CEOs of the top fertiliser companies prior to the G20 meeting in Bali in November “to scale-up production as fast as possible.”29

It would be simpler and more cost effective for governments to focus instead on reducing fertiliser consumption and reining in corporate profits to immediately reduce costs to farmers. Building new factories and ramping up production will take time and is unlikely to have an immediate impact on supply or prices. Nor will it do anything to dismantle the market power of the corporations that control the sector, effectively leaving fertiliser consumers as price-takers in the market.

The more fundamental problem with a focus on production is that it shifts attention from the pressing need to dramatically reduce reliance on chemical fertilisers. Chemical fertilisers are a leading cause of the climate crisis, with nitrogen fertilisers alone being responsible for 2.4% of all global greenhouse gases.30 Chemical fertilisers are also responsible for loss of soil health, ozone depletion, biodiversity loss, air pollution, impacts on human health and the transgression of multiple planetary boundaries.31 The current fertiliser price crisis must be addressed by actions that ease the climate crisis and these other vital environmental issues, contributing to a more resilient future.

WHAT CAN BE DONE?

The huge profits that fertiliser companies are making should be dealt with urgently. Some ideas that have been suggested include the imposition of windfall taxes and investigations into pricing.32

Governments should take urgent action to support a significant reduction in the consumption of chemical fertilisers. In countries where industrial agriculture is dominant, one of the most immediate and impactful steps that can be taken is public support for farmers to implement more efficient fertiliser use. In these countries, a large amount of fertiliser is over-applied and wasted. The excess evaporates or is washed away, polluting air, soils and water. In Germany, one study found that only 61% of fertiliser is reaching wheat crops, meaning 39% is wasted.33 In Mexico just 45% of fertiliser reaches crops, in Canada only 59%, and in Australia 62%.34

In many places, farmers are already demonstrating that they can transition away from the use of chemical fertilisers as part of a broader transition to agroecology, without sacrificing their yields (see Box 1).35 Agroecology incorporates traditional knowledge with science, empowers farmers as actors in their markets, focuses on delivering varied and healthy food, and works with biodiversity and nature.36 With agroecology, instead of chemical fertilisers, farmers restore nutrients and fertility to soils through the use of manure or through the cultivation of plants that absorb nitrogen from the atmosphere, such as legumes. These farming practices also do less damage to soils in the first place.

Agroecology receives very little of the international and national government finance given to agriculture compared to industrial agriculture which receives the vast majority of funding.37 To make a transition away from chemical fertilisers, farmers need public support. Abrupt, top-down bans on chemical fertilisers, such as those in Sri Lanka in 2021, invite failure.38 The Sri Lankan government introduced a sudden ban on chemical fertilisers in an attempt to address a sovereign debt crisis and reduce spending of foreign exchange. With no time to prepare, even those farmers and groups that had advocated a gradual transition to organic farming39 were badly affected. The problem is not with farming that relies on less or no use of chemical fertilisers, but with the failure to provide any transitional support.40 It is also important to understand that, as price-takers in commodity markets, farmers are very vulnerable to changes in access to the inputs they rely on, as well as to changes in input prices. Addressing farmer concerns is critical to build confidence and avoid strong political opposition, as happened in the Netherlands over recent changes to fertiliser policies.41 As noted by the International Panel of Experts on Sustainable Food Systems: “Farmers cannot simply be expected to rethink their production model… without a major shift in the incentives running through food systems.”42

The world can no longer afford the food system’s addiction to chemical fertilisers. The costs are too high, both in terms of the financial burden for farmers and public budgets, and the severe environmental and health impacts. Governments urgently need redirect public funds and policies away from industrial agriculture and towards agroecological farming.

