Lea "Distorsionar los mercados en nombre del libre comercio" aquí.

For the last three months, business pages and farm media in the United States have been sounding the alarms about the Mexican government’s announced phaseout of imports of genetically modified (GM) corn. Mexican President Andrés Manuel López Obrador first reported the move in a December 2020 presidential decree, which immediately banned the cultivation of GM corn in Mexico and mandated the phaseout of GM corn imports and the importation and use of the herbicide glyphosate by January 31, 2024.

Mainstream U.S. farm organizations reacted immediately, calling on U.S. government officials to invoke the new biotechnology provisions in the newly revised U.S.-Mexico-Canada Agreement (USMCA), which replaced the North American Free Trade Agreement in July 2020. But the most recent alarm bells were prompted by an economic modeling study from consulting firm World Perspectives, Inc. (WPI) that claims to show catastrophic impacts of Mexico’s looming GM corn ban on U.S. and Canadian farmers and on Mexico’s own food security.

The media dutifully reported the story, with alarmist headlines and dire warnings to U.S. officials to stop Mexico from enacting the ban. “Mexico Threatens a Trade War with the U.S. and Canada,” read a Wall Street Journal headline. The Hill warned “Mexico moves closer to a devastating policy for US agricultural exports.” Farm-state legislators cited the study and demanded the U.S. government sue Mexico for trade violations.

Largely unreported was the fact that the original modeling was commissioned by CropLife International, the agrochemical industry trade association. And the March 2022 study was updated to reflect market turbulence caused by the Russia-Ukraine war on behalf of a self-described “coalition of leading food and agriculture industry stakeholders in both Mexico and the United States.” Those “stakeholders” include CropLife and comprise a Who’s Who of agribusiness interests in the U.S. and Mexico, all of whom have a strong economic interest in opposing Mexico’s proposed restrictions on GM corn.1

The purpose of this study is to analyze the methodology and assumptions in the industry-sponsored modeling to determine whether researchers have inflated the estimates of the negative impacts of the proposed GM corn ban. Indeed, we find that the researchers overestimate the costs of the ban in both the U.S. and Mexico by:

- treating the January 2024 GM corn ban as sudden, even though it had been announced three years earlier;

- treating the ban’s deadline and scope as inflexible, even though the Mexican government has announced it will phase in the ban on feed corn;

- underestimating U.S. producers’ ability and willingness to respond to increasing demand for non-GM corn;

- ignoring the Mexican government’s funded effort to decrease import dependence by increasing its own corn production;

- overestimating the yield advantages of GM over non-GM corn;

- imputing high costs associated with segregating non-GM from GM corn in international supply chains.

Taken together, these flaws call into question the high cost estimates in the industry-sponsored modeling. Many U.S. corn producers have indicated a willingness and ability to increase production of non-GM corn. Given Mexico’s clear signal that it wants to buy non-GM corn and its willingness to procure it from U.S. farmers, the specter of a trade dispute is uncalled for. There is no discriminatory action against U.S. producers, just against GM corn from any country. A close textual reading of the USMCA’s biotechnology provisions by IATP’s former senior attorney documents that Mexico has the right to enact such a restriction based on legitimate science-based concerns about human health and the environment. U.S. farmers would be better served by taking the advance notice of Mexico’s interest in procuring non-GM corn and preparing to supply this important market for U.S. farm goods. In the process, they would also be giving U.S. consumers something market surveys indicate they desire: greater choice in the marketplace to purchase non-GM food products.

Background

The Mexican government’s stated reason for the presidential decree phasing out GM corn and glyphosate was to protect both the environment and public health. The environmental concerns relate to biodiversity loss and potential contamination of native corn varieties by pollen from GM corn. The health issues relate to glyphosate being a “probable human carcinogen,” according to the World Health Organization’s cancer institute, and to outstanding questions about the safety of GM corn, particularly since most is engineered to tolerate glyphosate applications. Traces of both transgenes from GM corn and glyphosate have been found in tortillas and other common corn-based staple foods in Mexico. In issuing the presidential decree, President López Obrador cited the country’s recognition of the precautionary principle, which asserts a higher standard of proof for product safety than is commonly used in the U.S.

