A report for the Institute for Agriculture and Trade Policy (IATP) and the Alliance for Food Sovereignty in Africa (AFSA)

Download a PDF of this report here.

Executive summary

This report is intended to serve as an assessment of the World Bank Group’s involvement in African agriculture since 2014, with an emphasis on its investments in livestock agriculture, particularly in East and Southern Africa. The question of WBG involvement has become especially important in recent years as the leading proponents of the so-called “African Green Revolution” have either scaled back their ambitions or, in the case of USAID, collapsed entirely, while the project to reconstruct African agriculture on a continental scale and integrated with global networks of trade and finance which they began in earnest around 2010 continues.

As we discuss in the following report, the leading proponent of this effort today may be the WBG, which has greatly increased its capital expenditures in African agriculture since 2021 and, more recently, has declared its intention to increase that expenditure still further.

Among our findings:

- From 2014 to 2020, WBG financing for African agriculture came out to around $1 billion per year. From 2021 to 2024, WBG financing in this area rose to about $3 billion per year. During the entire period, the WBG committed approximately $12 billion total to livestock projects in Africa.

- Livestock is a popular avenue for agricultural development, not just for the WBG, but for African governments, as well. Out of 49 sub-Saharan African countries, 29 have hosted at least one WBG livestock project since 2014.

- A number of livestock projects emphasize a “productivist” take to agricultural development. Even some projects classified as emergency preparedness or recovery emphasize increasing the productivity of farmers.

- The WBG’s theory of change has long hinged on shifting farmers from agriculture to more “advanced” sectors of the economy. Some livestock projects embody this logic with explicit intentions to reduce the number of farmers in a given country or region.

- With a new emphasis on networked technologies, including AI, the WBG is presenting itself as a vanguard for a new technology-driven approach to agriculture, yet the goals and the overall nature of the African Green Revolution remain essentially since its inception under the leadership of other organizations, such as USAID and the Gates Foundation.

We conclude with some emphasis on the importance of putting farmers at the helm of any effort to transform African agriculture and promoting agroecology as an answer to endemic hunger and nutrition deficits on the continent.

Introduction: A new lead organization for the “Green Revolution in Africa”?

Since its inception around 2010, the so-called “Green Revolution in Africa” (a broad term for a strategy of promoting input and technology-intensive agricultural practices with stated goals of increasing yields, and reducing hunger and poverty) fell more under the purview of the Global North’s developmental aid agencies and philanthropies than its development finance institutions (DFIs). But in the last two years, some of the groups that led the endeavor have either shrunk under or reeled under the moral disgraces of a founder. USAID has imploded under the watch of the Trump administration: As recently as 2022, the agency had obligated $684 million in agricultural assistance to sub-Saharan Africa. For the first quarter of 2026, ForeignAssistance.gov, the U.S. government’s website for tracking aid expenditures, recorded the figure at -$45,445, as the U.S. State Department claws back the late agency’s promises.

USAID’s implosion was a dramatic event, but only the most extreme occurrence of a wider trend towards marginalization of aid on the Global North’s extra-territorial priority list, as European countries including France, the Netherlands, the United Kingdom, and Germany have pared back their own development agencies, ostensibly to spend more on defense.1 Beyond the government realm, Bill Gates, founder and chairman of the Bill & Melinda Gates Foundation, the leading underwriter behind the Alliance for a Green Revolution in Africa (AGRA), has been brought low after a series of revelations surrounding his long association with Jeffery Epstein. As Gates himself said in an apology to staff, the Foundation’s business is largely dependent on his personal reputation: If even being seen with Gates is a hazard, African governments may choose to find other partners.2

The curtailment of these agencies is nothing if not a restructuring of the pillars of Green Revolution in Africa, in and of itself. Despite those setbacks, the Green Revolution in Africa continues — though, perhaps more than ever, the organization that will lead it will be the World Bank Group.

As we discuss in the following report, from 2015 to 2020, the World Bank Group disbursements to African agriculture averaged about $1.1 billion per year. From 2021 to 2024, its annual spending in this area increased to nearly $3 billion. As of 2025, the WBG plans to double its spending on agriculture worldwide, with a focus on Africa. Through its involvement, the WBG is taking the lead in a continent-spanning effort to make the small farmers who still supply a majority of Africa’s food less independent as the benefits of their labor accrue more for agribusiness, deepening a model that has characterized the Green Revolution in Africa since its inception.

For all these reasons, understanding the WBG and the nature of its involvement in livestock will be essential to understanding the near future of the African Green Revolution.

Much of that spending has already gone into livestock — the focus of this report — with projects dedicated to production, processing, and related sectors, and covering a range of agricultural sectors from feed to manufacturing. As we discuss, a few projects also are also dedicated to intervening in pastoral systems.

That is not to say that a focus on livestock production is inherently detrimental. Livestock is a vital component of rural economies across Africa and the world, and has been since pre-colonial times. While the WBG understands that fact well, and promotes it for rural development, it also values livestock as a “high value” agricultural product whose production cycles can join rural areas to urban markets through industrial processes. As we discuss further, the WBG may conflate livestock as a foundation to rural livelihoods with livestock as a component of an industrial process, but doing so highlights an essential contradiction of its efforts, and of the Green Revolution in Africa, more generally.

