Executive Summary

Thirteen of the world’s largest dairy corporations combined to emit more greenhouse gases (GHGs) in 2017 than major polluters BHP, the Australia-based mining, oil and gas giant or ConocoPhillips, the United States-based oil company. Unlike growing public scrutiny on fossil fuel companies, little public pressure exists to hold global meat and dairy corporations accountable for their emissions, even as scientific evidence mounts that our food system is responsible for up to 37% of all global emissions.

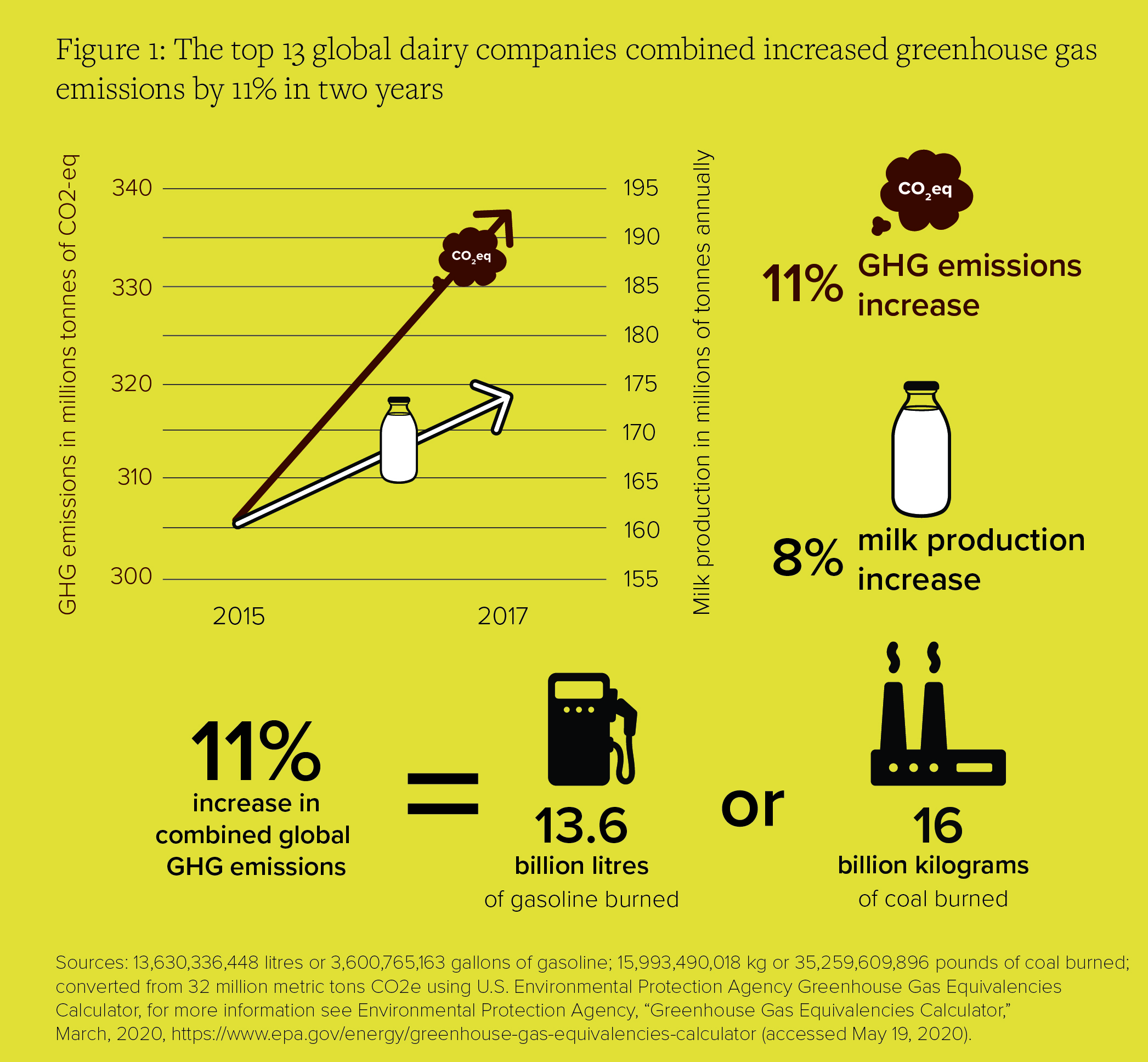

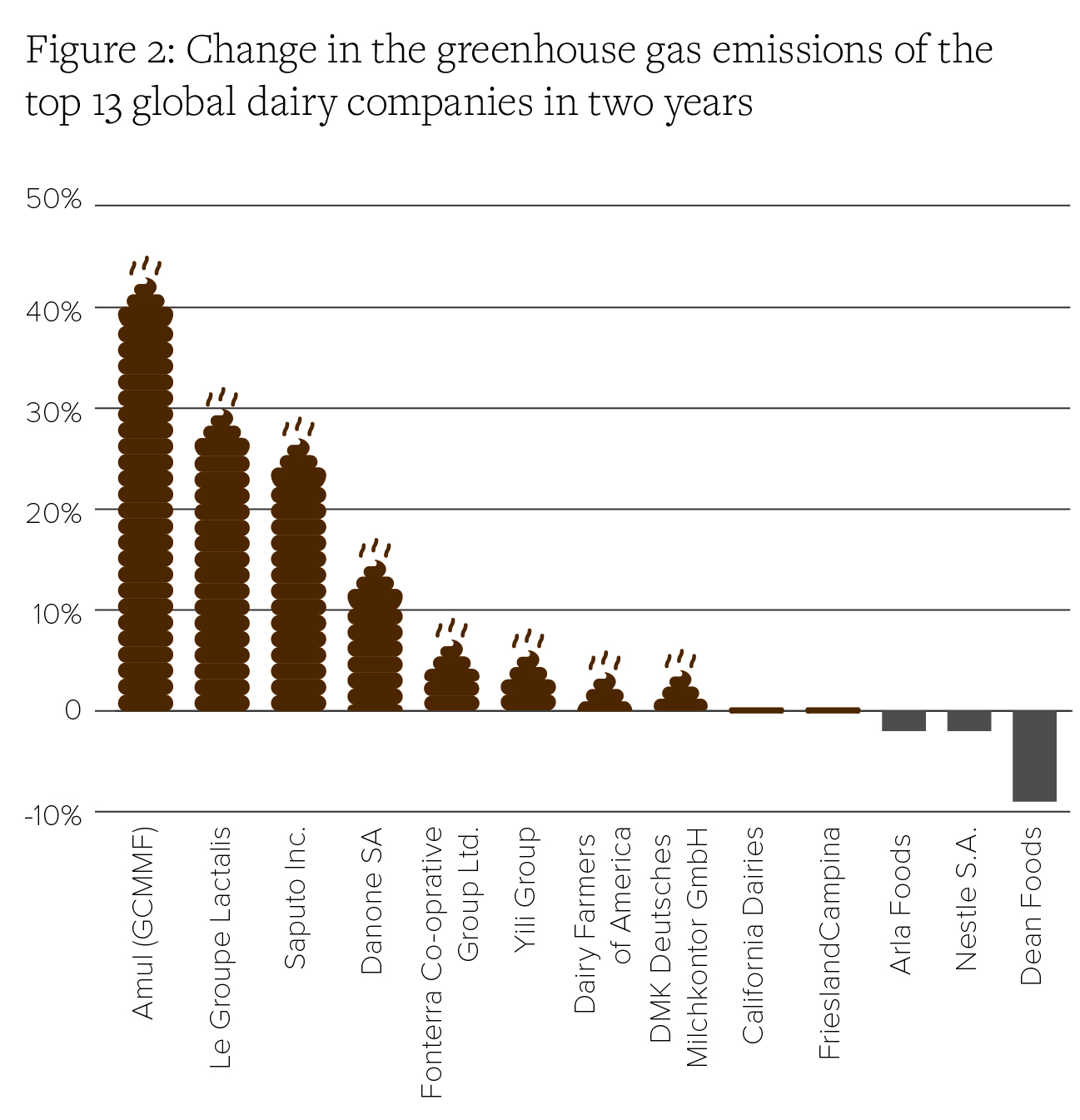

The total combined emissions of the largest dairy corporations rose by 11% (Figure 1) in just two years (2015-2017) since we last reported on them. Even as governments signed the Paris Agreement in 2015 to significantly rein in global emissions, these companies’ increase of 32.3 million tonnes (MtCO2eq) of GHGs equates to the pollution stemming from 6.9 million passenger cars driven in one year (13.6 billion litres or 3.6 billion gallons of gasoline). Some dairy companies increased their emissions by as much as 30% in the two-year period (Figure 2).

The emissions rise occurred amidst a dramatic crash in global dairy prices in 2015-2016. This crash was fueled partially by increased production from mega-dairies and global dairy corporations that dumped excess dairy into the global market, pushing prices down below the cost of production and forcing out many small to mid-sized dairy farmers. COVID-19 has dramatically compounded the dairy crisis rural communities face (COVID-19 box).

Since our first global assessment in 2018 with GRAIN, Emissions Impossible: How big meat and dairy are heating up the planet, the global dairy industry has continued to expand and scale up into new territories through mergers and acquisitions, expanding its collective production by 8% in just two years (Annex 1).

