During the fight to pass and implement the Dodd-Frank Wall Street Reform and Consumer Financial Protection Act of 2010, a favorite Wall Street lobbyist tactic was to organize small and large non-financial business owners to talk with members of Congress about the “unintended consequences” for Main Street of regulating Wall Street. Wall Street didn’t want to be seen as directly lobbying for continuing the regulatory exemptions that lead to the big bank bankruptcies and multi-billion dollar bailouts of 2007–2009.

Instead the Chamber of Commerce, International Swaps and Derivatives Association and other lobby groups’ strategy used “Main Street” clients to promote the idea that global banks such as Goldman Sachs and J.P. Morgan should operate under many of the same rules as small businesses under Dodd-Frank. In sum, they argued, it is in the interest of Main Street business to not reform Wall Street “too much.”

For example, Dodd-Frank exempts municipal electricity and gas companies from having to put money down (margin collateral) to trade to manage their price risks in the commodity derivatives market. (Derivatives are financial contracts that manage the price risk of an underlying asset, such as wheat, oil or a mortgage interest rate.) Municipal companies must provide service to all, and the cost of posting margin collateral for each trade puts them in a competitive disadvantage with electricity and gas companies that can deny service to the poor. Through their lobbying associations, Wall Street banks argued that they are essential buyers and sellers of such derivatives contracts, and sought to benefit from this margin collateral and other Dodd-Frank exemptions for derivatives trading by commercial users of commodities.

Numerous allegations of the banks’ abuse of the Federal Reserve’s Bank Holding Company Act regulation to allow banks to own and trade commodities in which they also trade derivatives contracts has lead the Fed to consider changing the regulation. Now, Wall Street is trotting out Main Street business representatives once again, this time in an attempt to get the Fed to allow Wall Street to continue to own and trade physical commodities, which are not covered by the Dodd-Frank reforms, to commodity derivatives contracts. Officials from these municipal utility companies are visiting legislators, including Dodd-Frank opponent and incoming U.S. Senate Finance and Banking Chair Senator Richard Shelby, whose committee oversees the Fed. It is not improbable that Senator Shelby invited the visits, following Wall Street lobbying.

The municipal officials complain that Federal Reserve Bank rules under discussion on big bank ownership and trading of physical commodities will harm Main Street gas and electricity service provision. Notwithstanding J.P. Morgan manipulation of electricity supply and prices, the Main Street officials agree with the Wall Street lobbyists that gas, electricity and other physical commodity prices will only be affordable if big banks are allowed to compete with Big Electricity (and little electricity) for supply and price. The Main Street lobbying trips are designed to defend the Fed rule that allows banks with huge and unique competitive advantages, such as access to the lowest interest rate Fed loans, to “compete” with commercial users of those commodities.

IATP criticized this rule in an April comment letter on proposed rulemaking. As we noted then, gas and oil prices affect the agricultural cost of production for such inputs as chemical fertilizer and diesel fuel.