1. Understanding the World Bank Group

While the terms are sometimes used interchangeably in colloquial conversation, the World Bank and the World Bank Group are distinct entities, each with their own governance structures, and with the former making up the largest entity within the latter’s umbrella organization.

Figure 1.1: Organization of the World Bank Group

Source: World Bank Group

The World Bank

Surely the most famous of the DFIs, the World Bank is the namesake institution of the World Bank Group. The World Bank distributes funding through two subsidiary organizations: the International Development Association (IDA), which works with low-income countries on poverty-alleviating projects, and the International Bank for Reconstruction and Development (IBRD), which works with middle-income countries on projects that connect them to international markets. All the World Bank projects we identified as livestock-related projects are currently funded through the IDA.

The International Finance Corporation (IFC)

The IFC is the WBG’s private sector underwriter. Unlike the World Bank, which generally provides capital to governments, the IFC lends money and takes equity stakes in companies. It has taken on more of a role in African agriculture as the sector has borne more industrial and capital-intensive operations, like meat processing. The IFC also provides “advisory services” to help clients advance their business, both as part of its program of capital support and as a separate offering. In 2025, Africa was the single largest destination for IFC advisory services, accounting for 35% of program expenditures (though the IFC does not disclose how much of that went to agriculture.)

Multilateral Investment Guarantee Agency (MIGA)

MIGA is the WBC’s in-house guarantor. It functions as an insurer for cross-border investments in developing countries, protecting investors from risks of war and non-payment from counter-parties to encourage investment in risky areas. As of 2024, MIGA has housed another entity, World Bank Guarantees, which manages similar risk-reduction offerings from MIGA and the IFC. During the period covered, MIGA’s investments in livestock agriculture in Africa were related to the Silverlands projects in Zambia and Tanzania.

International Centre for Settlement of Investment Disputes (ICSID)

The ICSID is a mediator for international investors. It is unique among WBG subsidiary entities in that it does not provide capital itself.

2. What the WBG says about agriculture

WBG leaders have maintained a longstanding pattern of declaring agriculture, Africa, and, to a lesser extent, African agriculture as priority areas. Though the WBG leaders speak of what they understand to be shortfalls in African agricultural production as if they are the first to notice them, their rhetoric has changed little from the rhetoric of other groups who led it at various stages over the last two decades. In his remarks at the WBG’s latest round of annual meetings, which it held with the International Monetary Fund (IMF) last October, WBG president Ajay Banga said the following:

Agriculture has always been central to development. But today, the real issue is, how do you make it a driver of jobs, how do you make it a driver of income, and how do you get to food security at scale? How to grow more food, but then to turn that growth into a business that produces higher incomes for smallholder farmers and more opportunity across entire economies?3

Banga introduced the matter of turning agriculture “into a business” as if it were a new endeavor, yet proponents of the African Green Revolution have been making the case for more than a generation. The following is from a 2004 World Economic Forum report.

Establishing market linkages and providing needed goods and services to producers and entrepreneurs can raise local food production and incomes … Viable models, when applied on a large scale, have the potential to substantially accelerate Africa’s Green Revolution and its corresponding goals to eliminate hunger and poverty.4

The “business” narrative also papers over an essential fact about African agriculture: Farmers already grow crops for money. Just because they are at the bottom of a market arrangement does not mean they do not act as part of a market. That discrepancy between rhetoric and reality points to a larger issue that, at stake, is not just whether agriculture becomes more profitable (or more “business” oriented), but who controls production, land, finance, inputs, processing and markets, and whether communities retain the right to define their own food systems.

Banga’s comments opened the launch event for the WBG’s AgriConnect initiative (discussed more below). One number, touted during that event, reveals how little the WBG position on the subject has evolved in recent years. Said Tanvir Gill, the host for the event, African agriculture could be “a one-trillion-dollar market by 2030.” (See Figure 2.1.)

Figure 2.1: A still from WBG’s AgriConnect launch presentation

The figure is impressive, but it’s also quite old, first appearing in a widely circulated 2013 World Bank report by Derek Byerlee and others, who made the estimate themselves, based on the rate of growth of African cities and estimates about the purchasing power of urban vs. rural populations. At the time, the World Bank estimated the combined value of African agribusiness and agriculture to be around $313 billion, meaning an increase to $1 trillion would more than triple the value of these industries in less than 20 years.5

With time, other parties have revisited those figures and made their own assessments. As recently as 2023, the African Development Bank (AfDB) estimated the value of “Africa’s agricultural output” (presumably a similar scope as the one covered in Byerlee’s report) to be $280 billion, citing a quote from then-AfDB president Akinwumi Adesina.6 Another estimate circulated by the African Food Show, a trade convention for food and beverage proprietors that do business in Africa, estimated the value of the African food and beverage market to be around $346 billion in 2024, and projected its value to be around $567 billion by 2032 — a far cry from the World Bank’s 2013 estimate.7