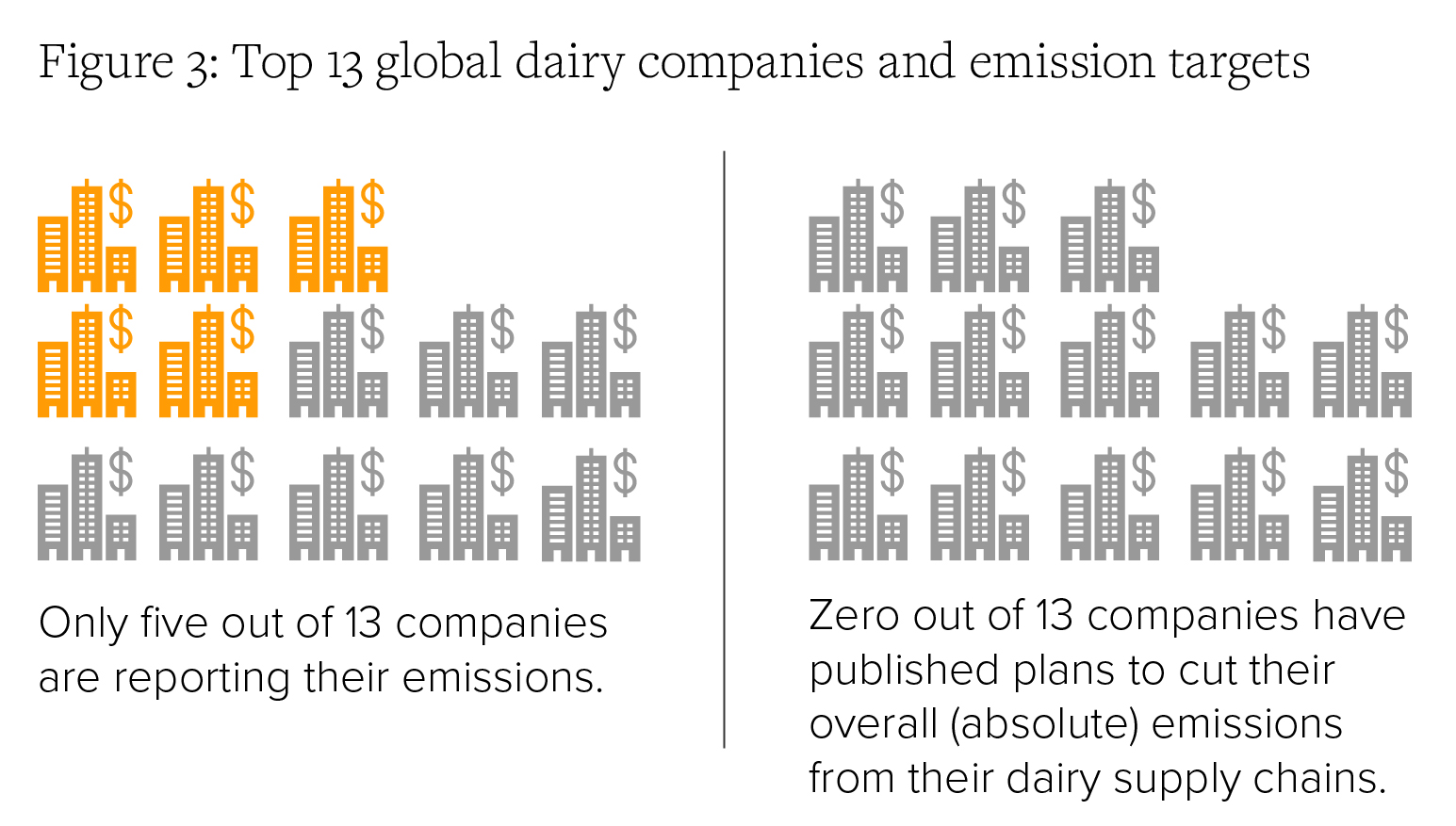

None of these companies are required by law to publish or verify their climate emissions or present plans to help limit global warming to 1.5˚C. Fewer than half of these companies are publishing their emissions (Annex 1 and 2). Zero out of the 13 have committed to a clear and absolute reduction of emissions from their dairy supply chains or emissions from the animals themselves.

Emissions Intensity

Reducing emissions per litre of milk hides environmental costs of overproduction

Emissions from dairy animals in the supply chain account for over 90% of corporate dairy emissions. Yet, only three companies out of the 13 have pledged to address scope 3 (dairy supply chain) emissions to any degree (Annex 2). Companies such as Danone and Arla track their supply chain emissions through “emissions intensity” reduction targets. However, what ultimately counts for a warming climate is whether these companies are reducing their overall emissions at a scale that matters, not their emissions reductions per litre. For example, a FAO study reveals that while the industry reduced emission intensity by 11% between 2005-2015, its overall emissions increased by 18% in that same period.

The European Union (EU), United States (U.S.) and New Zealand alone account for nearly half (46%) of all global dairy production. The companies headquartered in these and other industrialised countries account for the lion’s share of global dairy emissions, and these governments are the best placed to enact policies that enable a Just Transition for dairy producers towards much more climate resilient and agroecological practices in line with ambitious 2030 and 2050 emissions reduction targets.

Dismantling supply management, hastening rural and climate crises

Governments must begin to address both the rural and climate crises associated with the dairy sector by listening to rural communities about their economic and social needs. Fewer and much larger mega-dairies are flooding the market, pushing out small to mid-sized dairies and hurting rural economies. There is growing support for supply management, a crucial policy that could address dairy’s twin crises. Supply management schemes prevent overproduction, balance supply and demand and stabilise prices.