The prohibition on the cultivation of GM corn was immediate, formalizing a suspension of permits for GM corn trials that had been ordered by Mexican courts in 2013 and affirmed by its Supreme Court last year. The decree also mandated that corn used in relatively unprocessed forms for direct human consumption, such as tortillas, not contain GM varieties. The phaseout of glyphosate and GM corn imports was issued with a three-year deadline for full enforcement in January 2024. The glyphosate phaseout is ongoing, with Mexico reporting a 50% decrease in the importation and use of the herbicide. The phaseout period is being employed by Mexico to develop safer alternatives to glyphosate, a process that is indeed generating less toxic forms of weed-control.

The announced phaseout of GM corn imports has thus far produced resistance rather than market development in the U.S. In part, that was due to a lack of clarity on the part of the Mexican government regarding the scope of the ban. One section of the government has stated that the ban would be all-encompassing, while another, led by Mexico’s Secretary of Agriculture, has sought to reassure U.S. officials that the ban applies only to corn for direct human consumption in low-processed foods such as corn dough (“masa”) and tortillas — generally white corn. But the ban would not extend to yellow dent corn, which is used primarily as animal feed and as a raw material for industrial products. Some 95% or more of U.S. corn exported to Mexico is yellow corn, nearly all of it GM corn. White corn exports have risen in the last two decades. There are conflicting reports about how much white corn the U.S. exports to Mexico and how much of that comes from GM varieties.

While such uncertainty over the scope of the restrictions may have delayed U.S. farmers’ efforts to increase non-GM corn production, President López Obrador recently clarified his government’s position. Mexico would stop allowing imports of GM corn for direct human consumption in January 2024, as announced. That action that would affect the relatively small number of U.S. farmers growing GM white corn, though they would still be permitted to export their corn for use in processed foods, animal feed and industrial uses. On GM yellow corn, he clarified that he would extend the deadline for the import phaseout to 2025, pending a joint review and a more thorough scientific assessment of the risks to human health and the environment of GM corn used in livestock and other sectors.

Though some uncertainty remains about the future of GM yellow corn exports to Mexico, the market signals from the government declaration are now quite clear. Mexico will not allow GM corn to be used in the production of minimally processed foods for direct human consumption, such as tortillas and tamales, from the U.S. or any other nation. Demand will increase for non-GM white corn, and at least for now, U.S. exports of GM white corn will be permitted but not allowed to be used in the “corn-tortilla chain.” And Mexico clearly prefers to buy non-GM yellow corn, with any outright ban postponed beyond the original January 2024 deadline but with reviews planned to consider further restrictions. In the meantime, Mexico will continue its efforts to increase production of non-GM white and yellow corn, which Mexican government officials state they hope will reduce the need for imported corn by half by 2024.

Damage estimates on growth hormones

As its sponsors hoped, the WPI modeling produced alarming economic damage estimates for the U.S.:

This study finds that the sudden shift to non-GM corn imports by Mexico would cause non-GM corn prices to increase sharply, peaking at 42 percent above baseline values. Conversely, GM corn prices would fall 10 percent over three years following the ban and these price changes would fundamentally alter crop acreage and the U.S. grain handling system. As the shock ripples through the U.S. economy, this study finds that GDP would contract by $30.55 billion, and $73.89 billion in economic output would be lost.

They were even more dramatic for Mexico, according to WPI researchers:

Over the 10-year forecast period, higher non-GM corn prices mean Mexico would pay $9.73 billion more to import corn than it would otherwise, an increase of 19 percent over baseline forecasts. Additionally, tortilla prices would increase sharply, peaking at 30 percent above baseline forecasts and averaging 16 percent higher over 10 years. Additionally, the Mexican livestock sector would see feed costs increase by 13.7 percent, on average, which would cause the industry to contract by 1.2 percent annually. The total impacts of added costs for consumers, costs to import grain, and the contraction in the livestock sector mean that a policy banning GM corn would cost Mexico’s economy 56,958 jobs annually, create a contraction in GDP of $11.72 billion and reduce economic output by $19.39 billion over 10 years.