Byerlee, et al were optimistic about the future of African food and agriculture, projecting the sector could add around $500 billion in value to the continent per year, compared to $150 billion at the time. However, they stressed that such a monumental change was contingent on a then-$10 billion agricultural trade deficit turning into a $20 billion trade surplus.8 Since their report was released, the deficit has only increased to almost $17 billion. What’s more, only four countries in sub-Saharan Africa have trade surpluses, and two of those countries (Ghana and Côte d’Ivoire) can attribute their surpluses mostly to a heavy reliance on cocoa production.9

Why does the WBG now tout such an optimistic case that is a) more than 10 years old, b) depends on changes that have generally not happened, and c) is contradicted by other, more recent estimates? The reason could be as simple as the fact that “$1 trillion” is an easily shared number and is justified by the WBG’s own numbers (if one doesn’t bother looking at more recent estimates).

Yet perhaps another reason is that the WBG is essentially appealing to two audiences: The first is a general public that includes some specialists and policymakers who are interested in Africa and/or the Global South, broadly, and can get onboard with the overtly altruistic mission of the African Green Revolution but will not be investing themselves. A second group, the investors, are interested in a particular country or sub-region and are only invested in the African Green Revolution to the extent that it benefits their endeavors. The latter group depends on the former group to keep the pressure on African governments to develop “enabling environments” that can better serve their ends. For that reason, it helps that actors like the WBG maintain the illusion that the future is bright and the past irrelevant, as though they are the first to make a serious effort to revitalize African agriculture, despite the fact that many entities have claimed to do exactly that for close to two decades.

Making money, alleviating hunger — what’s the difference?

That dichotomy speaks to a broader issue within the African Green Revolution: people guided by altruism and lofty ideals about development may define its continental scope, but people with often mercantilist ends are the ones who make it real. The WBG and other proponents have long said that altruism and self-interest are entirely compatible, yet the current $17 billion agricultural trade deficit is evidence of a major gap between rhetoric and reality. Investors surely recognize that Africa’s urban populations are growing and becoming more affluent, though they are likely ideologically indifferent to whether it serves those populations via imports or domestic production, and whether domestic production benefits smallholders under something other than exploitative conditions.

Consider the rise of poultry consumption and production across Africa. The IFC has taken a special interest in the trend (see Table 5.1). Most of the cost (and thus a substantial portion of the resulting economic benefit) of poultry production is in feed (typically corn and soy). Small farmers across Africa grow these crops (especially corn), and the WBG has invested in their production, with the IFC making some substantial investments in animal feed processors (such as Bidco) and traders (most notably ETG), some of which support outgrower schemes. Yet feed crops are categorically “low-value” crops, meaning the profits per acre of land is small, and that, almost no matter what kind of support is on offer in an outgrower scheme, only farmers with large land holdings generally stand to benefit. Moreover, in the absence of import controls (which the WBG typically opposes), domestically produced feed crops have to compete with South American imports, which also pushes production towards low-cost operations that small farmers struggle to match.

AgriConnect — the next phase of WBG investment in agriculture

With its new AgriConnect initiative, announced last October, the WBG plans to commit $9 billion of its own capital to agriculture annually by 2030, with much of the funding going to Africa. As described in a January 2026 blog post, under the initiative, the IFC will provide capital while the World Bank will devote itself to “the policy changes and government-led programs needed for success.”10 In this way, the new initiative will function as a vehicle for policy reform and market restructuring, and not just for capital.

Though much about AgriConnect is the same old, same old — supporting large agro-enterprises with some residual benefits envisioned for farmers that service those operations — one thing that may be new about it is the partners involved. Beyond supplying its own capital, the IFC is being tasked with organizing an additional $5 billion from other organizations, including DFIs like AfDB and the International Fund for Agricultural Development (IFAD). Yet at least one partner not previously seen in African Green Revolution projects is also joining — upon signing a compact with Qatar that allowed it to open an office in the country, the WBG and the Qatari government also agreed to discuss Qatar becoming involved as an AgriConnect underwriter in the future.11

The rhetoric of agricultural transformation is also getting an upgrade. Through AgriConnect, the WBG is also showcasing a timely new fixation — AI in agriculture — and aligning itself with various tech industry titans. At the AgriConnect launch, President Banga laid out a vision for how farmers might use AI in the future and how networked technology could incorporate them into a global financial system that has so far ignored them.