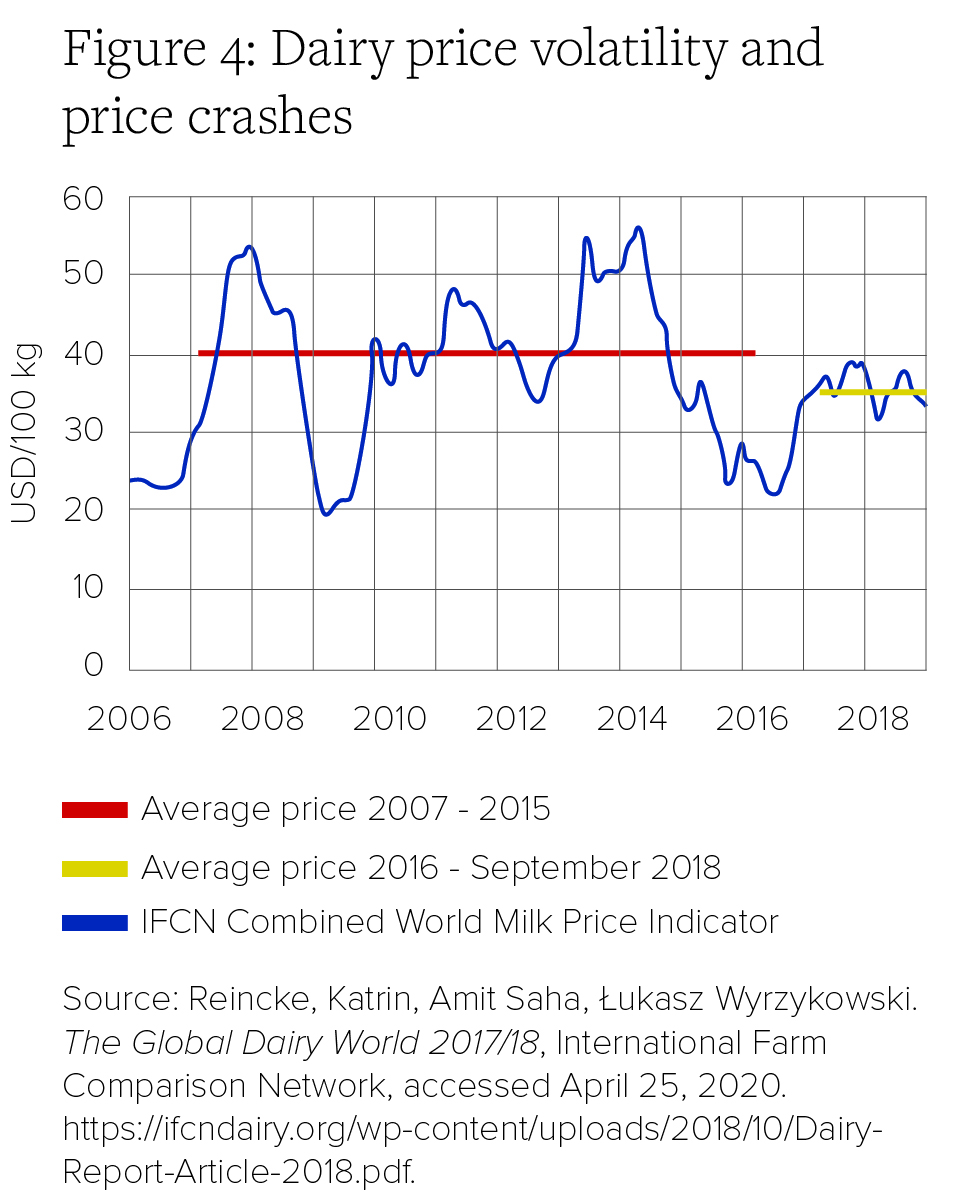

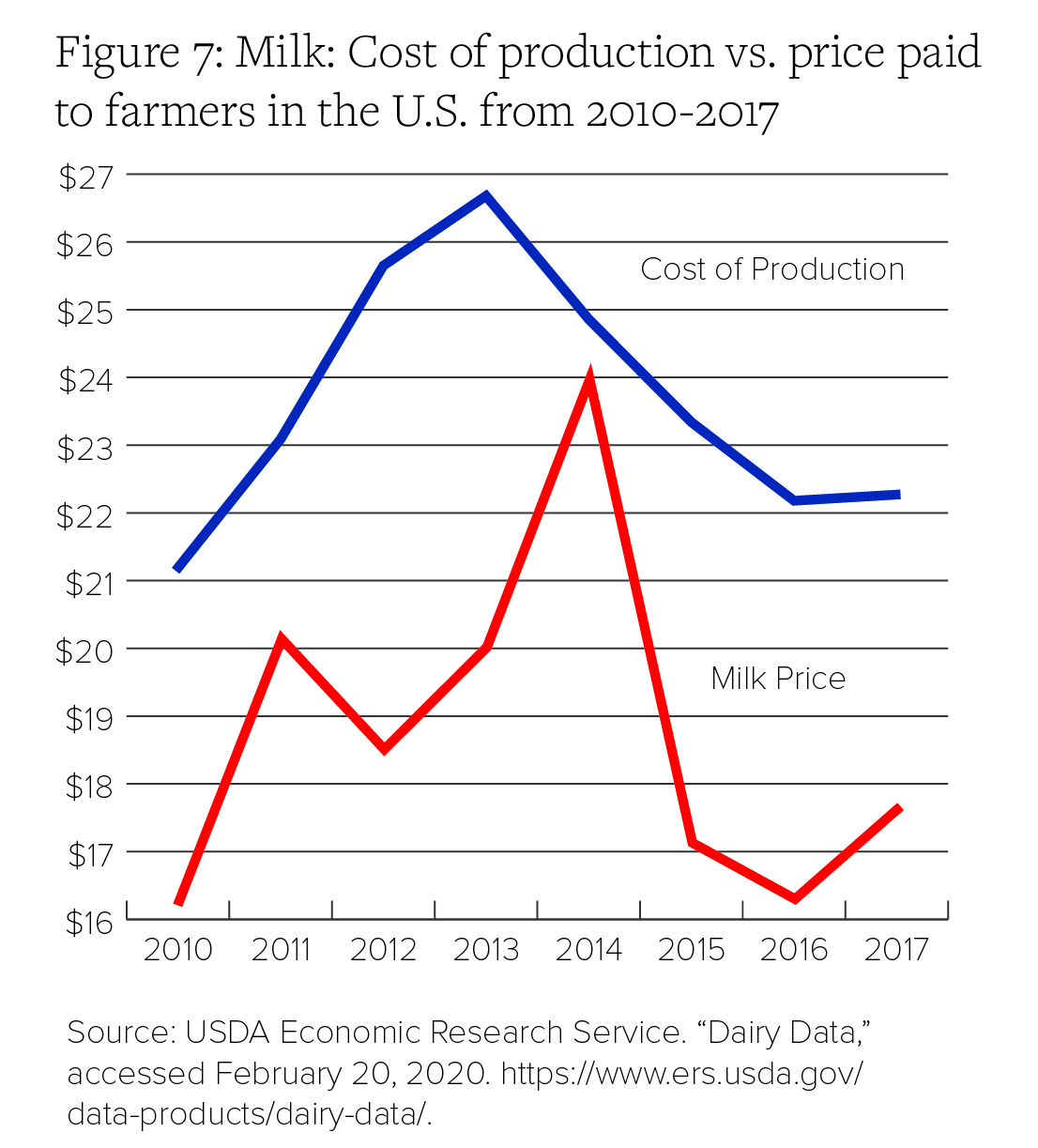

In their absence, global dairy prices have become volatile with boom and bust cycles. From 2008-2018, the global dairy price crashed twice (Figure 4). Competition policies (or lack thereof) in favour of large corporations have further increased corporate buyer power by driving mergers and acquisitions, pushing down prices even more. Dairy prices for the last decade and more have been below the actual cost of production (Figure 5A and 7).

The COVID-19 crisis is amplifying calls for supply management

As countries shut down and corporations stopped buying milk, farmers have been forced to dump milk on the streets. The European Milk Board, representing over 100,000 producers, is calling on governments to implement a Market Responsibility Program that triggers supply controls in various stages when the milk price begins to fall below a certain index. U.S. family farm groups are pointing to their Canadian neighbors to advocate for the return of supply management.

Global Dairy Crisis

The view from four regions

As market concentration and production has increased in every major dairy production region, indebtedness, farm loss and bankruptcies in rural communities have also increased:

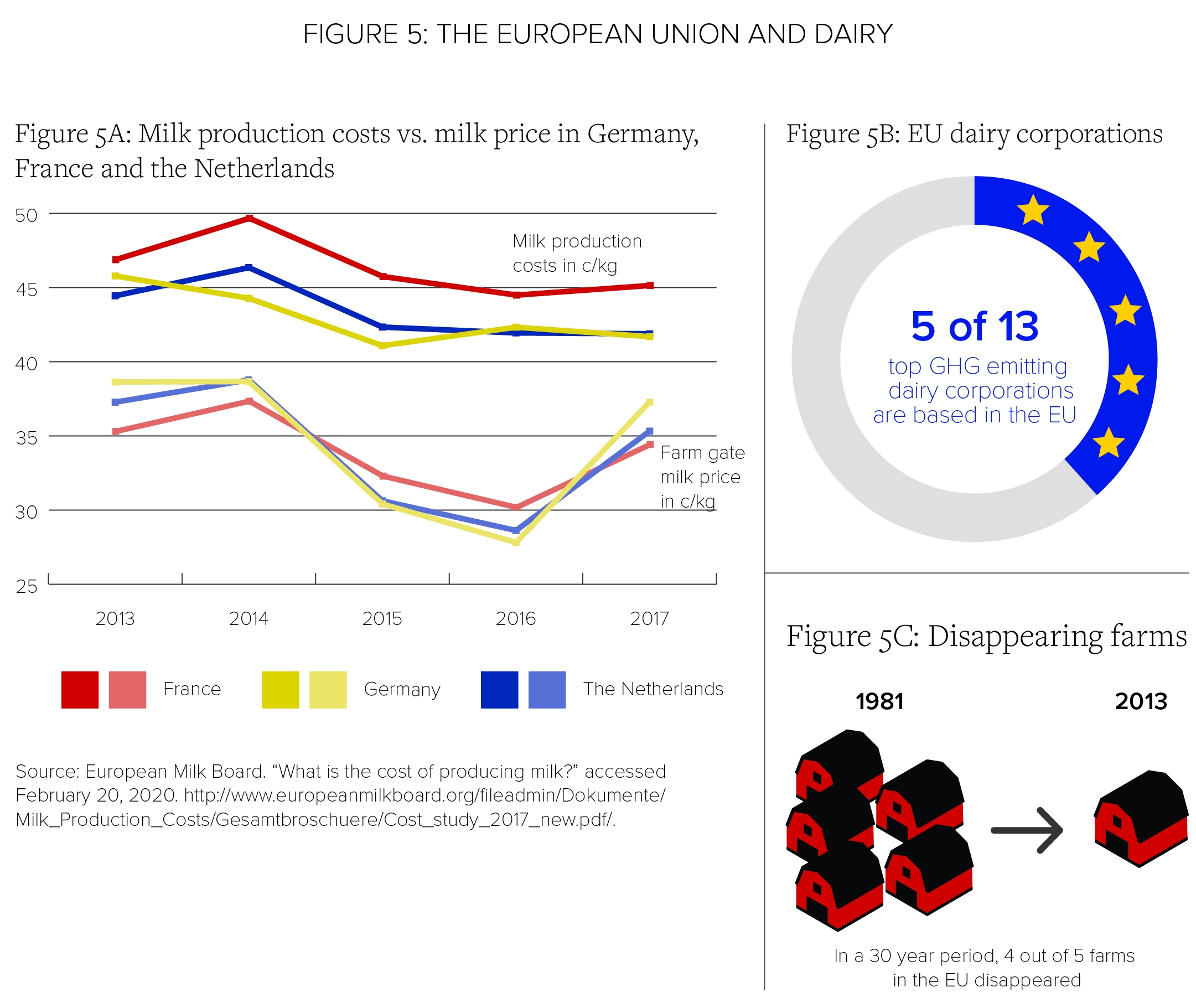

EU: Four out of five dairy farms disappeared between 1981-2013 (Figure 5C). EU’s milk quota removal in 2015, along with other factors, contributed to the second global dairy crisis in 10 years. The EU accounts for over a quarter of the world’s exports. Its dairy corporations remain competitive in the global market by paying EU farmers below the cost of production and dumping “cheap” dairy exports into developing country markets. If the EU is serious about its climate ambition, not only must the EU dramatically reform the Common Agriculture Policy (CAP) to incentivise environmental resilience, but also regulate the market so that companies pay producers their cost of production plus a reasonable profit.

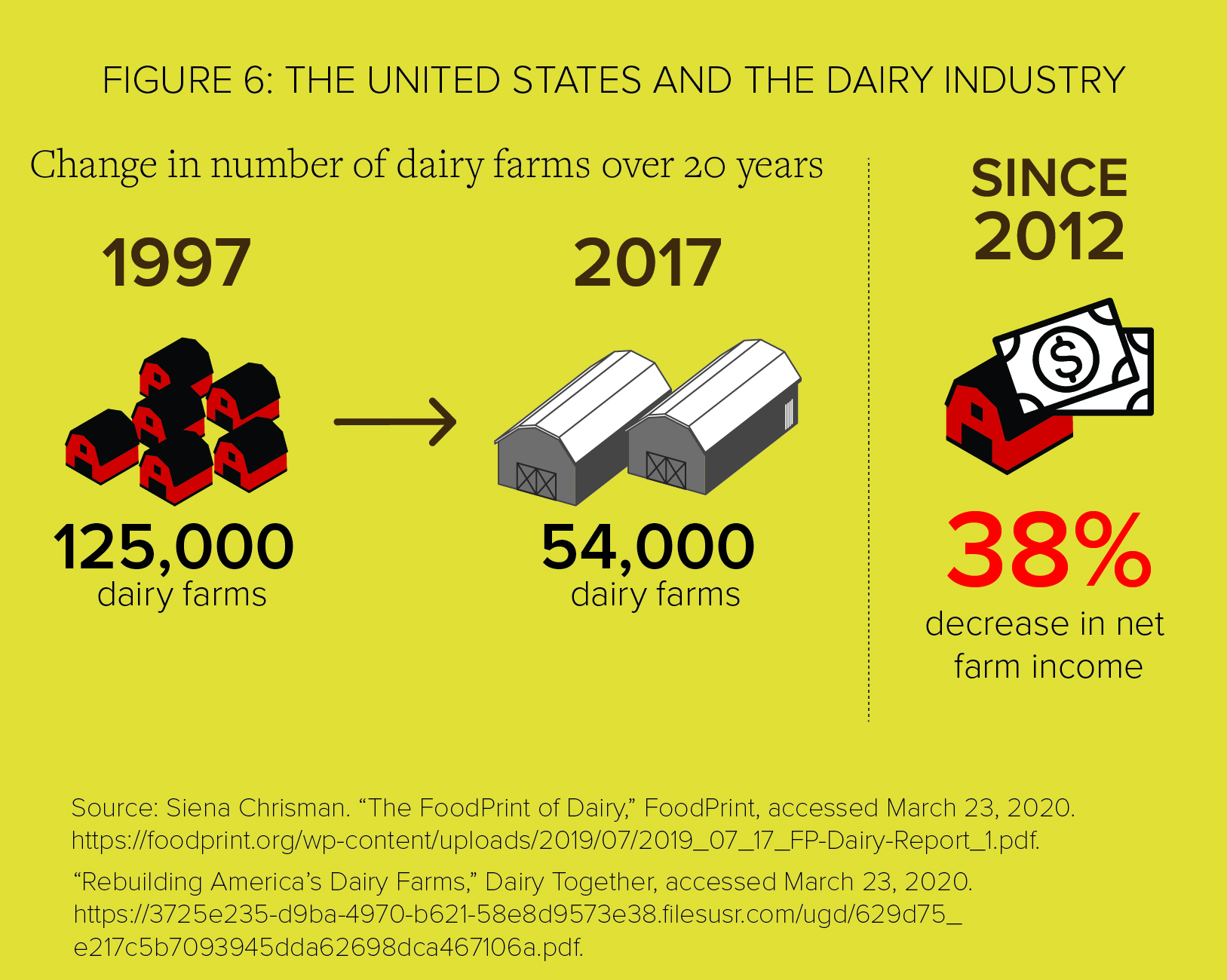

U.S.: 93% of family farms have shuttered since the 1970s. Yet, overall dairy production in the U.S. continues to rise due to new or expanding mega-dairies. These are often funded by outside investors and propped up by a number of Farm Bill programmes. The lack of environmental enforcement, particularly of their GHG emissions, further abets mega-dairies.

