On May 13, the Commodity Futures Trading Commission (CFTC or Commission) issued a warning to the trading platforms, clearing organizations (the back office processing of trades) and futures contract merchants: the organizations “are expected to prepare for the possibility that certain contracts may continue to experience extreme market volatility, low liquidity and possibly negative pricing.” The trigger for the warning was the price collapse of the Chicago Mercantile Exchange (CME) West Texas Intermediate (WTI) crude oil contract to minus $37 per barrel, the first time a U.S. oil futures contract had traded below zero. But the CFTC said that the warning applied to all physical commodity contracts, including the 16 agriculture contracts covered by a CFTC proposed rule on speculative position limits. IATP submitted a May 15 comment on the proposed rule.

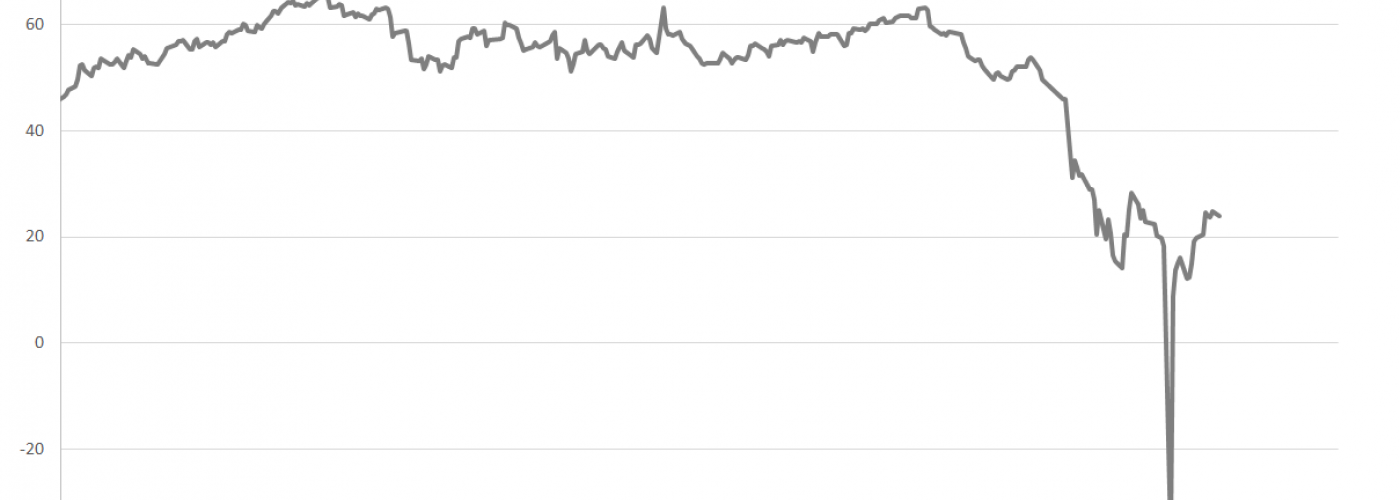

The initial explanation of the WTI price collapse on April 20 was a combination of a production glut, near full oil storage capacity and sharply falling demand for crude oil derived products, above all gasoline, due to COVID-19. No doubt supply and demand figures played a role in the price collapse. But by April 21, the WTI price for June delivery had risen to $13.78 per barrel. Supply demand factors did not change overnight, so what had happened?

The United States Oil Fund (USO), which held 25% of all WTI May contract positions as the contract expired on April 21, “rolled” its positions so close to the expiration that it could not find buyers for its May positions except at negative prices. USO found enough buyers for its June positions far enough before the contract expiration to jack the price up more than $50 per barrel from one day to the next.

Among the questions the CFTC should be asking in its investigation of the WTI price collapse and rebound are 1) how did the CME’s voluntary “position accountability” computer enabled monitoring regime fail to warn USO to divest gradually a large part of its WTI positions to prevent excessive speculation and extreme price volatility in the contract?; and 2) will the CFTC’s proposed position limit rule, which would allow financial speculators to hold up to 25% or less of positions in 25 physical commodity contracts, with numerous limit exemptions, be revised to prevent excessive speculation? Indeed, these questions could also be asked about the CFTC investigation into the livestock (live cattle, feeder cattle, lean hogs) futures contracts, announced by CFTC Chairman Heath Tarbert on April 22.

Position limits were mandated in the Dodd Frank Wall Street Reform and Consumer Financial Protection Act of 2010 (Dodd Frank), following the speculation fueled commodity market price boom and bust of 2005-2009. Both Wall Street and LaSalle Street (home to the CME) lobbying, litigation and regulatory comments have delayed the finalization of a position limit rule for a decade. The CFTC recently opened the fifth version of that rule for comment, not counting supplements to past proposals and position aggregation rule proposals. IATP was critical of most features of the 2020 proposed rule.