Small AI tools and basic phones that can diagnose crop disease from a photograph, that can inform fertilizer choices — it can prompt action well ahead of a weather event and move payments securely. That data trail then becomes a credit history. Better underwriting lowers the cost of capital, lowers costs, draws in more lenders. That’s the virtuous loop that we want to build.12

Banga is not the first to talk up the imminent arrival of AI in African agriculture for the benefit of small farmers, and his comments follow a history of similarly influential enthusiasts talking about how mobile, networked technology can not just allow farmers to access markets, but allow markets to extend themselves to farmers. This is Rockefeller Foundation president Raj Shah speaking at the African Green Revolution Forum in Kigali in 2018:

We can dramatically step up these platforms of innovation to accelerate Africa’s Green Revolution. A future where a farmer can use her smartphone to take a photo of a diseased leaf on a banana tree, send it over SMS to an expert-based artificial intelligence system, and in return, get a precise recommendation for how to treat the disease, with particular inputs delivered to her by drone may represent a viable alternative to traditional and often broken extension services.13

The focus on networked technology is perhaps best understood as one element of a wider agenda of incorporating small farmers into larger industrial processes — in effect, turning subsistence producers into suppliers of regional or international systems of production. In that sense, it advances an agenda that has guided the African Green Revolution virtually since its inception, of reimagining farmers as participants in a globally connected financial system (namely, as borrowers) and as fonts of data for AI platforms which can supplant farmer-serving extension services.

Such an agenda informs much of the African Green Revolution to date, and it speaks to the WBG’s current and recent efforts to advance livestock production.

3. The role & scope of livestock projects in the WBG’s agriculture agenda

The World Bank Group’s theory of development has long been predicated on moving people from agriculture into industrial jobs, like manufacturing. As two WBG economists wrote in a 2022 blog post, “Expansion of better income earning opportunities” hinge on “structural transformations” to the local economy, in part, through “the shift of workers and resources from low-productivity, low-earning sectors such as traditional agriculture to higher-productivity sectors through the more rapid entry and growth of firms.”14 (Emphasis added.)

Within that framework, industrial livestock production has a unique role, as it bridges manufacturing and agriculture. Its raw materials can be locally or regionally sourced, and strong local markets can tee-up export opportunities as the industry evolves. As a nation’s livestock industry grows, it also supports other, interrelated industries, from feed production to veterinary medicine, which the WBG considers worthy of its support.

As the WBG has taken on a greater interest in climate change, livestock has stood out as one of the leading sources of emissions in developing countries, and one of the fastest growing ones, as well. To that end, the WBG has seen yet more reasons to underwrite and transform it (largely in the same way that it has in the past, but with new tracking metrics and new technologies for paring back emissions). As a 2021 WBG paper states, “the WBG has a specific interest in supporting the livestock sector as a core strategy to reduce poverty and promote secure livelihoods in rural areas, while attacking vectors of climate change at source.”

The paper continues:

While donor countries may be able to envisage alternative sources of protein and quality nutrition at scale, developing countries remain dependent on the livestock sector, both as producers and consumers. … [F]or the moment … livestock will continue to make an essential contribution to enhanced nutrition and improved diets in the developing and graduating countries. Ignoring this reality will be costly for the WBG both in terms of its international image and, therefore, its ability to produce change, and in lost opportunities to support struggling rural communities in the face of climate change.15

Both for African farmers and for the world, the risk in treating the same model with new metrics as an adequate response to climate change is that an industrial agricultural model that is at the center of the problem gets repackaged, only with new descriptors and numbers.

Increasing livestock, reducing farmers

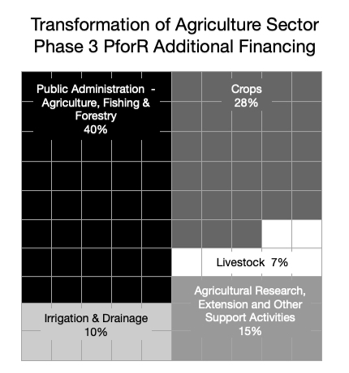

WBG projects are often tied to bigger goals of transformation of an entire country. An illustrative example is 2017’s Transformation of Agriculture Sector Program Phase 3 PforR Additional Financing project in Rwanda. The project represents follow-on financing for a project that was co-funded by multiple governments, including the United States, Japan, and the Netherlands. The goals of this project included “animal resource intensification” and “professionalization of farmers” and was planned with the intent of reducing the number of people working in agriculture. As the World Bank notes, the project was intended to support the Rwandan government’s own goal was to reduce the proportion of people working in agriculture from 70% to 50% by 2020.16

“Intensification” in this case may not mean outright industrialization of livestock production. In a document outlining the project, the World Bank attributes a doubling of total production of milk, meat, fish, eggs, as well as corn and cassava from 2005 to 2015 to policy changes that “enhanced access to better agricultural inputs” for small farmers in Rwanda, not the construction of concentrated feedlot operations. Yet we should not interpret the ostensibly less industrial approach of this project as a turn away from industrialization. We should take the mere fact that this project is intended to reduce the number of farmers working in Rwanda as evidence that the government of Rwanda and the project funders, including the WBG, very much favor that mode of development. Even with substantial capital invested and the government interested, industrialization is a process, and often a long one, but it is one to which African Green Revolution proponents are no doubt committed.

4. Geographic coverage of WBG meat & feed, production & processing projects

While most projects for either bank are specific to a single country, the IFC has initiated four projects since 2014 that cover multiple countries in Africa. The World Bank has similarly initiated 18 projects that are regional.