New Zealand: Half of the country’s emissions come from the livestock sector, agricultural emissions having risen by 12% since 1990 with the doubling of its dairy herd and a 600% increase in fertilizer use. New Zealand exports 95% of its milk, largely through Fonterra, the world’s second largest dairy processor. Fonterra’s nearly 10,000 farmer shareholders incurred huge losses last year, calling into question Fonterra’s corporate structure and investment strategy. In 16 years (2003-2019), New Zealand’s on-farm debt increased by NZ$30.1 billion. In 2019, New Zealand became the first country to set GHG reduction targets for agriculture in its new Climate Law.

India: India’s Amul, a state-supported dairy cooperative, recorded the largest increase in emissions due to the massive increase in production between 2015-2017. However, unlike Fonterra or Lactalis, Amul’s emissions are embedded in a complex relationship between millions of Indian dairy producers and government policies. Over 16.5 million farmers are integrated into Indian dairy cooperatives such as Amul and Mother Dairy, one-third of them women. Between 2013 and 2015, India went from exporting 130,000 tonnes of skim milk powder to just 30,000 tonnes. The rest was reconstituted into liquid milk and dumped into the Indian market at low prices — sending small dairy producers and local markets into a tailspin. In the last 16 years, over 5.2 million households with one or two cows have stopped dairying. With growing feed and fodder shortages, feeding animals constitutes 60-70% of the costs of Indian dairying, squeezing poorer farmers out of the market. The Government of India plans to double its milk processing capacity by 2025 with policies that seem to be driving India’s dairy sector away from benefitting the poor and marginalised towards a highly capitalised industrial system of dairying.

Way Forward

Redirect, Regulate, Regenerate

There is an exit out of this dead end: by redirecting public funds away from industrial agriculture, regulating the public health, environmental and social impacts of this extractive model of production and designing incentives to regenerate rural communities through agroecology.

There is growing public support in the U.S., the second largest milk producer, for a dairy supply management system to limit production and ensure that small and mid-sized dairy farmers stay on the land. There are rising calls for a U.S. moratorium on new and expanding large-scale confined animal feeding operations (CAFOs). New national-level climate policy also must place restrictions on GHG emissions from large-scale, high-emitting CAFOs.

In the EU, the CAP negotiations present perhaps the last opportunity to overhaul the perverse system of public subsidies that benefit large operations and perpetuate a destructive model of agriculture. The next reform, along with a genuine European Green Deal, must help catalyse a shift towards agroecological systems that support rural communities, while preventing harm to small producers in the Global South.

New Zealand’s new climate law must be implemented in tandem with new trade and agriculture policies that diversify the economy away from its addiction to dairy exports. This will require a dramatic reduction of the country’s dairy herd and the government to help dairy producers and workers transition justly to agroecological systems of production and other means of employment. New Zealand’s rural communities and the environment would benefit, and the country would be less dependent on a fickle global market.

Finally, proper implementation of India’s National Food Security Act through financial and policy support will help revitalise local and decentralised dairy markets. Thoughtful and progressive agriculture, climate, trade and investment policies that holistically uplift the multifunctional role of animals in Indian food and farming systems would help support millions of small and marginal producers. Furthermore, such policies must strengthen the protection of natural resources and respect human and indigenous peoples’ rights.

Governments need to begin by integrating climate goals within their national-level farm policies. These climate goals should address strategies to build climate resilience and reduce emissions. Critically, trade rules must be reformed, having thus far driven an export-focused agriculture system while ignoring the climate. International development aid also needs to support an integrated set of social and environmental measures for agroecological systems that support small-scale producers in the Global South.

For a real climate revolution in the agriculture sector, governments have to transform farm and climate policy in a way that shifts power away from these corporate drivers. They must be courageous enough to enact policy change towards agroecological systems that empower rural producers to do the right thing for their families, communities and the planet.

Key findings

Thirteen of the world’s largest dairy corporations combined to emit more greenhouse gases (GHGs) in 2017 than either BHP, the Australia based mining, oil and gas giant or ConocoPhillips, the United States-based oil company. Both make the world’s top 20 list of the biggest fossil fuel emitters, also known as the carbon majors.1 However, unlike growing public scrutiny on fossil fuel companies, little public pressure exists to hold global meat and dairy corporations accountable for their emissions, even as scientific evidence mounts that our food system is responsible for up to 37% of all global emissions.2

The total combined emissions of the largest dairy corporations rose by 11% (Figure 1) in just two years (2015-2017) since we last reported on them. Even as governments signed the Paris Agreement in 2015 to significantly rein in global emissions, these companies’ increase of 32.3 million tonnes (MtCO2eq) of GHGs equates to the pollution stemming from 6.9 million passenger cars driven in one year3 (13.6 billion litres or 3.6 billion gallons of gasoline4). Some dairy companies increased their emissions by as much as 30% in the two-year period (Figure 2). Emissions data was obtained using the UN Food and Agriculture Organization (FAO)’s GLEAM methodology and the IFCN dairy research network’s calculation of companies’ production quantities (Annex 1).

The emissions rise occurred amidst a dramatic crash in global dairy prices in 2015-2016. This crash was fuelled partially by increased production from mega-dairies and global dairy corporations that dumped excess dairy into the global market, pushing prices down below the cost of production and forcing out many small to mid-sized dairy farmers. COVID-19 has dramatically compounded the dairy crisis rural communities face (COVID-19 box).

Public policies to redirect public funds away from highly polluting industrial agriculture systems, regulate the negative impacts and regenerate rural communities and livelihoods through agroecological systems are critical to solving the climate crisis and to mitigating the worst effects of unanticipated emergencies like COVID-19. Concrete policies designed to address the overproduction of dairy, including traditional supply management programmes and a slew of complementary agricultural and competition policies that support producers and workers must be seriously considered to both increase rural incomes and lower GHG emissions.

Rising Production, Rising Emissions

Since our first global assessment in 2018 with GRAIN, Emissions Impossible: How big meat and dairy are heating up the planet, the global dairy industry has continued to expand and scale up into new territories through mergers and acquisitions, expanding its collective production by 8% in just two years (Annex 1). As a result, the third largest producer, Group Lactalis’s emissions increased by a whopping 30% (Figure 2) as it expanded into India, Turkey, Brazil, Mexico, Uruguay, Argentina, Hungary and Romania.5 Canada-based Saputo’s emissions increased by 27%, acquiring businesses in the U.K. and Australia. Even Danone, which has positioned itself as a leader on climate mitigation, increased its production and emissions by 15%. Notably, the largest increase in emissions came from Amul, the largest dairy cooperative in India, ramping up its production by 43% in just two years (Annex 1), primarily for domestic consumption with implications for small producers and independent Indian cooperatives.

None of these companies are required by law to publish or verify their climate emissions or present plans to help limit global warming to 1.5˚C. Fewer than half of these companies are publishing their emissions (Annex 1 and 2).6 Only three have committed to targets that address their supply chains where up to 90% of the dairy sector’s emissions reside. These are known as scope 3 emissions (Annex 2). However, zero out of the 13 have committed to a clear and absolute reduction of emissions from their dairy supply chains or emissions from the animals themselves. Nestlé has committed to scope 3 absolute emissions reductions, but given how diversified the company is, it is not clear that these emissions will also include its dairy supply chain.

The UN Framework Convention on Climate Change (UNFCC) is currently discussing agriculture in one of its scientific bodies and at the next climate COP could decide to include agricultural GHGs in the climate negotiations. As governments ratchet up their climate goals for 2030 and 2050, the rise of large-scale dairy and public incentives that further increase corporate dairy power, production and emissions must be stopped. Rural livelihoods and our planet’s future depend on it.

Emissions intensity

Reducing emissions per litre of milk hides environmental costs of overproduction

Emissions from dairy animals in the supply chain (also known as scope 3 emissions) account for over 90% of corporate dairy emissions. Yet, only three companies out of the 13 have pledged to address scope 3 emissions to any degree (Annex 2). Companies such as Danone and Arla track their supply chain emissions through “emissions intensity” reduction targets. For example, Danone pledges a 50% reduction in “emissions intensity” of its supply chain by 2030. This means in 10 years, every litre of milk it processes should emit half as many GHGs as it did in 2015. We argued in Emissions Impossible 2018 that given the level of technological “efficiency” gains in the industrial sector, this drastic reduction seems technologically unrealistic. Ultimately, what counts for a warming climate is whether these companies are reducing their overall emissions at a scale that matters, not their emissions reductions per litre.

With increased attention on the meat and dairy sector, some dairy companies such as Danone, Arla and Fonterra have pledged to reduce their absolute emissions. However, they limit these “absolute” or total reduction pledges to how they operate their offices and processing plants (scope 1 and 2), thereby excluding their supply chain emissions (Annex 2). Nestlé is an exception. It includes a scope 3 absolute reduction target, but given its highly diversified portfolio that includes coffee, cocoa, timber and so many other products, its dairy supply chain may not necessarily be included.

Emissions intensity reduction pledges allow for greenwashing because companies can highlight emissions reductions per litre of milk even if their total emissions continue to rise due to increases in milk production and rising numbers of animals in supply chains. This is clearly demonstrated by the Global Dairy Platform, an association of some of the largest global dairy corporations. The Dairy Platform’s joint study with the FAO reports that the industry reduced emission intensity by 11% between 2005-2015; however, its overall emissions increased by 18% in that same period.7 This is because these companies dramatically increased their worldwide operations and the number of animals in their supply chains, even as they reduced emissions per litre of milk processed.

Their study further suggests that the highest potential for reducing dairy industry emissions through emissions intensity reduction lies in low and middle-income countries. This essentially suggests converting smallholder systems in the Global South to intensive and more industrial dairy systems with more concentrated feed utilisation and higher milk production per cow as key pillars to their strategy. Yet, the European Union, United States and New Zealand alone account for nearly half (46%) of all global dairy production. The companies headquartered in these and other industrialised countries account for the lion’s share of global dairy emissions, and these governments are the best placed to enact policies that enable a Just Transition for dairy producers towards much more climate resilient and agroecological practices in line with ambitious 2030 and 2050 emissions reduction targets.