While Mexico’s actions are intended to reduce potential harm to human health and the environment, the Crop Life-sponsored study is designed to magnify the social and economic harm from Mexico’s proposed GM corn ban. To achieve this, WPI modelers used a set of unrealistic assumptions about Mexico’s policies and the real farm economy. In their modeling, these operated like growth hormones genetically engineered to inflate estimates of economic damage. More realistic assumptions would dramatically reduce the estimates of economic disruption, price increases, lost output and rising food insecurity in Mexico. Here, we examine only the most questionable inflationary assumptions.

False Assumption #1: The ban will cover all GM corn imports. As noted, the Mexican government’s recent clarifications about the implementation of the phaseout of GM corn make clear that they do not now cover all GM corn imports. The government confirms that the phaseout is certain for GM white corn for direct human consumption, a small segment of U.S. production estimated at less than 5% of U.S. exports to Mexico. If even half of U.S. white corn production is GM corn, the impacts will be commensurately small, and those U.S. exports would still be permitted for uses outside the corn-tortilla chain. The clarification on yellow corn imports leaves open the possibility that Mexico will indeed ban GM yellow corn imports, but it undercuts one of the central assumptions in the industry model they will be prohibited in January 2024. That is relevant to the second flawed assumption.

False Assumption #2: Mexico’s ban on GM corn imports will take effect, without warning, in January 2024 and farmers and traders will have to scramble to adjust. WPI modelers remarkably treat the ban, long foretold, as a completely unanticipated economic shock. There are two key flaws in this assumption. First, farmers are getting plenty of warning. The decree was announced three years before the January 2024 deadline, and now that deadline is being extended for some varieties of corn. It does indeed take time for agricultural markets to adjust to changes in demand. More non-GM seeds need to be produced, for example, and traders need to establish segregated supply chains to ensure purity of non-GM content. But with clear market signals, markets adjust. That’s what markets do.

Second, we now know the January 2024 ban will not include GM yellow corn, even if it may thereafter. To the extent the ban will not initially affect the vast majority of U.S. corn exports, there is even more time to make that adjustment. There is every reason to believe the Mexican government would not enact a total ban even in 2025 but would phase in restrictions over time. Why? Because the economic shock might be too large, and markets need time to adjust.

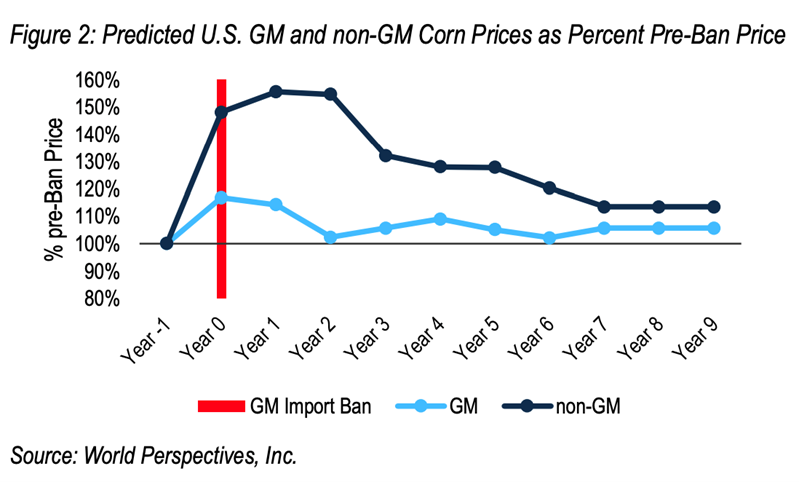

This assumption is a key growth hormone in WPI’s economic model, which estimates costs over a 10-year period following the ban. Consider one of the key graphs in the model, which shows 50-60% price increases for non-GM corn in the first three years of the ban (Years 0, 1, 2).