Figure 3.1: WB & IFC projects by country, 2014-2025

Ethiopia has hosted more projects than any other, which is not surprising considering the historic place of livestock agriculture and its more recent standing as a center for agricultural development, though a number of countries that are not known for livestock production are also on the list. As you can see in Figure 2.2, WBG livestock investments over the past 10 years have touched most sub-Saharan African countries — though notably, not some higher-income countries, including several where the livestock industry is rapidly developing such as Angola, Ghana, Namibia, and Botswana.

Table 3.1: WB and IFC projects by country (excluding dropped projects)

5. The World Bank’s investments in African agriculture & livestock

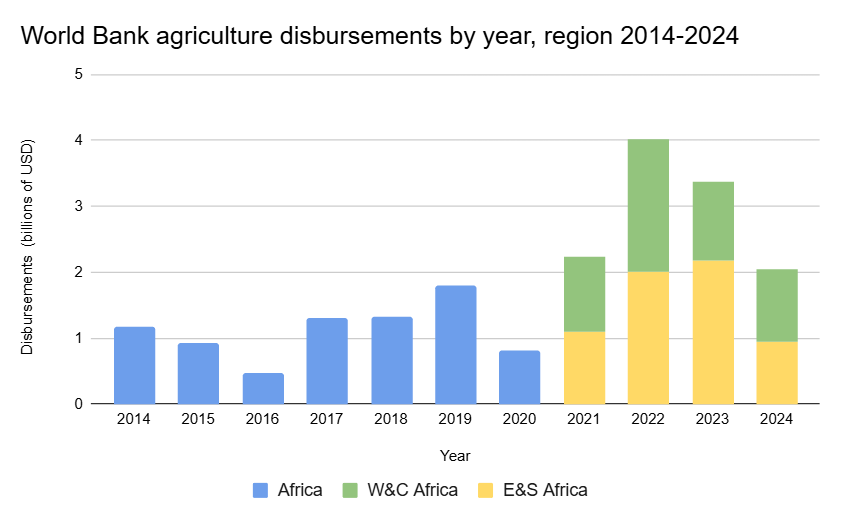

Through a review of its annual reports, we were able to assess the World Bank’s disbursements to agricultural projects in Africa from 2015 to 2024. (“Disbursements,” or the capital the World Bank spent, are the only figures available in the annual reports and differ from “commitments,” or the capital it has decided to spend. Since commitments generally speak to the World Bank’s strategic direction, we used these figures when available and disbursements when they were not.)

Figure 4.1

Figure 4.1 shows the World Bank divided its disbursements to Africa into two regions starting in 2021. The change coincided with a substantial rise in spending. In 2021, World Bank disbursements to East and Southern Africa alone outdid disbursements in three of the previous six years.

While the rise in disbursements appears to follow a general rise in disbursements to Africa across sectors, the World Bank did increase the proportion of its capital disbursed to agricultural projects during this time. From 2015 to 2020, agriculture constituted 8.5% of World Bank disbursements in Africa, on average. From 2016 to 2024, those disbursements made up 9.25% of its disbursements to East and Southern and 11.5% of its disbursements to West and Central Africa, on average.

The World Bank scaled down its investments in 2023 and 2024, from a peak of $4 billion in 2022.

As of this writing, the World Bank has not listed a figure for agricultural projects in Africa in its 2025 annual report, nor has it added any livestock projects for 2025 on its list of projects.17 But we can assume the absence is not due to a lack of investments, only that the World Bank has yet to list those projects as of this writing. With the WBG’s deployment of its AgriConnect initiative over the next four years, we can expect the Bank to increase its disbursements substantially in the near term.

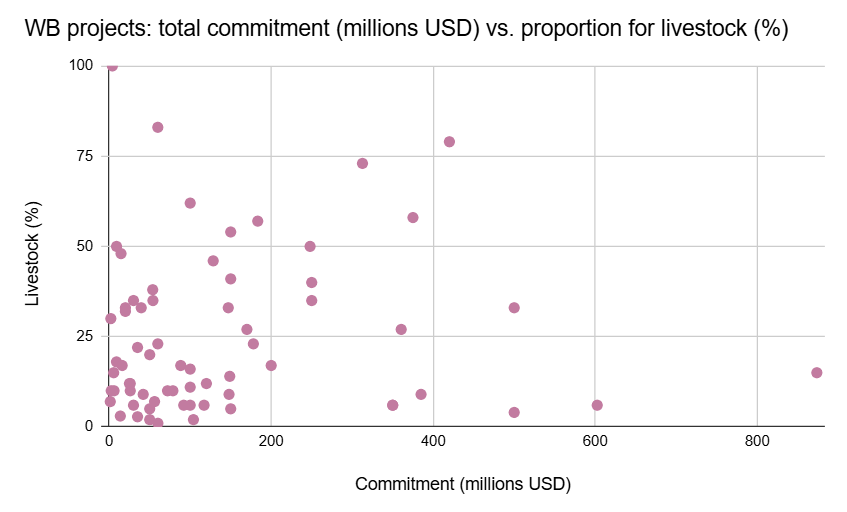

World Bank commitments to African livestock

To assess World Bank support for livestock in Africa, we generated totals from the commitment figures listed in individual project reports, and not disbursements, as listed in the World Bank’s annual reports. In total, we identified World Bank commitments to livestock projects totalling $12 billion in 31 countries. Projects in East and Southern Africa accounted for $7.2 billion, of which $2 billion came from the Strengthen Ethiopia’s Adaptive Safety Net project in 2020, which was intended to greatly expand an existing government social safety net program in rural, drought-prone parts of Ethiopia, partly by supporting livestock production (see Figure 4.2).