Dismantling supply management, hastening rural and climate crises

Alongside the rise in production and emissions is the shift toward fewer, but much larger mega-dairies that are flooding the market, pushing out small to mid-sized dairies and hurting rural economies. As mega-dairies increase, much of the opposition to them is led by rural residents, who are critical of the extensive water and air pollution associated with these operations. Governments must begin to address both the rural and climate crises associated with the dairy sector by listening to rural communities about their economic and social needs. There is growing support, for instance, for supply management, a crucial policy that could address dairy’s twin crises. This agriculture policy, currently working in Canada, limits production while providing a viable income to small and mid-sized dairy farms. Since governments in the U.S. and EU have systematically dismantled supply management policies that managed the amount of milk produced and thus entering the world market, a handful of powerful dairy corporations have been able to game the system. With an unregulated milk supply, mass production results in low prices to farmers, which in turn induces farmers to expand production to stay afloat. These economies of scale increase the dairy sector’s climate footprint (more cows, more milk). They also lead to declining farm incomes and inflated corporate profits. Competition policies (or lack thereof) in favour of large corporations have further increased their buyer power by driving mergers and acquisitions, pushing down prices even more.

Supply management schemes prevent overproduction, balance supply and demand and stabilise prices. In their absence, global dairy prices have become volatile with boom and bust cycles. From 2008-2018, the global dairy price crashed twice: 2014-2016 and just five years prior from 2008-2009 (Figure 4).

Dairy prices for the last decade and more have been below the actual cost of production (Figure 5A and 7). In addition, they fail to include environmental or public health costs of industrial scale production. Because farmers integrated into these global chains are paid below production costs, governments step in to subsidise their operations. The weak enforcement of water and air pollution protections when it comes to mega-dairies is another form of government support. In essence, governments subsidise Big Dairy’s growth at the expense of rural communities and the planet. They do so through a variety of national and regional level farm policies such as the U.S. Farm Bill and the EU’s Common Agriculture Policy (CAP).

BOX 1: COVID 19: Rising calls for supply management amidst COVID 19 crisis

“You can’t shut down cows. You can’t turn them off like a faucet.”

-Zoey Nelson, 27, a sixth-generation dairy farmer in Waupaca, Wisconsin8

Beginning in China, COVID-19 created a massive ripple across the dairy sector as governments shut down restaurants, cafes, schools and large parts of the food service industry. China’s lockdown led a massive decline in dairy imports, even as unseasonably mild weather in parts of the U.S. and Europe allowed for increased milk production. Lockdowns also created difficulties in procurement and logistics in the processing industry, compounded by workers getting sick and all coinciding with a collapse in demand.9 The result: farmers with too much milk and nobody to sell it to.

Though European dairy prices were on the rise in the fourth quarter of 2019, and higher prices were expected after a long downturn in the U.S., the series of shutdowns sent milk prices tumbling with a glut of liquid milk. In the global system where dairy corporations favour oversupply and low milk prices, calls for supply management and fair prices are getting louder.

In March, the European Milk Board, representing over 100,000 milk producers, once again proposed an EU-wide Market Responsibility Programme (MRP), a coordinated supply management scheme that would be enacted in three phases to reduce supply as milk prices fall until the crisis is averted.10 The programme is based on a market index that considers several factors including production cost margins. An Index over 100 means that farmers are meeting costs of production, including a fair income. Anything below that number indicates that production costs are not being met. In the first phase of the MRP, an early warning system is activated if the Index falls by 7.5%, including the opening of private storage, more milk going towards suckling calves and fattening heifers. When the Index falls by 15%, the crisis phase is activated and core measures of the MRP are launched, including bonuses for production cuts and levies for overproduction. The final phase is activated when the Index falls by 25% and requires obligatory production cuts by a set amount for a certain duration of time.11 Such a phased in approach is supposed to help deal with unanticipated crises.

In the U.S., food service and institutional purchases for schools, hospitals and the like account for about 30% of milk sales.12 With the shutdowns, dairy farmers poured milk down drains as the virus came on the heels of a debilitating six-year dairy price crash (see U.S. section). In one week, as much as 7% of all milk produced in the U.S. was dumped, while milk processors encouraged farmers to dispose milk, cull herds or stop milking their cows earlier.13 Recently approved U.S. COVID-19 aid programmes would purchase additional fluid and powdered milk, cheese and other dairy products in connection with food banks. The impact of these upcoming purchases on the dairy market is still unclear.

The U.S. dairy industry has proposed a Milk Crisis Plan to restrict milk supply by 10% in the coming months to gain access to part of the $9.5 billion government bailout for farmers. An additional $14 billion discretionary fund is available to help commodity farmers and could be part of government purchases of dairy products. However, family farm-based groups worry that the bulk of these payments will only reinforce a system of overproduction that benefits big agriculture at the cost of farmers, especially those whose regional and direct markets were abruptly eliminated due to the lockdowns. Farmers movements including the California Dairy Campaign, Wisconsin Farmers Union and National Family Farm Coalition want direct payments from the virus aid14 to become part of a systemic change to implement a supply management programme. Such a programme would limit production and hence new or expanded mega-dairies and the number of cows with the associated need for feed grains. It would also create predictable and fair prices for farmers.15 The organisations point to Canada as an example with its long-standing dairy supply management scheme.

The supply management scheme enacted in Canada since the 1970s is providing a level of stability and income support to farmers, lacking for their American counterparts. Yet, in spite of the supply management scheme, the sudden panic buying at grocery stores, followed by a lockdown, created a market shock.16 Canadian farmers were also asked to dump milk due to sudden oversupply to manage prices.17 The Canadian example shows that milk supply cannot, in fact, be shut down from one day to the next. Supply management schemes must be complemented with measures that lessen milk production losses including storage, reserves and social protection programmes that provide a way to direct sudden excess supply to food insecure people.

The global dairy crisis

The view from four regions

As every major dairy producing region (Europe, North America, New Zealand and India) has increased production, indebtedness, farm loss and bankruptcies in rural communities have also increased. Aided and abetted by governments and international organisations such as the International Finance Corporation,18 the World Bank’s private arm, dairy corporations have been allowed to consolidate and ramp up production and emissions.

Europe

In the EU, four out of five dairy farms disappeared in a thirty-year period (1981-2013) (Figure 5C).19 EU’s removal of its milk quota in 2015, along with other factors, contributed to the second global dairy crisis in the last 10 years. Between 1984 and 2009, the dairy quota (the amount of milk allowed into the market) placed limits on European production and stabilised prices for dairy producers. In 2009, the EU started enlarging the quota in order to eliminate it by 2015. Policymakers reasoned that the quota was no longer necessary due to an increased global demand for milk that could absorb unlimited quantities of dairy. As milk flooded the global market, the milk price paid to farmers crashed, to the benefit of global dairy corporations.

Five out of the 13 largest dairy corporations are headquartered in the EU, plus Nestlé in Switzerland (Figure 5B). Nearly all of them benefitted from low farm prices in these two years to boost their production and/or acquisitions (Annex 1). This happened while dairy farmers across Europe lost their farms or were on the verge of bankruptcies. The EU and its member states then had to step in with price supports, public subsidies and ironically initiated a “voluntary” milk reduction scheme which resulted in over 48,000 dairy farmers applying to enter the programme.20

The price crash impacted dairy producers worldwide (Figure 4). The EU is a significant player in global dairy markets, accounting for over a quarter of the world’s exports. Between 2016 and 2017, the EU increased its skim milk powder exports by 35%.21 The EU Commission expects 90% of additional demand for European agricultural products to come from global markets in the next 10 to 12 years. Getting access to other countries’ dairy markets through free trade agreements is therefore central to the EU’s agribusiness growth strategy. EU’s dairy corporations remain competitive in the global market by paying EU farmers below the cost of production and dumping “cheap” dairy exports into developing country markets. In Sub-Saharan Africa, EU’s milk powder exports increased by 20% between 2007-2017, with countries such as Mali, Cameroon and Nigeria particularly hard hit.22 This destabilises local dairy markets and rural communities heavily dependent on dairy animals in these countries. For example, Misereor, a German Catholic charity, found that milk powder imported from the EU was two to four times less than the price of local milk procured in Burkina Faso from the Fulani, a pastoralist ethnic group, dependent on livestock and dairy farming.23 Companies such as Arla, Friesland Campina and Danone have all made expansion into Sub-Saharan Africa a priority for their economic growth plans.24

It is an expansion on the backs of producers North and South. In the EU, farmers paid below the cost of production by these processors are supported through public subsidies through the CAP which is currently up for reform. In 2017, 889 million euros went to meat and dairy producing farms alone as part of “coupled” direct payments from the CAP. This is in addition to millions of euros of direct payments provided through the CAP to farms with large landholdings. If the EU is serious about its climate ambition, not only must the EU dramatically reform the CAP to incentivise environmental resilience, but also regulate the market so that companies pay producers their cost of production plus a reasonable profit. This would not only curb overproduction, but also prevent dumping into global markets.

U.S.

In the U.S., the number of family farms in dairy has declined dramatically since the 1970s, with 93% of these farms since shuttered. The state of Wisconsin starkly illustrates the North American dairy crisis. Between 2014 and 2019, Wisconsin lost nearly a quarter of its 10,000 dairy farms.25 The crisis is directly linked to overproduction, creating a market glut that has pushed prices down. But even though prices have dropped and dairy farms have been lost, overall dairy production in the U.S. continues to rise due to new or expanding mega-dairies (Figure 6). These mega-dairies, often funded by outside investors, are also propped up by a number of Farm Bill programmes and the lack of strong environmental enforcement.

This mega-dairy growth has come with enormous environmental costs, including growing water pollution in states from Wisconsin to California. The U.S. Farm Bill props up mega-dairies by subsidising the management of their giant manure lagoons through the Environmental Quality Incentives Program. The Farm Bill provides government-backed loans to construct new or expanding mega-dairies through its Farm Service Agency. The dairies are further indirectly subsidised by Farm Bill programmes that support below-cost animal feed through farm commodity and insurance programmes.

In addition, the lack of environmental enforcement, particularly of their greenhouse gas emissions, further abets mega-dairies. Only the state of California has a regulatory approach through its climate policy to reduce emissions associated with mega-dairies. But even in California, these mega-dairies are further supported through public subsidies for controversial methane digestors, which allow air and water pollution to continue even as they perversely incentivise additional manure production.26 There are currently no such national-level regulations, nor are there national-level reporting requirements for mega-dairies.