First, we urged the Commission not to finalize the rule before completing its investigations into the WTI and livestock futures trading extreme price movements. Then we urged CFTC not to finalize the rule before they had finalized a rule on automated trading, first proposed in 2015. In the nine years since position limits were first proposed, the automated trading of physical commodity contracts — one computer algorithm responding to the price bid or offer of another algorithm — has greatly increased. It is very unlikely that the WTI contract price could fall 300% in a day without automated trading. At the 2018 and 2019 CFTC Ag Futures conferences, ‘point and click’ commodity traders said that automated traders had pre-empted their ability to buy contracts to manage price risks. Concurrent review of the two rules would help the Commission determine whether the proposed position limits could prevent or diminish excessive speculation, as required by Dodd Frank, in an automated trading environment.

Regarding the rule itself, IATP analyzed the proposed position limit levels, which are based on Deliverable Supply Estimates (DSEs) provided by the exchanges on which the contracts are traded. The CFTC proposed to increase the share of a contract that ‘non-commercial’ market participants, i.e. financial speculators, could control up to 25%, the share controlled by USO in the WTI May crude oil contract price collapse. The “up to 25%” provision provides the exchanges and the market participants with legal protection against violating limit levels, even if the exchanges have to throw “circuit breakers” to halt temporarily algorithm triggered extreme price movements.

We compared DSEs for corn and wheat contracts and found inconsistencies or lack of explanation of the level limits in those and other contracts. Furthermore, we advised the CFTC to review the limit levels annually but allow for interim reviews more frequently because of how climate change would disrupt agricultural production used to calculate the DSEs, according to the Fourth National Climate Assessment.

More worrisome than the insufficient rationales for the calculation of the limits themselves was the CFTC’s deference to the exchanges about when and why to allow for exemptions to the limits. We noted that at a May 7 meeting of the CFTC’s Energy and Environmental Markets Advisory Committee (EEMAC), a CME official said that it had granted 500 exemptions in 2019. How many exemptions were granted to market participants by the other exchanges? How would those exemptions, plus the exemptions to position aggregation granted under the terms of a rule finalized in 2016, enable the position limit rule to prevent excessive speculation and market disruption?

The CFTC must cooperate with the exchanges to implement and enforce its rules, while not delegating so much of its authority to the exchanges as to render the agency ineffective. We cited our March 9 letter to the Commission about a proposed rule on the cross-border trading of U.S. contracts by the foreign subsidiaries of U.S. parent firms. In that letter, IATP stated that the CFTC had imprudently subordinated its authority over cross-border trading to that of foreign regulators, the Federal Reserve Bank and the Securities and Exchange Commission. In the current proposed position limit rule, the CFTC would cede its authority to the exchanges and market participants to the point where it all but apologized to them for the “undue costs” of not just compliance with the rule, but even paying the price for non-compliance.

However, the Commission is not deferring to the exchanges about its authority to respond to market and financial risks related to external events, such as COVID-19 and climate change. On June 12, 2019 the CFTC’s Market Risk Advisory Committee (MRAC) agreed to appoint a subcommittee to report to MRAC on climate related financial risk in Commission regulated contracts, activities and entities. MRAC would review the report in late June and make actionable recommendations for the CFTC. In response to a CFTC request for information, IATP responded on June 19 to recommend a “360 degree review” of Commission rules and possible modifications to rules to make them climate finance resilient.

On May 14, IATP responded to a Commission request for five categories of information in four pages or less. We responded to four categories and added a fifth of our own, “Urgency and ambition.” To counter the disinformation campaigns about climate change and the costs and benefits of reducing carbon dioxide emissions and adapting to climate change, we recommended that the CFTC set up a Climate Change Financial Regulatory Lab to investigate the impacts of climate change on CFTC regulated contracts, market participants and exchanges. The indispensable Climate Risk Review summarized some of the forty responses to the Commission request, characterizing the IATP recommendation as “out there” or outside of the mainstream.

The subcommittee, which is scheduled to deliver its report to MRAC on June 17, may prefer to incorporate mainstream ideas from market participants. But IATP suggested that the subcommittee ask the CFTC to develop a cost benefit model for its rulemakings that would incorporate the “worst case economics” analysis of Frank Ackerman, rather than apply traditional cost to industry analysis of each rule.

We advised the subcommittee to recommend that the CFTC not accept uncritically the view that trading derivatives contracts based on carbon dioxide emissions offset projects would be the best and most economically efficient way to reduce emissions. We wrote, “Environmental market failures add to the global failure to halt the momentum towards an unstable climate that will impose huge costs on market participants.” Furthermore, if emissions offset derivatives contracts were used as collateral, — e.g., in Collateralized Loan Obligations (CLOs), a Wall Street innovation that turns debt into tradeable assets — those contracts could help trigger financial instability if CLO defaults cascade throughout the markets.

For our “urgency and ambition” topic we quoted Frédéric Hache of the Green Finance Observatory, who commented about market participant pledges to reach “net zero” emissions by 2050 made at the latest Conference of the Parties of the U.N. Framework Convention on Climate Change: “Everybody talks about ambition but nobody questions the how. The how is at least as important, because that’s where all the greenwashing takes place.” We concluded with a recommendation to the MRAC subcommittee that it advise the CFTC to question the how of derivatives products and trading to reach “net zero” and not become an enabler of greenwashing.