Figure 4.2

Characteristics of World Bank investments in livestock

Livestock is a popular mode of development project. A majority (29 of 49) countries in sub-Saharan Africa have taken on a WBG-backed livestock or related agricultural project in 2014 to 2025.

While we only looked at projects that the World Bank identified as benefiting the livestock sector, of those projects, on average, the World Bank marked only around 25% of the allocated funds for “livestock.” In keeping with its historical role of using capital to shape the conditions within which private capital operates, even projects that are explicitly intended to serve a country’s livestock sector typically cover multiple related areas, with allocations for “crops,” “health,” and a sizable portion dedicated to the local government, often related to the oversight of the livestock sector.

Setting aside Strengthen Ethiopia’s Adaptive Safety Net, a 2020 project which the World Bank made an extreme outlier with a commitment of more than $2 billion, the average project commitment was $128 million, and most projects involved commitments below $200 million. (See Figure 4.3).

Figure 4.3

There is no significant difference in capital commitments between projects in East and Southern Africa and sub-Saharan Africa, more generally.

Identifying themes in World Bank livestock investments

Unlike the IFC’s investments, which generally target a particular company, World Bank lending tends to focus on a particular development goal or group of goals. We identified seven themes that most (73 of 79) of the World Bank projects relating to livestock incorporate. (These themes rely on our own nomenclature and do not come from World Bank documents.) Note that most projects touch more than one theme.

Table 4.1: World Bank projects by theme

Looking at how the various themes relate to the projects, some interesting differences emerge. As you can see in Table 4.1, there is an apparent division between projects related to pastoralism and others that prioritize enhancing productivity. In all, 33 of the projects incorporated pastoral or productivist themes, however only four align with both themes.

Productivist projects can also follow some notable patterns:

Industrialization / value chain projects

Society-wide transformation is a major goal across Green Revolution projects. If only for that reason, a project that is primarily about agriculture can include a number of other priority areas. The Transformation of Agriculture Sector Program Phase 3 PforR Additional Financing project in Rwanda (discussed in Section 3) is illustrative: As you can see in Figure 4.4, slightly more than a third of the project’s financing was slotted for “livestock” and “crops.” The largest share appears to have been reserved for the government to bolster its own administrative capacity in managing the desired transformation of the agricultural sector.

Figure 4.4

Emergency projects that are also productivist projects

Emergency support (in the form of both funds for recovery after disasters and for preparing for future disasters) is a major variety of World Bank support. Yet, beyond recovery and preparedness, it appears the World Bank uses emergency lending not just to provide relief, but to advance an industrial agricultural model. Out of 20 projects we identified as projects intended to aid a country or region through an emergency, recover from one, or prepare for future emergencies, seven appeared to have some kind of productivist component. For instance, the stated goals of the 2022 Emergency Project to Combat the Food Crisis in Cameroon were to “strengthen food and nutrition security” and “increase resilience to climate shocks” of various households and producers.

Cameroon was at risk of famine due to conflict, food inflation, and adverse weather conditions.18 While the emergency food assistance was one component of the project, the rest was mostly focused on increasing farmers’ productive capacity and enhancing their connections to markets in the name of bolstering food security.19 In effect, it was a typical African Green Revolution project, dressed with added urgency and some emergency food aid.