In the U.S., Dean Foods’ lower 2017 carbon footprint of 2% has a backstory. In 2016, Dean Foods terminated contracts with as many as 100 dairy farmers as Walmart, the retail giant, vertically integrated into dairy, directly contracting dairy producers for the milk sold in its stores.27 In November 2019, Dean Foods filed for bankruptcy while initiating talks to merge with the Dairy Farmers of America (the world’s largest dairy emitter and milk producer).28

New Zealand

Half of New Zealand’s emissions come from the livestock sector, its agricultural emissions having risen by 12% since 1990. The government attributes this rise to a doubling of its dairy herd and a 600% increase in fertilizer use.29 New Zealand exports 95% of the milk it produces, largely through Fonterra, the world’s second largest dairy processor, supplying one-third of all global exports (by revenue) in 2018. In two years (2015-2017), Fonterra increased its emissions by 7% (Figure 2) due to a commensurate rise in its production. The company claims that it accounts for 20% of New Zealand’s GHG emissions “with 90% of those emissions from farms; 9% from manufacturing and 1% from distribution to markets across the world.”30

In November 2019, New Zealand became the first country to set GHG reduction targets for agriculture in its new Climate Law as the following: reducing methane by 10% below 2017 levels by 2030; and by 24-47% below 2017 levels by 2050.31 For New Zealand’s methane reduction targets, how Fonterra does business matters (Box 2).

BOX 2: Fonterra’s climate targets, growth and impacts

Fonterra has indicated that it supports the new climate law, but that reaching both the 10% methane reduction target by 2030 and the minimum 24% target by 2050 is “very ambitious” and will require further research and development. The company states that to achieve these targets and more, “the agriculture sector will need to deploy a comprehensive package of breakthrough mitigation activities, including some that are not yet technically and commercially viable.”32 Fonterra’s own climate target aims to achieve a 30% absolute reduction in scope 1 and 2 emissions by 2030 from 2015 GHG levels — so reductions are limited to its operations and processing facilities, even though 90% of its emissions come from its supply chain. With the climate law in place, however, the company is looking into technological fixes such as methane inhibitors to help cows burp less.

These techno fixes, however, present their own dilemmas for the company:

“While there are some promising ideas, such as cow breeding, feeds and inhibitors, we also face some dilemmas. For example, to maximise the effectiveness of inhibitors administered through supplementary feed, the cows would need to spend more time in sheds or on feed pads being fed the special feed. This not only increases the farming costs, it is at odds with the growing consumer interest in pasture-based cows. This means our focus is on inhibitors that can be fed at milking time, and then reduce emissions while the cow is back out on the pasture.”33

Fonterra spent the greater part of the last two decades expanding into global markets. Its export-led strategy has not only led to rising emissions, but also an economic crisis for New Zealand’s dairy producers. Fonterra’s decade long corporate expansion into China, Latin America and Australia, for instance, resulted in one-third of its suppliers unable to pay their bank debts.34 Its nearly 10,000 farmer shareholders incurred huge losses last year, calling into question Fonterra’s corporate structure and investment strategy.35

In 16 years (2003-2019), New Zealand’s on-farm debt increased by NZ$30.1 billion to total over $41 billion, according to New Zealand’s Ministry of Primary Industries.36 The ministry notes that this level of indebtedness makes implementation of New Zealand’s environmental policy much more difficult: “Financial pressures associated with this highly indebted sector may constrain the ability of financially vulnerable farms to invest and adapt to the changes associated with increased environmental and other regulatory requirements on the sector over the longer term.”37 Even as New Zealand becomes the first national government to regulate agricultural methane emissions, unless the government comes up with an economic transition plan for rural dairy producers that incentivizes less production and better pasture management, it is difficult to see how the government fulfils its climate goals.

India

India’s Amul, a state-supported dairy cooperative, recorded the largest increase in emissions due to the massive increase in production between 2015-2017. However, unlike Fonterra or Lactalis, Amul’s emissions are embedded in a complex relationship between millions of Indian dairy producers and government policies that determine their fate.

India produces over 20% of the world’s milk and yet less than half of what it produces is marketed through the organized (cooperatives and private dairies) dairy sector.38 The rest is sold through local and informal networks, with buffalos providing a significant amount of the milk. Ten years ago, 70 million households produced India’s dairy with an average of 1-2 cows each, up to 70% of them small and marginal farmers and landless labourers.39 Women in particular dominate the sector and rely on dairy animals as a critical economic safety net and income.40

Over 16.5 million farmers are integrated into Indian dairy cooperatives such as Amul and Mother Dairy, at least one-third of them are women.41 Nearly a quarter of these producers are members of Amul.42 Like Fonterra, Amul started venturing into global markets in the 2000s. It started selling milk powder on a global dairy trade platform in 2013,43 shortly before milk prices started crashing in 2014.

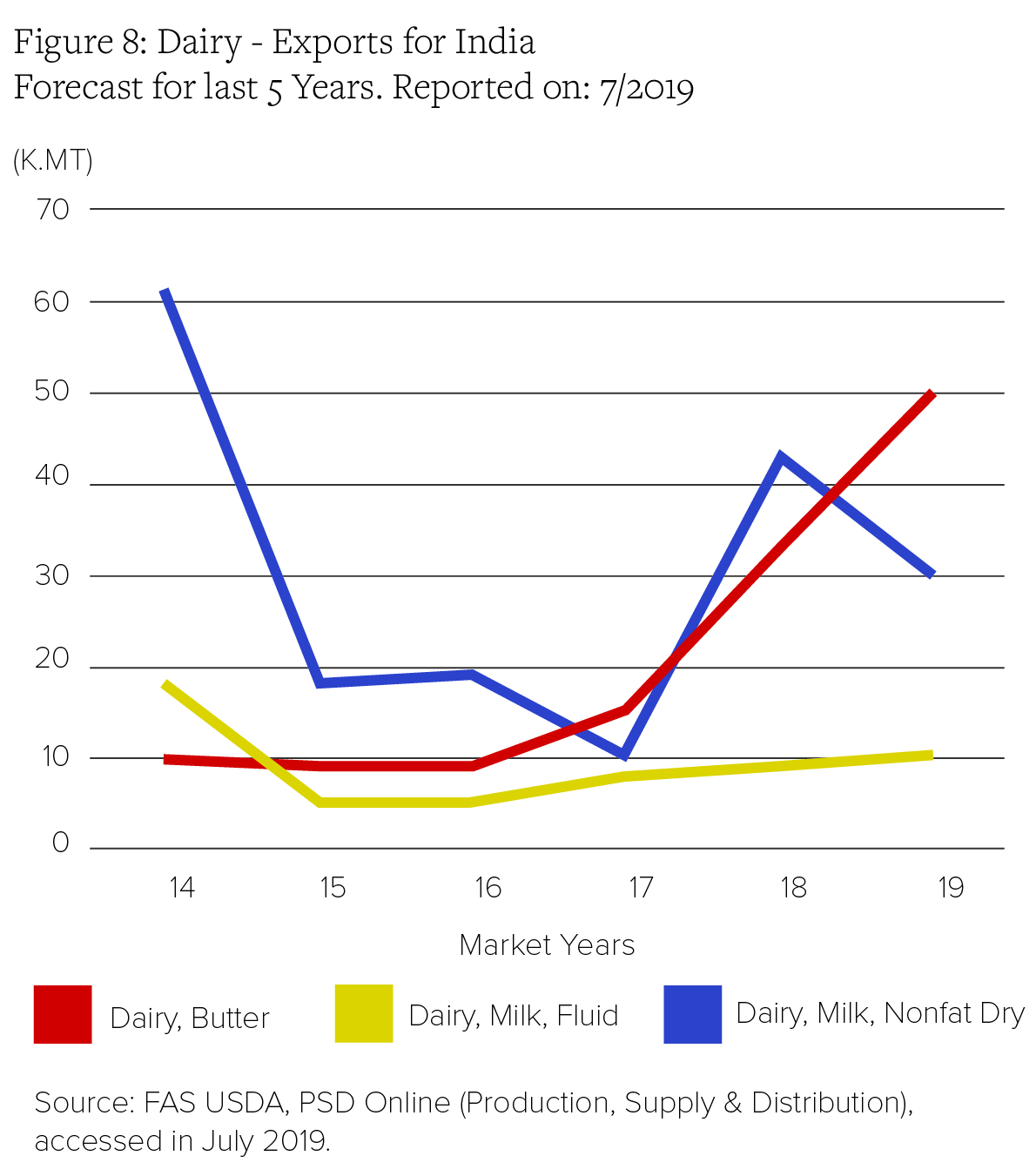

As the global price for skim milk powder crashed in 2014, private and cooperative dairies such as Amul’s management made a decision to stop exporting milk powder (Figure 8).44 Instead, the powder was reconstituted into liquid milk with the addition of butter fat and sold domestically. Between 2013 and 2015, India went from exporting 130,000 tonnes of skim milk powder to just 30,000 tonnes.45 The remaining 100,000 tonnes was reconstituted into liquid milk and dumped into the Indian market at low prices — sending small dairy producers and local markets into a tailspin. Because of the sudden need for butter fat, cheap imports of butter fat also increased, further disrupting local markets. Protests erupted in several parts of the country, and many small dairy producers gave up dairying.46

To alleviate the social upheaval created in the domestic market, the government offered a 20% export subsidy in 2016 for several dairy products.47 The plan seems to have worked as the global dairy supply started contracting in 2017 and India’s milk powder exports went up by 292% between 2017-2018.48

In the last several years, Indian milk production has increased at double the rate of the global average (India’s 4.2% compared to the world’s 2.2%).49 In January of this year, India’s Finance Ministry announced its plans to double its milk processing capacity by 2025.50

Industry data reveals that the dramatic rise in production has created equally dramatic changes in dairying households over the last 20 years. Families owning 1-2 cows declined by 7% between 2000-2016 (from 52% of all dairying farms to 45%).51 With approximately 75 million dairying households in the year 2000, the decrease represents 5.25 million poor households. Half of the milk produced by these households was consumed in the family,52 thus it is likely that they also lost an important source of nutrition. In the same period, families owning 2-10 cows and 31-100 cows, respectively, have gone up by 3% each.53 According to Dairy Global, “The number of family farms with 10-50 cows is constantly growing; in some regions by up to 30% each year.”54 While these are small numbers for a typical farm in the United States, these are dramatic increases in dairy herds for India where fodder and water are short in supply and add significantly to input costs.