The only reason non-GM corn prices rise so much in this economic model is that there has been no market adjustment and the ban is complete in January 2024. That is, no U.S. farmers have increased their production of non-GM corn to fulfill this new and growing market, so demand massively outruns supplies of non-GM corn and prices spike. Meanwhile demand drops suddenly for GM corn, reducing prices and returns. Economic costs are high. Note that in WPI’s own modeling, markets do eventually adjust, with non-GM corn supply and demand coming into balance and prices converging with those for GM corn. It is only the assumption of economic shock that has the model delivering shockingly large estimates of high prices and costs — some $13.4 billion in lost output — in those first three years after this supposed surprise policy change. The costs to U.S. farmers after that are negligible, as increased demand for non-GM corn increases production at reasonable prices.

It is worth noting that WPI modeled two alternative scenarios, one in which GM corn is permitted for animal feed but not industrial uses, and another in which both uses are exempted. The estimated price and economic impacts are a fraction of the WPI estimates of a full ban, though industry press releases have chosen not to emphasize those lower numbers. The first reduces costs dramatically. WPI modelers conclude: “Due to the smaller size of the shock and the ability to secure small volumes of non-GM corn from other suppliers (likely Argentina and Brazil), the market adjusts relatively quickly and the large shifts in farm trends and the grain handling industry are not predicted. This study finds negligible changes in GM corn and other crop plantings and prices.”

The second scenario, which leaves white corn for direct human consumption as the primary product covered by the January 2024 ban, appears to be closer to present-day reality. The impacts are even smaller. Still, the modelers leave the ban as a sudden shock rather than an anticipated shift in the market. They do not offer an estimate of what share of U.S. white corn production is GM corn. The USDA has called it “little, if any,” while industry sources say it could be as high as 50%. Either way, WPI is overestimating the price increases and economic costs of a ban limited to GM corn for direct human consumption. U.S. farmers can easily produce enough non-GM corn to supply Mexico’s market, particularly if they take current market signals seriously and begin now to increase production of non-GM seeds.

False Assumption #3: U.S. farmers are unable or unwilling to easily shift to growing non-GM corn. On its face, this is a bizarre and convenient assumption. After all, until the widespread adoption of GM crops in the mid-1990s, the U.S. was the world leader in non-GM corn production and exports. GM seeds and their related technologies have eclipsed that history, but they have in no way obliterated it. The land and equipment are largely the same, the only change is in the seeds, related agrochemicals and grain handling. It is bizarre to suggest that farmers can’t or won’t switch if the market wants non-GM corn.

But it is convenient for those who want to challenge Mexico’s policy. In fact, the National Corn Growers Association, one of the mainstream corn farmer organizations, is a sponsor of the WPI study and its President Tom Haag authored an opinion article for The Hill that echoed the alarms but failed to disclose that his organization sponsored the study. Andy Jobman, president of Nebraska Corn Growers Association, told Reuters that non-GM seeds were an archaic technology and switching would be “like going from using electricity to going back to using candles in terms of technology."

As the Organic & Non-GMO Report has documented in several articles about the issue, with a price premium and a guaranteed market, farmers can and will switch back to non-GM corn. Ken Dallmier, CEO of Clarkson Grain, an Illinois-based supplier of organic and non-GMO grains, said that the U.S. could supply Mexico with all the non-GMO corn it needs. “Given time and focus, I think it’s completely feasible,” he said.

Graham Christensen, a fifth-generation farmer in Lyons, Nebraska, said he would be eager to supply Mexico. “There are a lot of farmers up here who could easily transition to non-GMO corn, and there are a lot of us that are looking for a solid marketplace.”

Mac Ehrhardt, owner of Albert Lea Seeds, a leading supplier of organic and non-GMO seeds, told Non-GMO Report, “I totally believe if Mexico made the decision, the U.S. supply chain would rise to meet the demand.”