6. The IFC’s investments in African livestock

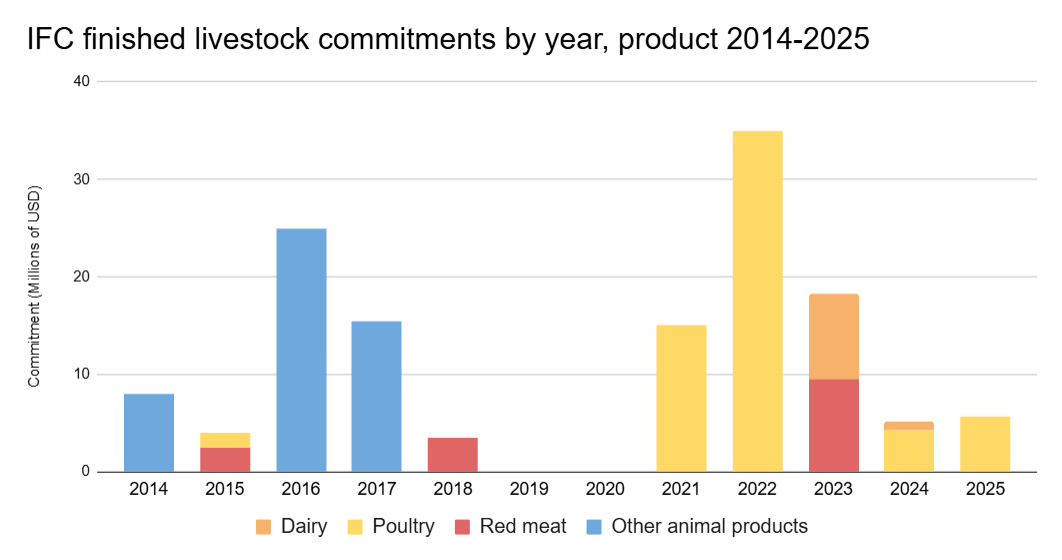

Since 2021, the IFC’s commitments have shifted further upstream, away from processing operations that deal in animal products and towards livestock production. One way to think of the trend is that the IFC is now underwriting fewer companies that make chicken-flavored bouillon and instead more companies that make chicken. (See Figure 5.1.) True to its development mission, the IFC has also shown a willingness to underwrite operations in countries lacking “mature” livestock industries, with investments that include a poultry company in Mauritania and a beef company in Madagascar.

Figure 5.1

It’s harder to discern a pattern in IFC’s financing of companies producing livestock precursors, or inputs, like soy and veterinary medicines, as the vast majority of these companies produce goods for humans and not just for livestock. (See Table A.5.)

IFC case study: Zambeef

The largest agribusiness company in Zambia, and surely the most sought-after meat producer in sub-Saharan Africa (at least outside South Africa), Zambeef makes not just its namesake meat, but pork, chicken, eggs, milk, animal feeds, cheese, and (leather) shoes.

The company is also a major beneficiary of DFI support, having received multiple rounds of IFC financing since 2010. According to its most recent annual report, BII is its largest shareholder, after the DFI acquired a 38% stake in 2016.20

Much of what makes Zambeef unusual in the region is also what makes it an attractive investment. It is a “vertically integrated” operation, more so than one sees in dominant beef-producing countries like the United States and Brazil. While it works with a network of farmers and ranchers, much of the company’s operations are consolidated under its own direct control. Zambeef grows its own corn, raises its own cattle, processes its own meat, then sells the meat under its own labels and at its own stores. The depth and breadth of Zambeef’s operations mean that any influence exerted over the company registers across the entire food system in Zambia, and beyond it. As Keiron Audain noted in a recent AFSA report, Zambeef’s continued expansion entails a greater reliance on input-intensive monocropping in every country from which it sources feed.21

In its poultry and dairy operations, Zambeef relies on a network of farmers to whom it supplies technical support and basic goods, like day-old chicks, in exchange for a guaranteed market. As of 2025, about 10,000 small farmers service Zambeef’s cattle operations alone.22 Despite the enormity of its influence on the lives and livelihoods of African farmers, there is only very limited research available on the company’s relations with the farmers in its network.

In her 2018 dissertation at the University of Pretoria, Rebecca Kiwanuka Namulindwa (now a professor at the University of Zambia) found that slightly less than a third of the 39 small farmers who supplied dairy to Zambeef said the company did not understand their needs. Some specific complaints that farmers shared with Kiwanuka Namulindwa reveal a company that leverages its purchasing power to the detriment of farmers. Farmers said that Zambeef did not certify milk at the point of collection, and often waited to bring it to their own processing facilities after it had spoiled, in which case they paid the farmer nothing. Farmers also said that Zambeef used a system to assess milk volume that was different from the system used at the point of collection, and often reported collecting less milk than they actually had. A broader theme in the complaints was that Zambeef seemed to treat dairy farmers who supplied it as competitors instead of essential contributors to their operations.

Despite these issues, at least within this particular study, Zambeef did not appear to stand out among large dairy buyers. Farmers that supplied the other two that Kiwanuka Namulindwa investigated (Parmalat Zambia and Mpima, a dairy cooperative) also had similar and other complaints, and the vast majority of farmers interviewed (34 of 39) said that Zambeef treated them fairly. Levels of trust were similar for the other companies.23

OPIC case study: Silverlands

The name “Silverlands” pertains to several different agricultural projects controlled by the U.K.-based private equity group Silver Street Capital which have benefited from various DFI investments since their inception in East and Southern Africa. Other underwriters have included the BII (at the time known as CDC), OPIC (since reorganized under the U.S. Development Finance Corporation), and the Danish International Investments Fund. Two Danish pension funds have also invested. But the OPIC investment was unique within this group in that it benefited from a MIGA guarantee.

Silverlands is notable for its sophistication, and the way it closely tracks with the broader goals of the Green Revolution in Africa, noted in the 2018 report Mapping Financial Flows of Industrial Agriculture in Africa, Silverstreet provided health and sanitation facilities for local farmers to take their cattle. The company described this offering as an act of charity (in its words, a “community engagement” project), and also a benefit to its own business, as it would ensure a steady inflow with a “regular, healthy source of cattle” into its own feedlots.24

As MIGA noted when it made its guarantee for the OPIC investment in Silverlands Ranching in Zambia in 2014, its support was meant to help the company expand one of its ranches and increase its production of cattle. Silverlands did not slaughter or process the cattle itself, but it sold them to area processors, including Zambeef, making the company an internationally connected node in a growing industrial livestock system.25

7. Taking a stand against the WBG

People looking to resist WBG projects have limited means for doing so. However, formal channels do exist for people who are, or expect to be materially affected by WBG projects. In the case of the World Bank, that channel is called the Accountability Mechanism (AM). The corresponding channel for the IFC and MIGA is called the Office of the Compliance Advisor Ombudsman (CAO).