With dairy becoming highly capitalised and input dependent, feed and fodder shortages have indeed become acute.55 The Indian Grassland and Fodder Research Institute (IGFRI) estimates nearly a 30% deficit in fodder and 36% deficit in concentrated feed compared to production needs,56 with some states registering over 60% deficits compared to demand. As India relentlessly pursues increased milk production, the 151 million indigenous cattle are increasingly being replaced or cross-bred with foreign high yielding cattle breeds (currently around 40 million)57 with the subsequent need for more feed.

As feed constitutes 60-70% of the costs of Indian dairying, poorer farmers are being squeezed out of the market.58 Rather than focus on how to revitalise these local markets, the Indian government plans to increase investments in productivity of fodder crops and grasslands and increase the use of concentrated feed.59 Such policies would favour producers who have capital. The dramatic projections for increased feed and fodder are based on the premise of ever-increasing production targets and increased productivity of existing cattle. These projections and proposed solutions, however, do not address competing pressures on land and water where 3.3% of all land is classified as permanent pasture, 21% forest and 40% as grazing land on which marginalised and indigenous populations depend.60 These are also biodiversity hotspots. According to IGFRI, livestock is “often the only source of cash income” for 126 million small and marginal farmers and serves as “insurance in the event of crop failure.”61 Yet, the Indian government’s policies seem to be driving India’s dairy sector away from benefitting the poor and marginalised towards a highly capitalised industrial system of dairying. Given that this trajectory has led to rising emissions, farm loss, farm debt and rural disintegration in high-income dairy producing countries, similar impacts are devastating millions of producers who depend on dairy for their livelihoods.

Way forward

Redirect, Regulate, Regenerate

Two years after our first GHG estimates of the big dairy emitters, these corporations have continued to increase their emissions when we should be heading the other way. This is happening as rural dairying disintegrates into larger operations in the control of a handful of corporate dairy processors. And yet, there is a way out of this dead-end through redirecting public funds away from industrial agriculture, regulating the public health, environmental and social impacts of this extractive model of production and designing incentives to regenerate rural communities and agriculture through agroecological practices. Making this shift will not only reduce dairy emissions, but also improve the lives of rural dairy producers and rural communities. However, this requires governments of major milk producing regions of the world to fundamentally shift away from flawed systems of incentives that allows large dairy processors to game the system. Narrow-minded productivist and export-led strategies buttressed by public money and deregulation drive further corporate consolidation of the dairy sector. Now is the time for governments to address these emissions in ramping up their climate targets for 2030 and 2050.

Governments need to begin by integrating climate goals within their national-level farm policies. These climate goals should address strategies to reduce emissions as well as build climate resilience. As important will be to reform trade rules which have driven an export-focused agriculture system, including for dairy — while ignoring the climate. Governments aid and development programmes also need to support an integrated set of social and environmental measures for agroecological systems that support small scale producers in the Global South.

There is growing public support in the U.S., the second largest milk producer, for a dairy supply management system to limit production and ensure that small and mid-sized dairy farmers stay on the land. The Dairy Together campaign led by the Wisconsin Farmers Union and the National Family Farm Coalition have put together different variations of a dairy supply management proposals. Coupled with a supply management system is the need for farm policy to greatly expand conservation and rural development investments that support lower-emitting, more climate-resilient systems of farming, including mid and small-sized organic and grass-fed dairy operations, which also are struggling with low prices, lack of infrastructure and markets.

Regulations must also target emissions associated with mega-dairies. There are rising calls for a U.S. moratorium on new and expanding large-scale confined animal feeding operations. Recent legislation proposed by Senator Corey Booker would place a moratorium on new large-scale CAFOs, provide resources for farmers to transition to new agriculture systems and phaseout of existing big operations by 2040. New national-level climate policy also must place restrictions on GHG emissions from large-scale, high-emitting CAFOs.

In the EU, the ongoing CAP negotiations present perhaps the last opportunity to overhaul the perverse system of public subsidies that benefit large operations integrated into a destructive model of agriculture. The next reform, in sync with Europe’s ambition for a genuine European Green Deal, must help catalyse a shift towards agroecological systems that support rural communities, while preventing harm to small producers in the Global South.

New Zealand’s new climate law must be implemented in tandem with new trade and agriculture policies that diversify the economy away from its addiction to dairy exports. This will entail a dramatic reduction of the country’s dairy herd while at the same time helping dairy producers and workers transition justly to agroecological systems of production and other means of employment that can strengthen New Zealand’s rural communities and environment and make the country less dependent on a fickle global market.

Finally, India’s proliferation of ever larger private and international dairy processors and a few large and highly capitalised state-supported dairy cooperatives are steadily replacing millions of local and diverse channels of dairy distribution through small farmers, milk vendors and independent cooperatives. India’s free trade negotiations involving the EU, New Zealand and the U.S. further threaten these local markets. Yet, implementing India’s National Food Security Act through financial and policy support that helps revitalise local and decentralised dairy markets, thoughtful and progressive agriculture, climate, trade and investment policies that “protect the holistic, multifunctional roles of animals in food and farming systems” would help revitalise rural communities and support millions of small and marginal producers.62 Furthermore, such policies must strengthen the protection of natural resources such as land, water, air, forests, biodiversity and seeds and respect human and indigenous peoples’ rights. For a full set of recommendations, see Food Sovereignty Alliance 2017.

There is scientific consensus that our global food system and land use change is having a dramatic impact on climate change. And yet, those producing our food have been at the receiving end of flawed policies and an ever-narrower set of powerful corporate actors driving these emissions and ecologically destructive farming practices at a scale that is unsustainable for the planet, while economically bankrupting rural communities. For a real climate revolution in the agriculture sector, governments have to fundamentally transform farm and climate policy in a way that shifts power away from these corporate drivers towards agroecological systems that empower rural producers to do the right thing for their families, communities and the planet.

Endnotes

- Climate Accountability Project 2020. Personal Communication with Richard Heede on CAI’s forthcoming publication of annual emissions of the top 20 Carbon Majors for 2017, April 6, 2020. CAI calculates BHP’s (Australia) emissions as 266.4 MtCO2eq and ConocoPhillips’ (USA) as 208.1 MtCO2eq.

- IPCC, Climate Change and Land: an IPCC special report on climate change, desertification, land degradation, sustainable land management, food security, and greenhouse gas fluxes in terrestrial ecosystems, (P.R.Shukla,J.Skea,E.CalvoBuendia,V.Masson-Delmotte, H.-O. Pörtner, D. C. Roberts, P. Zhai, R. Slade, S. Connors, R. van Diemen, M. Ferrat, E. Haughey, S. Luz, S. Neogi, M. Pathak, J. Petzold, J. Portugal Pereira, P. Vyas, E. Huntley, K. Kissick, M. Belkacemi, J. Malley, (eds.), 2019), In press.

- 6,913,394 of passenger vehicles driven for one year; converted from 32 million metric tons CO2e using U.S. Environmental Protection Agency Greenhouse Gas Equivalencies Calculator, for more information see Environmental Protection Agency, “Greenhouse Gas Equivalencies Calculator,” March, 2020, https://www.epa.gov/energy/greenhouse-gas-equivalencies-calculator (accessed June 9, 2020). https://www.epa.gov/energy/greenhouse-gas-equivalencies-calculator

- 13,630,336,448 litres or 3,600,765,163 gallons of gasoline; converted from 32 million metric tons CO2e using U.S. Environmental Protection Agency Greenhouse Gas Equivalencies Calculator, for more information see Environmental Protection Agency, “Greenhouse Gas Equivalencies Calculator,” March, 2020, https://www.epa.gov/energy/greenhouse-gas-equivalencies-calculator (accessed May 19, 2020).

- Groupe Lactalis, “History,” Groupe Lactalis, (n.d.), https://www.lactalis.fr/en/the-group/history/#/annees2010 (accessed May 13, 2020).

- Five out of 13 are actually reporting any or all of their GHG emissions. Arla, Danone, Fonterra and Nestlé seem to be the only ones doing third-party verification of all their reported emissions as per the Carbon Disclosure Project Database. Saputo has done third-party verification on only its scope 1 and 2 emissions and not its supply chain emissions. It is not clear that Friesland Campina has third-party verification in place for its reported emissions in its annual report.

- Global Agenda for Sustainable Livestock. “Climate change and the global dairy cattle sector – The role of the dairy sector in a low-carbon future.” Food and Agriculture Organization of the UN and Global Dairy Platform, 2018, Rome. http://www.fao.org/3/CA2929EN/ca2929en.pdf (accessed May 19, 2020)

- Vaughn Hillyard, Maura Barrett and Matt Wargo, “Dairy farmers forced to dump milk as the demand drops amid coronavirus closures,” NBC news, April 14, 2020, https://www.nbcnews.com/news/us-news/dairy-farmers-forced-dump-milk-demand-drops-amid-coronavirus-closures-n1182601 (accessed May 13, 2020).

- European Milk Board, “Coronavirus spreads to producers in the dairy sector,” European Milk Board, March 19, 2020, http://www.europeanmilkboard.org/special-content/news/news-details/article/coronavirus-crisis-spreads-to-producers-in-the-dairy-sector.html?cHash=cfb7b27731e86a621dbe1bb4e77a06d0 (accessed May 13, 2020).

- European Milk Board, “Market Responsibility Programme,” 2018, http://www.europeanmilkboard.org/fileadmin/Subsite/MVP/MVP_EN_122018_1.pdf (accessed May 13, 2020).

- For more information, see European Milk Board, “Market Responsibility Programme,” European Milk Board, 2018, http://www.europeanmilkboard.org/fileadmin/Subsite/MVP/MVP_EN_122018_1.pdf (accessed May 13, 2020).

- Siena Chrisman, “The Coronavirus Pandemic is Pushing Dairy Farmers to the Brink,” Civil Eats, April 8, 2020, https://civileats.com/2020/04/08/the-coronavirus-pandemic-is-pushing-the-dairy-crisis-to-the-brink/ (accessed May 13, 2020).

- Jesse Newman and Jacob Bunge, “Farmers Dump Milk, Break Eggs as Coronavirus Restaurant Closings Destroy Demand,” The Wall Street Journal, April 9, 2020, https://www.wsj.com/articles/farmers-deal-with-glut-of-food-as-coronavirus-closes-restaurants-11586439722 (accessed May 13, 2020).