THE EVIDENCE ON FARMING WITHOUT CHEMICALS

Agroecology — which does not involve the use of chemical fertilisers — is often criticised for reducing food production. However, there is a growing body of research showing how agroecology provides “immense economic, social and food security benefits while ensuring climate justice and restoring soils and the environment.”43 Some examples include:

- Thirty farm studies across Europe and Africa have shown that yields can be maintained or even increased if fertilisers are replaced with agroecological farming methods.44

- In 57 nations, agroecological projects45 covering 37 million hectares (equivalent to 3% of the total cultivated area in these countries) were shown to increase average crop yield by 79%, as well as land productivity on 12.6 million farms.46 In Africa,47 farmers had even higher gains with average crop yields rising by 116%.48 In Andhra Pradesh, India an agroecology programme now involving 700,000 farmers has resulted in no negative impact on yields.49 In Malawi farms that use agroecological techniques are up to 80% more productive.50

- An analysis by the Royal Society of 1,000 observations across 115 studies around the world found that using crop rotation in organic farming could minimise the difference in yields compared to conventional farming to just 4%.51

- In the Drôme Valley in central southern France, farmers have been developing organic production methods since the 1970s. The region is home to livestock, fruit, cereal, poultry and wine production. In the 1990s, several cooperatives were established to share organic practices, and today 40% of farmers in the region are organic, the highest level of any French département.52

- In Mexico, the Asociación Nacional de Empresas Comercializadoras de Productores del Campo (ANEC) supports its members to adopt agroecological farming practices.53 By 2017, there were 1,617 farmers in Mexico using these practices, reporting falls in their bills for inputs, and 30-50% increases in yields.

- Seven case studies of agroecological transitions from Europe, North America, Central America, Africa and Asia reported on by the International Panel of Experts on Sustainable Food Systems show that it is possible for communities, regions and whole countries to fundamentally redesign their food and farming systems.54

RECOMMENDATIONS

The evolving fertiliser crisis cannot be addressed through increased chemical fertiliser production. Actions that can be taken to reduce costs for farmers and protect future food production include:

- Measures, including a change in subsidies, which support a managed transition towards farming practices that significantly reduce or eliminate the use of chemical fertilisers.

- Coordinated efforts to rapidly ramp up the production on non-chemical fertilisers and expand agroecological farming.

- The termination of public or private philanthropic programmes that support the introduction of fertilisers into farming systems which are not already dependent on their use.

- Initiatives to prevent profiteering by fertiliser companies.

ANNEX 1

This analysis examined the wholesale costs for chemical fertilisers. It looked at the three to four most commonly imported fertilisers for each country.

Wholesale costs on a range of global markets are collected by Bloomberg Green Markets (https://fertilizerpricing.com/), making this data readily accessible up to August 2022 (at time of writing). Retail costs within countries are not collected in the same way.

Therefore, instead of focusing on domestic production, this analysis looked at fertiliser imports to the sample countries from key global markets.

Resourcetrade.earth (https://resourcetrade.earth/), a Chatham House tool, provides commodities import data up to 2020, including for chemical fertilisers. This was used as the source for import data for each fertiliser product for each country in the sample.

More recent trade data per fertiliser product was not available, so it was assumed that imports in 2021 and 2022 would be similar to 2020, but using 2021 and 2022 wholesale cost data from Bloomberg Green Markets.

The wholesale cost was calculated by averaging the cost in each month across the year. For 2021 and 2022, this was using 12 months, for 2022 the average cost for the whole year is assumed to be the average of the cost in the first eight months of the year.

For some countries that are major fertiliser producers, imports only represent a small proportion of their total application of chemical fertilisers. However, domestic production and cost data were not easily available.

This means that the figures on extra costs in 2021 and 2022 are likely to be a significant underestimate for the countries sampled.

The following G20 members were in the sample: Argentina, Australia, Brazil, Canada, China, India, Indonesia, Japan, Mexico, Republic of Korea, South Africa, Turkey, the UK, the US, the EU (which also includes France, Germany, Italy, but these countries’ imports were not counted separately to avoid double-counting). Russia and Saudi Arabia were not included in the G20 sample because, as major producers of fertilisers, both countries import very low quantities of fertiliser.

The following countries were in the developing countries sample: Bangladesh, Senegal, Ethiopia, Nigeria, Kenya, Tanzania, Pakistan, Zambia and Ghana.