There will be a period of adjustment, but there is no reason to believe we will see the kinds of market disruption predicted by WPI researchers. Because there is already domestic demand for non-GM corn for consumer goods from producers such as Frito Lay, which they can label “non-GMO,” there are existing supply chains in the U.S. already meeting that demand. Farmers generally receive a small price premium for delivering non-GM corn. The Organic & Non-GMO Report notes that in 2020, U.S. farmers planted 7.5 million acres of non-GM corn and many more could and would do the same.

Obviously, that is exactly what CropLife, the sponsor of the original WPI study, does not want to happen. A shift from GM to non-GM corn should cost farmers very little, but it will cost the agrochemical industry customers for its products. As Ehrhardt observed, “Reports like that are written by people who have an economic interest in stopping Mexico from banning GMO corn.”

False Assumption #4: Non-GM corn is less productive and profitable for a farmer to grow, leading to higher consumer prices and reduced farmer profits. The WPI model assumes that GM corn offers 7-10% higher yields than non-GM corn. They offer no justification for this claim, and they impute that the productivity advantage will extend for the full 10 years of their projection. That is the main reason one sees, in their price graph reproduced earlier, higher prices for non-GM corn even after markets have adjusted. There is little basis for this claim, despite hand-wringing about archaic technologies.

Seed companies that produce and sell GM and non-GM corn seeds attest to their comparable productivity levels. According to Roseboro, companies selling non-GM corn seed, such as Spectrum Non-GMO, Prairie Hybrids and Albert Lea Seed, have found that their non-GMO corn seed hybrids yield as much or even more than GM hybrids. Farmers who grow non-GM corn report that they do not see lower yields as long as they control pests and weeds eliminated by most GM varieties and their accompanying chemicals. That requires alternative pesticides and herbicides, but it does not result in lower yields. In fact, many non-GM farmers use a variety of regenerative farming practices such as no till, cover crops and other practices. Many report a decreasing need for agricultural chemicals over time as the soil improves. That also lowers their production costs, as does the much lower cost of non-GM seeds compared to GM varieties. That means that farmers not only see comparable yields, but also they may see reduced costs and rising profitability.

False Assumption #5: The cost of establishing and maintaining supply chains that segregate non-GM corn for delivery to Mexico will be exorbitant. This may be the most exaggerated assumption in the WPI study. The estimated 10-year cost of $11.8 billion for segregation accounts for nearly as much of the final cost as the inflated estimates of production losses, $13.6 billion. It comes from an assumed 29.5 cents-per-bushel cost associated with ensuring the integrity and purity of non-GM corn supplies in the first four years after the GM corn ban. It is justified only by citing one study estimating costs at 1-27 cents/bushel and another estimating 1-50 cents/bushel. From that wide range, WPI modelers select 29.5 cents/bushel. By the end of the 10-year study period, the cost reduces to near zero. With these large upfront costs assumed to be passed on to consumers, they dramatically inflate the price spikes WPI claims in the first years of the graph presented earlier.

There will certainly be up-front costs associated with increasing segregated supply chains for non-GM corn, but such infrastructure already exists. For example, Bunge has a large corn processing facility in Nebraska that is certified by the Non-GMO Project, the organization that verifies Non-GMO products. There is no reason to believe the inflated WPI cost estimates, which account for roughly one-third of WPI’s estimates of direct losses from a full GM corn ban. There is every reason to doubt them.

False Assumption #6: Mexico does not increase domestic corn production to reduce its demand for imports. The WPI study makes little mention of the Mexican government’s programs to increase domestic corn production, and their model assumes that Mexico will continue to need some 17 million metric tons of imported corn, as it does now. That is a convenient assumption, because that fixed and high level of demand makes the assumed shock to the market caused by the GM corn ban all the more shocking.

This ignores well-funded Mexican government efforts to decrease import dependence in key food crops — corn, wheat, rice, beans and dairy products — and increase its food self-sufficiency by increasing domestic production. President Lopéz Obrador even created the new position of undersecretary of agriculture for food self-sufficiency. He has put in place a variety of programs to stimulate production of key staple crops. He is quoted stating that the government’s goal is to cut corn import dependence by half by the end of 2024, implying added production of some 7-8 million metric tons of corn.