- Siena Chrisman, “The Coronavirus Pandemic is Pushing Dairy Farmers to the Brink,” Civil Eats, April 8, 2020, https://civileats.com/2020/04/08/the-coronavirus-pandemic-is-pushing-the-dairy-crisis-to-the-brink/ (accessed May 13, 2020).

- Lela Nargi, “Can This Radical Approach to Dairies Save US Farms?,” Civil Eats, March 11, 2019, https://civileats.com/2019/03/11/can-this-radical-approach-to-dairies-save-us-farms/ (accessed May 13, 2020).

- Aleksandra Sagan, “Why Canada’s dairy farmers are dumping milk despite food supply issues in COVID-19,” CBC, April 9, 2020, https://www.cbc.ca/news/business/dairy-covid-19-1.5528331 (accessed May 13, 2020).

- BBC, “Coronavirus: Why Canada dairy farmers are dumping milk,” BBC News, April 6, 2020, https://www.bbc.com/news/world-us-canada-52192190 (accessed May 13, 2020).

- A $145 million financial package to Dutch company Friesland Campina for acquiring a Pakistani dairy processor Engro Foods, for more information see International Finance Corporation (IFC), “IFC Financing Package to Support Development of Pakistan’s Dairy Industry,” Press Release International Finance Corporation, February 3, 2017, https://ifcextapps.ifc.org/ifcext/pressroom/ifcpressroom.nsf/0/7622FF047028889B852580BF00290E97?OpenDocument (accessed March 25, 2020).

- Marie-Laure Augère-Granier, “The EU dairy sector. Main features, challenges and prospects,” Briefing European Parliament, December, 2018, http://www.europarl.europa.eu/RegData/etudes/BRIE/2018/630345/EPRS_BRI(2018)630345_EN.pdf (accessed May 13, 2020).

- Ibid.

- European Commission, “Milk Market Observatory: Historical Series: EU+UK Export of Dairy Products to Third Countries,” European Commission, February 21, 2020, https://ec.europa.eu/info/sites/info/files/food-farming-fisheries/farming/documents/eu-dairy-historical-trade-series_en.pdf (accessed May 19, 2020).

- Kerstin Lanje and Tobias Reichert, Billige Nahrungsmittel und ihre Folgen. Die EU-Exportstrategie – Das Beispiel Milch und die Auswirkungen auf die Weidetierhalter in Burkina Faso, In: Deutschland und die globale Nachhaltigkeitsagenda 2017: Großbaustelle Nachhaltigkeit. (Berlin/Bonn/Köln: Vendro et al., 2017), 73-79, https://www.2030report.de/sites/default/files/grossbaustelle/kapitel/Schattenbericht_2017_II-2.pdf (accessed May 20, 2020).

- Ibid.

- Ibid., see also Arla, “Investor Announcement: Sub-Saharan Africa: Arla aims to triple sales by 2020,” Arla, February 17, 2016, p. 5, https://www.arla.com/491b31/contentassets/e413bc32e41a4257a34a7c6f0f0347be/investor_announcement_17-02-2016.pdf (accessed May 20, 2020).

- Andrew Mollica and Milwaukee Journal Sentinel, “Wisconsin dairy farms: A portrait of loss,” Journal Sentinel, January 6, 2020, https://projects.jsonline.com/news/2019/5/16/wisconsin-dairy-farms-a-portrait-of-loss-map.html (accessed May 13, 2020).

- Tara Ritter, “Hidden props for factory farms in California climate programs,” Institute for Agriculture and Trade Policy, October 31, 2017, https://www.iatp.org/blog/201904/hidden-props-factory-farms-california-climate-programs (accessed May 13, 2020).

- Anna-Lisa Laca, “Walmart opens Indiana Milk Plant,” Farm Journal’s Milk, June 13, 2018, https://www.milkbusiness.com/article/walmart-opens-indiana-milk-plant (accessed May 13, 2020).

- Dean Foods, “Restructuring Information,” Dean Foods, November 12, 2019, https://deanfoodsrestructuring.com/ (accessed May 13, 2020).

- Government of New Zealand, “New Zealand’s Greenhouse Gas Inventory 1990-2016,” Ministry for the Environment, April, 2018, https://www.mfe.govt.nz/sites/default/files/media/Climate%20Change/final_greenhouse_gas_inventory_snapshot.pdf (accessed May 13, 2020).

- Fonterra, “Sustainability Report: For the year ending 31 July 2019. Fonterra Co-operative Group Limited,” Fonterra, 2019, https://view.publitas.com/fonterra/sustainability-report-2019/page/1 (accessed May 13, 2020).

- Government of New Zealand, “Climate Change Response (Zero Carbon) Amendment Act. What the Climate Change Response (Zero Carbon) Amendment Act does. The steps to get the new provisions up and running,” Ministry for the Environment, November 25, 2019, https://www.mfe.govt.nz/climate-change/zero-carbon-amendment-act (accessed May 13, 2020).

- Fonterra, “Sustainability Report: For the year ending 31 July 2019. Fonterra Co-operative Group Limited,” Fonterra, 2019, https://view.publitas.com/fonterra/sustainability-report-2019/page/1 (accessed May 13, 2020).

- Ibid., p. 64.

- Jamie Smyth, “Fonterra’s global ambitions sour dairy group’s fortunes,” Financial Times, August 26, 2019, https://www.ft.com/content/86450ea2-c4a1-11e9-a8e9-296ca66511c9 (accessed May 13, 2020).

- Jamie Smyth, “NZ’s Fonterra faces record loss after troubled overseas expansion,” Financial Times, August 12, 2019, https://www.ft.com/content/6ca82a88-bc9f-11e9-b350-db00d509634e (accessed May 13, 2020).

- New Zealand Herald, “High dairy debt may curb ability to meet challenges ahead, MPI warns,” New Zealand Herald, December 16, 2019, https://www.nzherald.co.nz/business/news/article.cfm?c_id=3&objectid=12294249 (accessed May 13, 2020).

- Ibid.

- Government of India, Economic Survey 2018-2019. Volume 2. Chapter 7: Agriculture and Food Management, (New Delhi: Government of India, 2019), 172-196, https://www.indiabudget.gov.in/economicsurvey/doc/vol2chapter/echap07_vol2.pdf (accessed May 20, 2020).

- Food Sovereignty Alliance, “The Milk Crisis in India: The story behind the numbers,” biliterals.org, October 15, 2017, https://www.bilaterals.org/?the-milk-crisis-in-india-the-story&lang=en (accessed May 13, 2020).

- Ibid.

- Government of India, “Cattle and Dairy Development,” Government of India. Department of Animal Husbandry and Dairying, 2019, http://www.dahd.nic.in/about-us/divisions/cattle-and-dairy-development (accessed May 13, 2020).

- Amul, “Gujarat Cooperative Milk Marketing Federation Ltd.,” Amul, (n.d.), https://amul.com/m/organisation (accessed May 13, 2020).

- Ibid.

- Food Sovereignty Alliance, “The Milk Crisis in India: The story behind the numbers,” biliterals.org, October 15, 2017, https://www.bilaterals.org/?the-milk-crisis-in-india-the-story&lang=en (accessed May 13, 2020).

- Ibid.

- Ibid.

- Jagdish Kumar, “India: 126% growth in dairy exports,” Dairy Global, October 3, 2019, https://www.dairyglobal.net/Market-trends/Articles/2019/10/India-126-growth-in-dairy-exports-480318E/ (accessed May 13, 2020).

- Jagdish Kumar, “India: 126% growth in dairy exports,” Dairy Global, October 3, 2019, https://www.dairyglobal.net/Market-trends/Articles/2019/10/India-126-growth-in-dairy-exports-480318E/ (accessed May 13, 2020).

- Emmy Koeleman, “India’s dairy ambitions are high, but feed is a problem,” Global Dairy, March 12, 2015, https://www.dairyglobal.net/Articles/General/2015/3/Indias-dairy-ambitions-are-high-but-feed-is-a-problem-1722872W/ (accessed May 13, 2020).

- Rutam Vora, “Budget 2020: Plan to double milk production to 108 MT by 2025,” The Hindu Business Line, February 1, 2020, https://www.thehindubusinessline.com/economy/agri-business/budget-2020-plan-to-double-milk-production-to-108-mt-by-2025/article30710390.ece (accessed May 13, 2020).

- Emmy Koeleman, “Dairy farms in India become bigger,” Dairy Global, December 21, 2017, https://www.dairyglobal.net/Market-trends/Articles/2017/12/Dairy-farms-in-India-become-bigger-226874E/ (accessed May 13, 2020).

- Government of India, “Cattle and Dairy Development,” Government of India. Department of Animal Husbandry and Dairying, 2019, http://www.dahd.nic.in/about-us/divisions/cattle-and-dairy-development (accessed May 13, 2020).

- Ibid.

- Ibid.

- Samyak Pandey, “Fodder shortage in India major reason behind rise in milk costs, says govt institute,” The Print, January 11, 2020, https://theprint.in/india/fodder-shortage-in-india-major-reason-behind-rise-in-milk-costs-says-govt-institute/347883/ (accessed May 13, 2020).

- Ibid.

- Ibid.

- Ibid.

- Emmy Koeleman, “India’s dairy ambitions are high, but feed is a problem,” Global Dairy, March 12, 2015, https://www.dairyglobal.net/Articles/General/2015/3/Indias-dairy-ambitions-are-high-but-feed-is-a-problem-1722872W/ (accessed May 13, 2020).

- A. K. Roy, R. K. Agarwal, N. R. Bhardwaj, A.K. Mishra and K. Mahanta, “Revisiting National Forage Demand and Availability Scenario,” In: Indian Fodder Scenario: Redefining State Wise Status, (Jahansi: AICRP on Forage Crops and Utilization ICAR-IGFRI, 2019): 1-21.

- Ibid., p. 1.

- Food Sovereignty Alliance, “The Milk Crisis in India: The story behind the numbers,” biliterals.org, October 15, 2017, https://www.bilaterals.org/?the-milk-crisis-in-india-the-story&lang=en (accessed May 13, 2020).

Downloads:

Download a PDF of the full paper, which contain Annex 1 and 2.

View and download the Milking the Planet original dataset.

Visit our Q&A page and download a copy of the Q&A.

Watch:

Watch a short video on Milking the Planet.

If you've found this article and others like it to be valuable, please consider making a contribution to support our work today. As a nonprofit, we rely on the generosity of our supporters to provide high-level research and analysis on agriculture and trade policy.