For each country, three different fertiliser products were chosen based on those most commonly imported into that country for which price data was also available from Bloomberg Green Markets (according to 2020 data from Resourcetrade.earth). In two cases (Senegal and Ethiopia), only two fertilisers were imported in any significant quantity).

Fertiliser profit data came from the websites of the companies:

Nutrien: https://www.nutrien.com/investors/news-releases/2022-nutrien-delivers-record-first-half-earnings-and-expects-strong-second

Yara: https://www.yara.com/investor-relations/latest-quarterly-report/

Mosaic: https://investors.mosaicco.com/financials/quarterly-results/default.aspx

ICL: https://s27.q4cdn.com/112109382/files/doc_downloads/ICL-2Q%2722-Earnings-Slides-and-Appendix-FINAL.pdf

CF Industries: https://cfindustries.q4ir.com/news-market-information/press-releases/news-details/2022/CF-Industries-Holdings-Inc.-Reports-First-Half-2022-Net-Earnings-of-2.05-Billion-Adjusted-EBITDA-of-3.60-Billion/default.aspx

OCP: https://ocpsiteprodsa.blob.core.windows.net/media/2022-09/Consolidated%20IFRS%20Financial%20Statements%201H%202022.pdf

PhosAgro: https://www.phosagro.com/press/company/phosagro-reports-operating-and-financial-results-for-1h-2022/

OCI: https://www.oci.nl/media/2097/oci-nv-q2-2022-results-report_vf.pdf

K+S: https://www.kpluss.com/.downloads/ir/2022/q2-2022/kpluss-h1-2022-half-year-financial-report.pdf

2020 and 2021 EBITDA figures are actual, 2022 12-month figures are projections based

on the first six months of the year.

Full data tables can be provided on request to [email protected]

ENDNOTES

1 Carbon Brief, 2022, Q&A: What does the world’s reliance on fertilisers mean for climate change?, https://www.carbonbrief.org/qa-what-does-the-worlds-reliance-on-fertilisers-mean-for-climate-change/

2 Singh, B., 2018, Are Nitrogen Fertilizers Deleterious to Soil Health?, https://www.researchgate.net/publication/324520265_Are_Nitrogen_Fertilizers_Deleterious_to_Soil_Health

3 Grain, Greenpeace International, and IATP, 2021, New research shows 50 year binge on chemical fertilisers must end to address climate change, https://grain.org/en/article/6761-new-research-shows-50-year-binge-on-chemical-fertilisers-must-end-to-address-the-climate-crisis

4 Farge, E., Reuters, U.N. pushes for global fertilizer price cut to avoid ‘future crisis’, https://www.reuters.com/markets/commodities/un-pushes-global-fertilizer-price-cut-avoid-future-crisis-2022-10-03/

5 ÉLYSÉE, 2022, Launch of the “Save Crops Operation” initiative., https://www.elysee.fr/en/emmanuel-macron/2022/09/23/launch-of-the-save-crops-operation-initiative

6 https://www.bloomberg.com/news/articles/2022-01-29/surging-fertilizer-prices-set-to-exacerbate-african-food-crisis

7 Bloomberg Green Markets, https://fertilizerpricing.com/

8 Southey, F., 2022, How should Europe manage the fertiliser crisis? ‘The market is overly dependent on one single country: Russia’, https://www.foodnavigator.com/Article/2022/06/22/Fertilizer-crisis-Can-Europe-reduce-its-dependence-on-Russia

9 Domm, P., 2022, A fertilizer shortage, worsened by war in Ukraine, is driving up global food prices and scarcity, https://www.cnbc.com/2022/04/06/a-fertilizer-shortage-worsened-by-war-in-ukraine-is-driving-up-global-food-prices-and-scarcity.html

10 Western Sahara Resource Watch, 2022, Mexico becoming top plunder partner, https://wsrw.org/en/news/new-report-mexico-becoming-top-plunder-partner

11 Gardner, M., Shares Magazine, 2022, Sanctions create potential earnings boost for non-Russian potash producers, https://www.sharesmagazine.co.uk/article/sanctions-create-potential-earnings-boost-for-non-russian-potash-producers