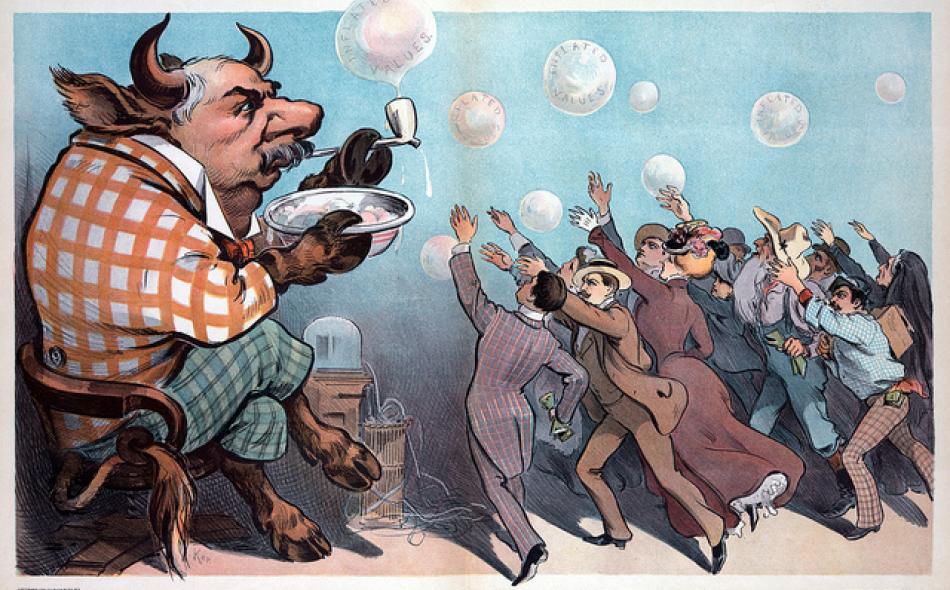

The timing of the lobbying trips couldn’t have been better. The U.S. Senate Permanent Subcommittee on Investigations (PSI) held a November 20-21 hearing related to the release of a scathing 400-page report, “Wall Street Bank Involvement With Physical Commodities.” The two-year investigation found that bank ownership of physical commodities, such as operating oil and gas pipelines, coal mines and power plants, allowed them to control the physical supply of commodities in which they traded derivatives contracts. According to the report, the deregulatory erosion of banking laws, which separate commercial activities from banking activities, exposed the banks and commercial entities to “significant financial loss, catastrophic event risks, unfair trading, market manipulation, credit distortions, unfair business competition, and conflicts of interest.”

As in prior PSI reports on Wall Street trading of natural gas and wheat derivatives contracts, Senate investigators found troubling trading practices and regulatory failures. The latest commodities trading report concludes with recommendations for the Fed to change its rule, in order to prevent the banks’ “complementary activities” from undermining their “safety and soundness,” e.g., through losses due to commodity related environmental accidents.

The PSI, under Republican Party leadership beginning in January, is very unlikely to do any more investigation that will discomfit Wall Street. Indeed, the leadership has already characterized Dodd-Frank as “Obamacare for banks,” and indicated that the Republican majority House and Senate could vote to repeal all of Dodd-Frank or cripple it by refusing to fund its implementation and enforcement, in the name of defending community banks and, of course, Main Street. The PSI report and hearing are a bittersweet swan song for retiring Senator Carl Levin (D-Michigan), one the few Senators willing to investigate Wall Street.

The Republican Congressional majority will not be alone in government in the effort to gut Dodd-Frank. A recent Republican appointee to the Commodity Futures Trading Commission (CFTC), Commissioner Christopher Giancarlo, released the text of a speech that indicated he intends to tear up CFTC regulations to implement Dodd-Frank. By posting the speech, intended for an industry group to which he had belonged, on the CFTC website, Giancarlo violated the spirit of President Barack Obama’s executive order prohibiting political appointees from appearing before industry groups with which they just had been associated. Giancarlo argues that unless CFTC rules are rewritten, derivatives contracts currently traded on U.S. markets by U.S. headquartered firms will migrate to foreign markets through the U.S. dealer broker’s foreign affiliates, resulting in the loss of “thousands” of jobs on Wall Street.

The carefully drafted and footnoted speech is the kind of document that the House and Senate majority party will cite as “evidence” of the need to repeal or “reform” Dodd-Frank. The House had cited several speeches by former Commissioner Scott O’Malia, who left the CFTC before the end of his term to become CEO of the International Swaps and Derivatives Association, in its report justifying a CFTC reauthorization bill (H.R. 4413) that authorized Commissioners to micro-manage even the length of enforcement subpoenas. The recent headlines of billion dollar fines for Wall Street violations of civil law reflect a cost that will diminish when political appointees vote on whether to investigate Wall Street firms that are financing the elections of both political parties.

Despite ample evidence to prosecute global bank executives for a broad range of financial crimes, the Department of Justice continues to avoid prosecution. DoJ apparently believes that the conviction of a handful of individuals will destabilize further a U.S. economy that suffered an at least $13 trillion loss as a result of the financial crisis of 2007–2009. Cities, both big and small, continue to suffer from Wall Street’s financial innovations that promised savings or profit that instead resulted in loss or greater debt. Main Street is doing itself no favors by continuing to enable Wall Street to operate with impunity.