The specific criteria for each channel varies slightly, however, for a complaint to qualify at either the AM or the CAO, it must come from someone who is (or expects to be) materially affected by a WBG project. The AM and CAO complaints processes are meant to ameliorate these material harms with material compensation. One way that it can work is that a group of people loses their farmland (and thus their livelihood) to a WBG project and then the WBG gives them money to partly compensate for the loss. Even this process can take years and be enormously cumbersome.

The material harm threshold is critical because it excludes organizations — even ones with members who live in the project area — who oppose a given project because, for instance, it threatens a market and thus undercuts their livelihood, though indirectly.

Complaints at the AM must also come from a group (defined as two or more people), and the group must live in the project area. Anyone filing a complaint will also have to document that they raised the issue with the World Bank in the past, but were unsatisfied with the response.26 The CAO limits harms to “environmental” or “social” harms, though both categories are broadly defined.27 Projects funded by a “financial intermediary” (such as a commercial bank or a private equity fund) can also qualify, if the people filing a complaint can show the intermediary benefited from IFC or MIGA support. Only active projects qualify for complaints.

Anyone looking to file a complaint with the AM related to a World Bank project can find more information on their website (https://accountability.worldbank.org/en/file-complaint). Anyone looking to file a complaint with the CAO concerning an IFC or MIGA project can find more information on their website (https://www.cao-ombudsman.org/).

One organization that has had considerable experience using the CAO process against a livestock operation is the Accountability Counsel in San Francisco. This group has led an ongoing and years-long campaign against MHP, a massive poultry operation in Ukraine that has committed numerous, documented harms against locals and still benefited from considerable IFC financing.28 Their contact information is available on their website (https://www.accountabilitycounsel.org/).

8. Conclusion

The greater role of the World Bank Group in advancing the African Green Revolution agenda in recent years is illustrated by the substantial increase in disbursements focused on agriculture for the continent. From 2021 to 2024 the average annual amount was nearly three times higher than from 2015 to 2020. A majority of countries in sub-Saharan Africa have taken on a WBG-backed livestock or related agricultural project from 2015 to 2024.

Recent spending uses the same rhetoric that technologies will benefit small farmers, but with a new spin on AI and networked technologies. Increasing productivity also continues to be a common theme, although directed in ways that reduce the number of people working in agriculture, and increase reliance on industrial supply chains.

The WBG is strategically positioned to become the principal actor in agricultural financing, policy shaping and private-sector engagement across Africa. This analysis points to a need for more transparency at the WBG, and more accountability for its lack of progress in achieving the stated goals of alleviating poverty and hunger. For now, the WBG’s enormous capital resources are poised to deliver a future committed to industrial agriculture in Africa, one that reduces the role of farmers to debtors and suppliers for “value chains” that they cannot influence.

While the WBG claims this move will alleviate climate change and raise small farmers out of poverty, history shows that it will not. A future rooted in agroecological livestock systems, pastoralism, public extension, local feed systems, territorial markets, and greater policy autonomy could do much more to achieve its stated aims, for the benefit of African farmers and the world.

Download a PDF of this report.

Endnotes

3. World Bank Group. “2025 Annual Meetings | AgriConnect: Farms, Firms, and Finance for Jobs #wbgmeetings.” YouTube video, October 14, 2015. https://www.youtube.com/watch?v=WIenndKR1m8

8. Growing Africa: Unlocking the Potential of Agribusiness.

12. World Bank Group. “2025 Annual Meetings …”

13. AGRF Forum. “The Great Debate.” YouTube video, September 7, 2018. https://youtu.be/GN6JULmLty4?t=133

17. Looking at the IDA’s disbursements across sectors, we see that disbursements to Africa have increased only 2% from 2024 and 2025, as disbursements increased by about 12% to East and Southern Africa and decreased about 10% in West and Central Africa. See World Bank Group. “Creating Jobs, Growing Economies: Annual Report 2025.” 2026. https://documents1.worldbank.org/curated/en/099503310092520301/pdf/SECBOS-8b71cac3-074c-43c1-ac8c-c3b5fc34cb5b.pdf

23. Kiwanuka Namulindwa, Rebecca. “Participation of smallholder farmers in Zambia’s dairy value chain through interlocked contractual arrangements and its impact on household income.” Dissertation, University of Pretoria, February 2018. https://repository.up.ac.za/server/api/core/bitstreams/9c92ac4a-3360-47be-b172-891114b5dec4/content

24. Rock, Joeva and Alex Park. “Mapping Financial Flows of Industrial Agriculture in Africa.” Report for Thousand Currents. November 2018.