12 Inkota Netzwerk, 2022, Golden bullet or bad bet? New dependencies on synthetic fertilisers and their impact on the African continent, https://webshop.inkota.de/node/1691; ETC Group, 2022, Food Barons 2022: Crisis Profiteering, Digitalization and Shifting Power, https://www.etcgroup.org/sites/www.etcgroup.org/files/files/food-barons-2022-full_sectors-final_16_sept.pdf

13 Earl, N., City A. M., 2022, CF Fertilisers’ ‘monopoly producer status questioned by UK farming body, https://www.cityam.com/cf-fertilisers-monopoly-producer-status-questioned-by-uk-farming-body/

14 Fang, L., The Intercept, 2022, Lobbying Blitz Pushed Fertilizer Prices Higher, Fuelling Food Inflation, https://theintercept.com/2022/08/03/fertilizer-prices-food-inflation-mosaic/

15 Inkota Netzwerk, 2022, Golden bullet or bad bet? New dependencies on synthetic fertilisers and their impact on the African continent, https://webshop.inkota.de/node/1691

16 CF Industries, CF Fertilisers Announces Intention to Temporarily Halt Ammonia Production at Billingham Complex; Company Will Import Ammonia to Produce AN Fertiliser and Nitric Acid at Site, https://www.cfindustries.com/newsroom/2022/billingham-import-ammonia

17 Maritz, J, How we made it in Africa, 2022, High fuel and fertiliser costs contributing to food inflation in Africa, https://www.howwemadeitinafrica.com/high-fuel-and-fertiliser-costs-contributing-to-food-inflation-in-africa/147416/

18 Energy and Climate Intelligence Unit, 2022, Two more years of high gas prices could leave British farmers paying £1.1 billion extra for fertilisers, https://eciu.net/media/press-releases/2022/two-more-years-of-high-gas-prices-could-leave-british-farmers-paying-1-1-billion-extra-for-fertilisers

19 Dawson, T., National Post, 2022, High fuel costs, demand for fertilizer driving up costs for Canadian farmers, https://nationalpost.com/news/canada/high-fuel-costs-demand-for-fertilizer-driving-up-costs-for-canadian-farmers

20 The Federal, 2022, Pakistan: Farmers hold massive protests against rising power costs, fertilisers, https://thefederal.com/international/pakistan-farmers-hold-massive-protests-against-rising-power-cost-fertilisers/; All Africa, 2022, Ethiopia: Farmers in East Gojam, Amhara State File Complaint On Supply Shortage, Rising Cost of Fertilizer, https://allafrica.com/stories/202203240116.html; Collyns, D., Guardian, 2022, Ecuador at standstill after two weeks of protests over cost of living crisis, https://www.theguardian.com/world/2022/jun/25/ecuador-at-standstill-after-two-weeks-of-protests-over-cost-of-living-crisis

21 GhanaWeb, 2022, Planting for Food and Jobs fertiliser supply drops by 150%, https://www.ghanaweb.com/GhanaHomePage/business/Planting-for-Food-and-Jobs-fertiliser-supply-drops-by-150-1612856

22 Mbabazi, E., The Kenyan Wall Street, 2022, Government of Kenya Unveils KSh5.7 Billion Fertilizer Subsidy, https://kenyanwallstreet.com/government-of-kenya-unveils-ksh5-7-billion-fertilizer-subsidy/#:~:text=The%20Government%20of%20Kenya%20has,reducing%20farmers’%20high%20input%20costs; Verma, N., Bhardwaj, M., et Ahmed, A., Reuters, 2022, India plans over $40 billion for food, fertiliser subsidy for 2022/3, https://www.reuters.com/world/india/exclusive-india-plans-over-40-billion-food-fertiliser-subsidy-202223-sources-2022-01-28/; Business World, 2022, Palace approves P20-billion fertilizer subsidy, https://www.bworldonline.com/economy/2022/03/07/434451/palace-approves-p20-billion-fertilizer-subsidy/#:~:text=PRESIDENT%