Many are skeptical that Mexico can meet such ambitious goals, but time will tell. There is more reason to be skeptical of the assumption in the WPI model that the effort will achieve no increase at all in domestic corn production. Again, that is convenient for a modeling exercise designed by its sponsors to show high and prohibitive costs from banning GM corn.

False Assumption #7: Mexico can find only limited supplies of non-GM corn from other countries. Mexico is currently one of the largest corn importers in the world. If its demand shifts to non-GM corn, foreign growers will take notice. The WPI study notes that Argentina and Brazil, two other large corn exporters, have 8% of their production in non-GM corn. Since the enactment of the North American Free Trade Agreement in 1994, Mexico’s import-dependence on the U.S. for basic grains like corn has skyrocketed. The effort to source non-GM corn from other countries is part of a broader Mexican government campaign to diversify its import sources to reduce the dominance of U.S. exporters. Again, time will tell how much non-GM corn can be sourced from other countries, but one can expect corn exporters to be eager to get a share of a large new market for non-GM corn.

False Assumption #8: Mexico will suffer punishingly high food inflation and food insecurity as a result of the GM corn ban. All the above assumptions produce unrealistically high estimates of impacts in Mexico. Those include a 26% and 30% increase in the cost of corn in the first two years after the ban. Over the full 10 years, WPI estimates a 19% increase in corn costs, a 16% increase in the price of tortillas, a 35% jump in feed costs and an astonishing 67% increase in the cost of chicken, which is imputed to result in a 78% drop in consumption. All of these cataclysmic outcomes flow from the unfounded assumptions about the policy shock, the failure of markets to adjust, and three or four years of assumed market chaos. Based on what we now know about the initial limitation of the ban to GM white corn, it is difficult to justify any estimate of significant impacts on Mexican corn, tortilla, feed or poultry prices or on food security.

Furthermore, lost in the WPI study and the unbalanced reporting on it are the high costs to Mexico of its rising levels of food import dependency. At a time like this, when the pandemic and geopolitical conflict have driven up crop prices, Mexico pays dearly for its imports of corn and other foods. When international prices are low, as they were in the seven years preceding the pandemic, cheap imports flow into Mexico, undercutting local producers, reducing the value of their harvests as prices are suppressed. This undermines efforts by the government to restore some measure of food self-sufficiency to insulate both farmers and consumers from their exposure to global markets dominated by large exporting nations and by large multinational agribusiness firms. Import dependency also carries high costs.

Disrupting, not securing, markets

Taken together, these flawed assumptions in WPI’s industry-sponsored assessment of Mexico’s GM corn restrictions act as growth hormones injected into a complex economic model to generate inflated estimates of high costs and lost output in the U.S. and severe food insecurity in Mexico. It would require new economic modeling using more realistic assumptions to generate better estimates, but we can be assured that the huge up-front costs in the first three years, as shown on the WPI graph earlier, would be dramatically lower as markets adjust to what now appears to be a partial ban in 2024 with additional restrictions possible after 2025. And there is little reason to believe that the long-term costs, after markets have adjusted, wouldn’t be close to zero.

That presumes that markets begin to adjust now based on the clear market preferences being articulated by the Mexican government. As Kellee James, chief executive of Mercaris, a commodities data provider, told Reuters, "It's about getting organized and sending clear signals ahead of time." And that is precisely with CropLife and the other agribusiness sponsors of the WPI analysis want to prevent from happening. With their study, they introduce uncertainty into those markets, disrupting what could easily be the relatively smooth and inexpensive emergence of a thriving non-GM corn sector in the U.S.