23 Mishra, R. D., Mint, 2022, Fertilizer budget may fall short by around ₹35,000 cr this FY, https://www.livemint.com/news/india/fertilizer-subsidy-budget-may-fall-short-by-around-35-000-cr-this-fy-report-11665138113935.html

24 U.S. Department of Agriculture, 2022, Biden-Harris Administration Invites Applications for Grants Under the Fertilizer Production Expansion Program, https://www.rd.usda.gov/newsroom/news-release/biden-harris-administration-invites-applications-grants-under-fertilizer-production-expansion

25 Guarascio, F., Reuters, 2022, EU split over fertiliser plants in poorer nations as food crisis bites, https://www.reuters.com/world/europe/eu-split-over-fertiliser-plants-poorer-nations-food-crisis-bites-2022-06-20/

26 Fertilizers Europe, 2022, Fertilizer industry needs prioritised access to gas supply as sector is key to Europe’s food security, https://www.fertilizerseurope.com/wp-content/uploads/2022/07/Fertilizers-Europe_press-release_gas-availability_20072022-2.pdf

27 Foote, N., Euractiv, 2022, European Commission announces communication on fertilisers, https://www.euractiv.com/section/agriculture-food/news/european-commission-announces-communication-on-fertilisers/

28 Brzozowski, A., Euractiv, 2022, EU plans new military aid for gas-rich Mozambique amid energy crisis, https://www.euractiv.com/section/defence-and-security/news/eu-plans-new-military-aid-for-gas-rich-mozambique-amid-energy-crisis/

29 ÉLYSÉE, 2022, Launch of the “Save Crops Operation” initiative., https://www.elysee.fr/en/emmanuel-macron/2022/09/23/launch-of-the-save-crops-operation-initiative

30 Grain, Greenpeace International, and IATP, 2021, New research shows 50 year binge on chemical fertilisers must end to address climate change, https://grain.org/en/article/6761-new-research-shows-50-year-binge-on-chemical-fertilisers-must-end-to-address-the-climate-crisis

31 National Farmers Union (Canada), 2022, Nitrogen Fertilizer: Critical Nutrient, Key Farm Input, and Major Environmental Problem, https://www.nfu.ca/wp-content/uploads/2022/08/nitrogen-fertilizer-report-nfu-2022-en.pdf ; Center for International Environmental Law, 2022, Fossils, Fertilizers, and False Solutions: How Laundering Fossil Fuels in Agrochemicals Puts the Climate and Planet at Risk, https://www.ciel.org/wp-content/uploads/2022/10/Fossils-Fertilizers-and-False-Solutions.pdf

32 Harvey, F., Guardian, 2022, Windfall tax on Covid profits could ease ‘catastrophic’ food crisis, says Oxfam, https://www.theguardian.com/world/2022/jun/27/windfall-tax-on-covid-profits-could-ease-catastrophic-food-crisis-says-oxfam; National Farmers Union (Canada), 2022, NFU Renews Call to Investigate Fertilizer Pricing, https://www.nfu.ca/media-release-nfu-renews-call-to-investigate-fertilizer-pricing/; Grain, 2022, A fertiliser cartel holds the global food system hostage, https://grain.org/en/article/6882-a-fertiliser-cartel-holds-the-global-food-system-hostage

33 SpaceNUs, 2021, Can Germany cut the nitrogen fertilization rate by 20%, https://www.spacenus.com/en/news/can-germany-cut-the-nitrogen-fertilization-rate-by-20

34 Ritchie, H., Roser, M., Rosado, P., Our World in Data, 2013, Fertilizers, https://ourworldindata.org/fertilizers

35 International Panel of Experts on Sustainable Food Systems, 2018, Seven case studies of agroecological transition, http://www.ipes-food.org/pages/Seven-Case-Studies-of-Agroecological-Transition

36 Institute for Agriculture and Trade Policy, Agroecological Transitions, https://www.iatp.org/agroecological-transitions

37 International Panel of Experts on Sustainable Food Systems, 2020, Money Flows: What is Holding Back Investment in Agroecological Research for Africa?, https://www.ipes-food.org/img/upload/files/Money%20Flows_Full%20report.pdf

38 Grain, 2021, Lessons from Sri Lanka’s agrochemical ban fiasco, https://grain.org/en/article/6774-lessons-from-sri-lanka-s-agrochemical-ban-fiasco

39 Organic Without Boundaries, 2022, Why We Cannot Blame the Sri Lankan Crisis on Organic Farming, https://www.organicwithoutboundaries.bio/2022/06/02/why-we-cannot-blame-the-sri-lankan-crisis-on-organic-farming/

40 Grain, 2021, Lessons from Sri Lanka’s agrochemical ban fiasco, https://grain.org/en/article/6774-lessons-from-sri-lanka-s-agrochemical-ban-fiasco

41 Peasant Journal, 2022, Jan Douwe van der Ploeg on Right wing farmers’ protests in the Netherlands, https://peasantjournal.org/news/jan-douwe-van-der-ploeg-on-right-wing-farmers’-protests-in-the-netherlands/

42 Frison, E., International Panel of Experts on Sustainable Food Systems, 2016, From Uniformity to Diversity: A paradigm shift from industrial agriculture to diversified agroecological systems, https://www.ipes-food.org/_img/upload/files/UniformityToDiversity_FULL.pdf

43 Oakland Institute, 2015, The Untold Success Story: Agroecology in Africa Addresses Climate Change, Hunger, and Poverty, https://www.oaklandinstitute.org/untold-success-story-agroecology

44 Rothamstead Research, 2022, Fertiliser Use Could be Reduced with Nature-Based Farming, Shows Major Study, https://www.rothamsted.ac.uk/news/fertiliser-use-could-be-reduced-with-nature-based-farming-shows-major-study

45 Pretty, J. N., et. al., 2006, Resource-Conserving Agriculture Increases Yields in Developing Countries, 40:4 (1114-1119), Environmental Science and Technology, https://pubs.acs.org/doi/10.1021/es051670d

46 Oxfam, 2014, Scaling-Up Agroecological Approaches: What, Why and How?, https://www.fao.org/fileadmin/templates/agphome/scpi/Agroecology/Agroecology_Scaling-up_agroecology_what_why_and_how_-OxfamSol-FINAL.pdf

47 United Nations Conference on Trade and Development, 2008, Organic Agriculture and Food Security in Africa, https://unctad.org/system/files/official-document/ditcted200715_en.pdf

48 Oxfam, 2014, Scaling-Up Agroecological Approaches: What, Why and How?, https://www.fao.org/fileadmin/templates/agphome/scpi/Agroecology/Agroecology_Scaling-up_agroecology_what_why_and_how_-OxfamSol-FINAL.pdf

49 United Nations Food and Agriculture Organization, 2022, Impact of Zero Budget Natural Farming on Crop Yields in Andhra Pradesh, South East India, https://www.fao.org/agroecology/database/detail/ar/c/1470939/

50 Global Alliance for the Future of Food, The Politics of Knowledge: Will we act on the evidence for agroecology, regenerative approaches, and Indigenous foodways?, https://story.futureoffood.org/the-politics-of-knowledge/

51 Ponsio, L. C., et. al., 2015, Diversification practices reduce organic to conventional yield gap, https://royalsocietypublishing.org/doi/10.1098/rspb.2014.1396

52 International Panel of Experts on Sustainable Food Systems, 2018, Breaking Away from Industrial Food and Farming Systems: Seven case studies of agroecological transition, https://www.ipes-food.org/_img/upload/files/CS2_web.pdf

53 Varghese, S., Institute for Agriculture and Trade Policy, 2017, A Case Study on the Agroecological Transition in Mexico, https://www.iatp.org/documents/case-study-agroecological-transition-mexico

54 International Panel of Experts on Sustainable Food Systems, 2018, Breaking Away from Industrial Food and Farming Systems: Seven case studies of agroecological transition, https://www.ipes-food.org/_img/upload/files/CS2_web.pdf

DOWNLOADS

Download a PDF of the full paper and Annex 1.

Descargue el documento en español.

Télécharger le document en français.