The U.S. government only adds to the market uncertainty with its threats to sue Mexico under the USMCA trade agreement. The U.S. agrochemical industry very much wanted the new NAFTA, in its added biotechnology chapter, to prevent Mexico from restricting GM imports. That is not what the text says, according to a detailed analysis by Sharon Treat, a respected attorney from the Institute for Agriculture and Trade Policy. “The final text of the agreement does not restrict domestic policy choices in the manner agribusiness and its allies might wish,” she concludes. It mandates only transparency in decision-making about agricultural biotechnology trade. In fact, the text of the Agricultural Biotechnology section is explicit: "This Section does not require a Party to mandate an authorization for a product of agricultural biotechnology to be on the market.” [Art. 3.14.2]

Given the repeated assertions that Mexico’s GM corn ban violates the USMCA, it is worth repeating the conclusions from her textual analysis:

While the USMCA’s agricultural biotechnology provisions provide procedural guidance to government regulators, they lack substantive requirements that would provide a basis for overturning Mexico’s policies and permit decisions. While industry lobbyists succeeded in convincing trade negotiators to include agricultural biotechnology provisions in the USMCA, they now misstate the scope and significance of the text that was agreed to by Canada, Mexico and the U.S. The parties to the USMCA retain considerable authority to enact and implement non-discriminatory agricultural, environmental and cultural policies that may affect the marketing and cultivation of agricultural biotechnology, and Mexico’s actions align with that authority.

Mexico is in no way discriminating against U.S. corn, it is restricting GM corn from any exporting country. Its action is grounded in a large body of scientific research that documents risks both to public health and to the environment, not just from cultivating GM corn in Mexico but from importing it. In fact, NAFTA’s environmental commission, in an extensive 2003 study of contamination of native corn crops in Mexico by transgenic pollen, concluded that the likely source was corn imported as food or feed and inadvertently planted by a farmer. Mexico retains the sovereign right to enact domestic laws and regulations that protect public health and the environment, and the current government is very committed to increasing those protections. The USMCA does not prevent Mexico from ensuring that international trade complies with such laws.

U.S. threats of trade disputes under USMCA have the same effect as the industry’s inflated estimates of damage from Mexico’s GM-corn ban. They add to market uncertainties that prevent farmers and other market actors from increasing the supply of non-GM corn that is clearly desired by an important trading partner. The cataclysmic economic disruptions predicted by WPI can be easily avoided if Mexico’s sovereign rights to determine its own standards for public health and the environment are respected and markets get the clear signals they need to adjust to the new demand for non-GM corn. The Mexican government has shown a willingness to negotiate the timeline for the needed transition.

Farmers and consumers on both sides of the border would be better served if the U.S. government engaged in respectful negotiations with Mexico. Instead of distorting North American corn markets by trying to prevent Mexican demand for non-GM corn from expressing itself, the U.S. can help ensure that Mexico’s preferences, as a major consumer of U.S. corn, do not disrupt corn markets in North America.

Timothy A. Wise is a senior advisor at the Institute for Agriculture and Trade Policy and a Senior Research Fellow at Tufts University’s Global Development and Environment Institute. His 2019 book, Eating Tomorrow (New Press), contains a full chapter on the controversies over GM corn in Mexico. This policy brief includes additional reporting by Ken Roseboro, editor of The Organic & Non-GMO Report.

Endnotes

1. Sponsors of the study include Mexico’s National Agriculture Council, the U.S. Grains Council, the National Association of State Departments of Agriculture, the National Corn Growers Association, Biotechnology Innovation Organization (BIO), CropLife America, the Corn Refiners Association, Mexican Association of Feeders of Bovine Cattle Ac., Local Agricultural Association of Matamoros, AC, Association of Suppliers of Agricultural Products Mexico, AC (Appamex), Mexican Association of Seeds, AC (Amsac), National Association of Manufacturers of Food for Animal Consumption, SC (Anfaca), National Chamber of Industrialized Corn (Canami), National Council of Manufacturers of Balanced Food and Animal Nutrition, AC (Conafab), Crop Protection Science and Technology, AC (Proccyt), National Swine Unification, Ac (Opormex), Mexican Union of Agrochemical Manufacturers And Formulators, Ac (Umffaac), Mexican Association of Food Producers, AC (Amepa).

Downloads

Download a PDF of the policy brief.